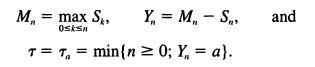

1.5. Consider the simple random walk in which the summands are independent with Pr{ 11 _ 2W...

Question:

1.5. Consider the simple random walk

![]()

in which the summands are independent with Pr{ 11 _ 2W e are going to stop this random walk when it first drops a units below its maximum to date. Accordingly, let

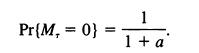

(a) Use a first step analysis to show that

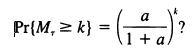

(b) Why is Pr{M, 2} = Pr{M, ? 1 }2, and

Identify the distribution of M,.

(c) Let B(t) be standard Brownian motion, M(t) = max{B(u);

0

a. Note: r is a popular strategy for timing the sale of a stock. It calls for keeping the stock as long as it is going up, but to sell it the first time that it drops a units from its best price to date. We have shown that E[M(T)] =

a, whence E[B(T)]

E[M(T)] - a = 0, so that the strategy does not gain a profit, on average, in the Brownian motion model for stock prices.

Step by Step Answer:

An Introduction To Stochastic Modeling

ISBN: 9780126848878

3rd Edition

Authors: Samuel Karlin, Howard M. Taylor