Assume that the time dependent volatility function (t) is deterministic. Suppose we write imp (t, T)

Question:

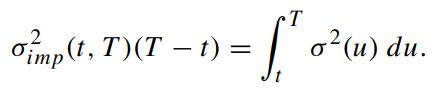

Assume that the time dependent volatility function σ(t) is deterministic. Suppose we write σimp (t, T) as the implied volatility obtained from the time-t price of a European option with maturity T , for T > t. Show that

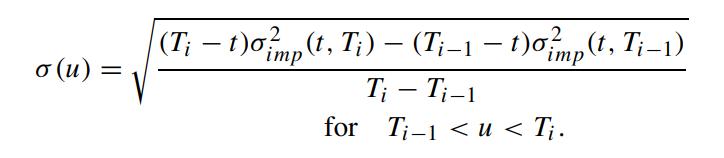

In real situations, we may have the implied volatility available only at discrete times Ti,i = 1, 2, ··· ,N. Assuming the volatility σ(T) to be piecewise constant over each time interval [Ti−1,Ti],i = 1, 2, ··· ,N, show that

The implied volatility σimp(t, T ) and the time dependent volatility function σ(t) are related by

The implied volatility σimp(t, T ) and the time dependent volatility function σ(t) are related by

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The given expression relates the implied volatility impt T to the timedependent volatility function ...View the full answer

Answered By

Madhvendra Pandey

Hi! I am Madhvendra, and I am your new friend ready to help you in the field of business, accounting, and finance. I am a College graduate in B.Com, and currently pursuing a Chartered Accountancy course (i.e equivalent to CPA in the USA). I have around 3 years of experience in the field of Financial Accounts, finance and, business studies, thereby looking forward to sharing those experiences in such a way that finds suitable solutions to your query.

Thus, please feel free to contact me regarding the same.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: