The management of Roach plc is currently assessing the possibility of manufacturing and selling a new product.

Question:

The management of Roach plc is currently assessing the possibility of manufacturing and selling a new product. Two possible approaches have been proposed.

Approach A This involves making an immediate payment of £60,000 to buy a new machine. It is estimated that the machine can be used effectively for three years, at the end of which time it will be scrapped for zero proceeds.

Approach B This involves using an existing machine, which cost £150,000 two years ago, since when it has been depreciated at the rate of 25 per cent p.a., on cost. The business has no use for the machine other than in the manufacture of the new product, so if it is not used for that purpose it will be sold. It could be sold immediately for £48,000. Alternatively there is a potential buyer who will pay £60,000 and take delivery of the machine in one year’s time. There are no additional costs of retaining the machine for another year.

If the machine is retained for manufacturing the new product, it will be scrapped (zero proceeds) in two years’ time.

The staff required under Approach B will be transferred from within the business. The total labour cost involved is £25,000 for each of the next two years. The employees concerned will need to be replaced for two years at a total cost of £20,000 for each of those years. The operating profit estimates, given below, are based on the labour cost of the staff that will actually be working on the new product.

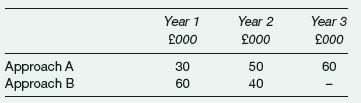

The estimated operating profits, before depreciation, from the new product are as follows:

The new production will require additional working capital. This is estimated at 10 per cent of the relevant year’s operating profit, before depreciation. It is required by the beginning of the relevant year.

The business’s cost of finance to support this investment is 20 per cent p.a.

On the basis of NPV, which, if either, of the two approaches should the business adopt?

Step by Step Answer: