Consider the two-factor Gaussian model, which is a combination of the HoLee and Vasicek models. Let the

Question:

Consider the two-factor Gaussian model, which is a combination of the Ho–Lee and Vasicek models. Let the volatility structure in the HJM framework be given by

![]()

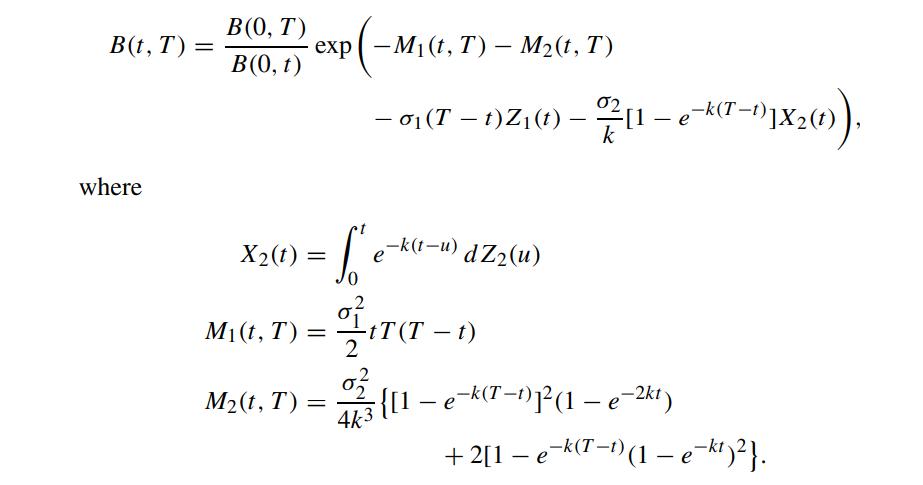

Show that the bond price B(t, T) is given by (Heath, Jarrow and Morton, 1992).

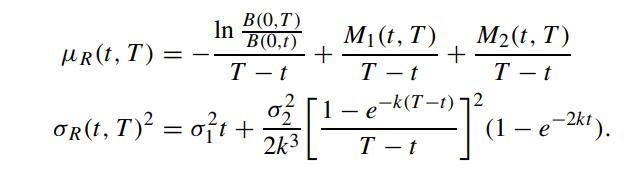

Also, show that the yield to maturity R(t, T) is normally distributed with mean μR(t, T) and variance σR(t, T)2:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The expression for the bond price BtT and the yield to maturity RtT provided in the question a...View the full answer

Answered By

Nyron Beeput

I am an active educator and professional tutor with substantial experience in Biology and General Science. The past two years I have been tutoring online intensively with high school and college students. I have been teaching for four years and this experience has helped me to hone skills such as patience, dedication and flexibility. I work at the pace of my students and ensure that they understand.

My method of using real life examples that my students can relate to has helped them grasp concepts more readily. I also help students learn how to apply their knowledge and they appreciate that very much.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: