Consider a discretely monitored down-and-out call option with strike price X and barrier level B i at

Question:

Consider a discretely monitored down-and-out call option with strike price X and barrier level Bi at discrete time ti,i = 1, 2, ··· ,n. Show that the price of this European barrier call option is given by (Heynen and Kat, 1996)

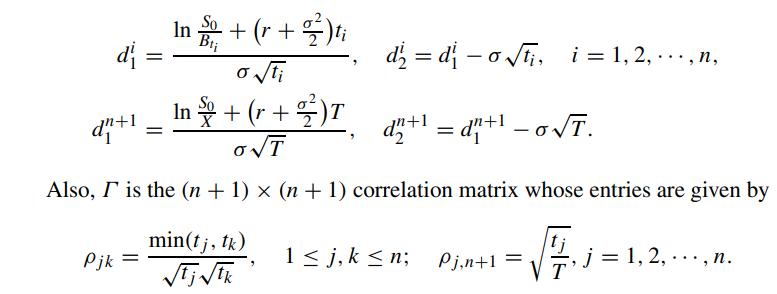

where

where

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To show that the price of the European barrier call option is given by the provided expression we ca...View the full answer

Answered By

Aun Ali

I am an Associate Member of Cost and Management Accountants of Pakistan with vast experience in the field of accounting and finance, including more than 17 years of teaching experience at university level. I have been teaching at both undergraduate and post graduate levels. My area of specialization is cost and management accounting but I have taught various subjects related to accounting and finance.

13+ Reviews

32+ Question Solved

Related Book For

Question Posted: