Show that, for constant drift and volatility , and zero discount rate, that the price of

Question:

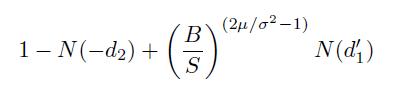

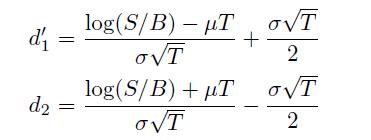

Show that, for constant drift μ and volatility σ, and zero discount rate, that the price of an up and in one-touch option, barrier height B ≥ S, maturity T is given by:

where

(Use (3.17) for the joint density of the terminal spot for a constant drift Brownian motion and its maximum over the interval of the trade.)

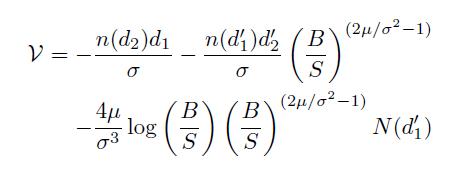

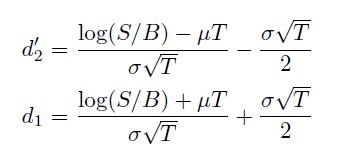

Show that the vega of this option is given by:

where

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Anum Naz

Lecturer and researcher with 10+ years of experience teaching courses in both undergraduate and postgraduate levels. Supervised 17 BA theses, 07 MA theses, and 1 Ph.D. dissertations. Edited and co-authored 2 monographs on contemporary trends in political thought. Published over articles in peer-reviewed journals.

11+ Reviews

52+ Question Solved

Related Book For

The Value Of Uncertainty Dealing With Risk In The Equity Derivatives Market

ISBN: 9781848167728,9781908979582

1st Edition

Authors: George Kaye

Question Posted: