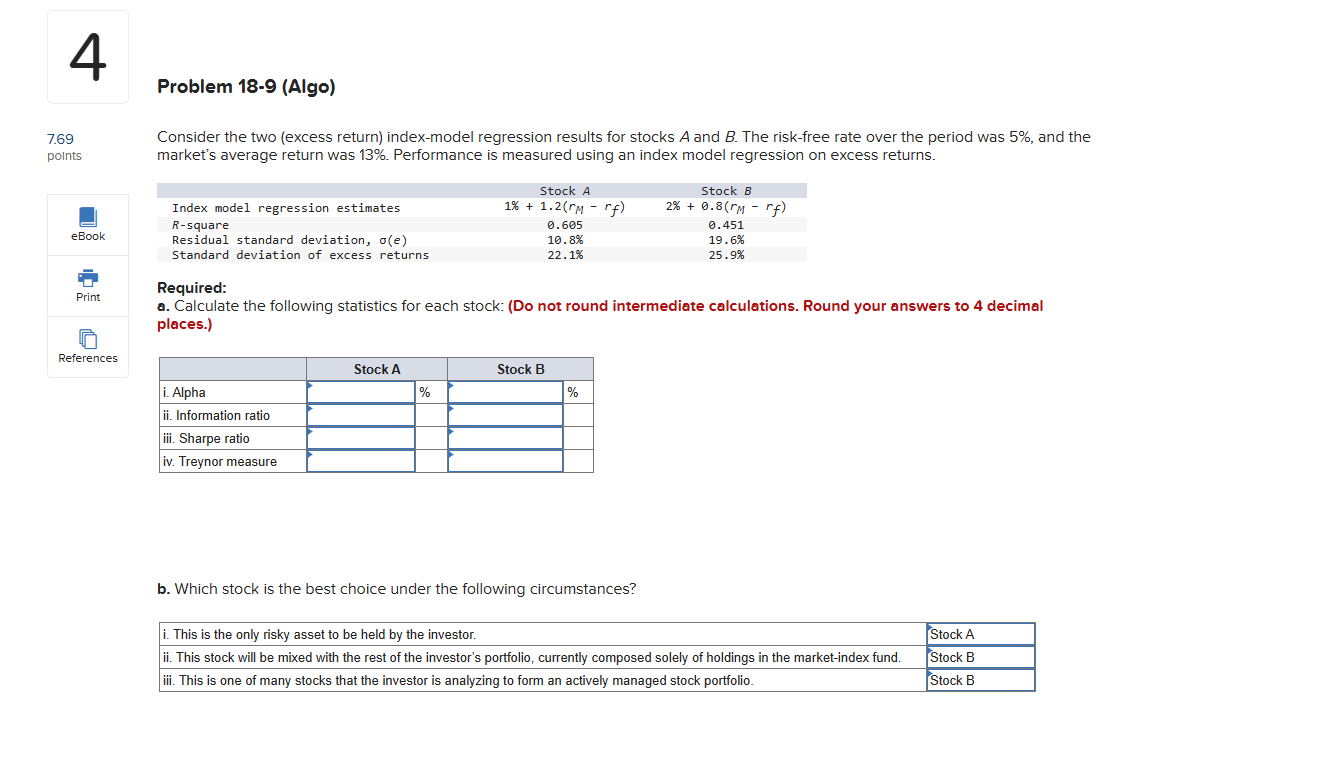

769 points References Problem 18-9 (Algo) Consider the two (excess return) index-model regressicon results for stocks A and B. The risk-free rate over the period

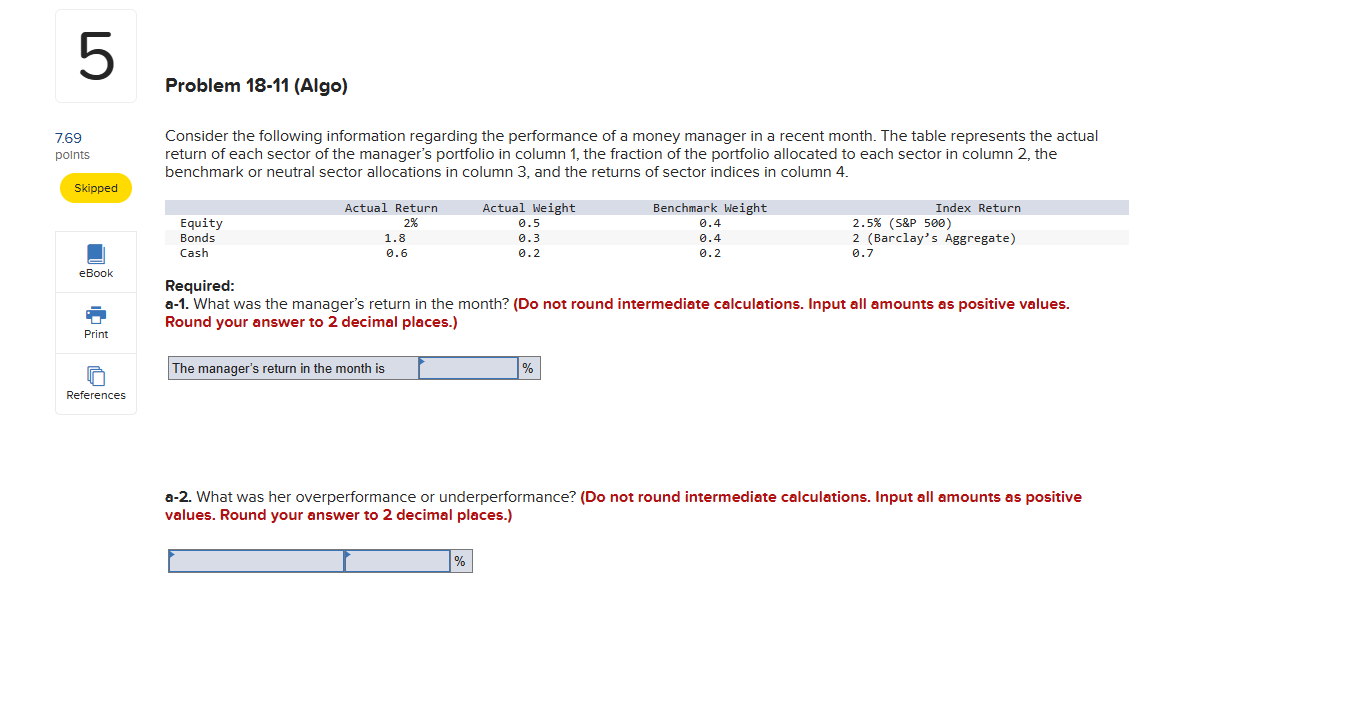

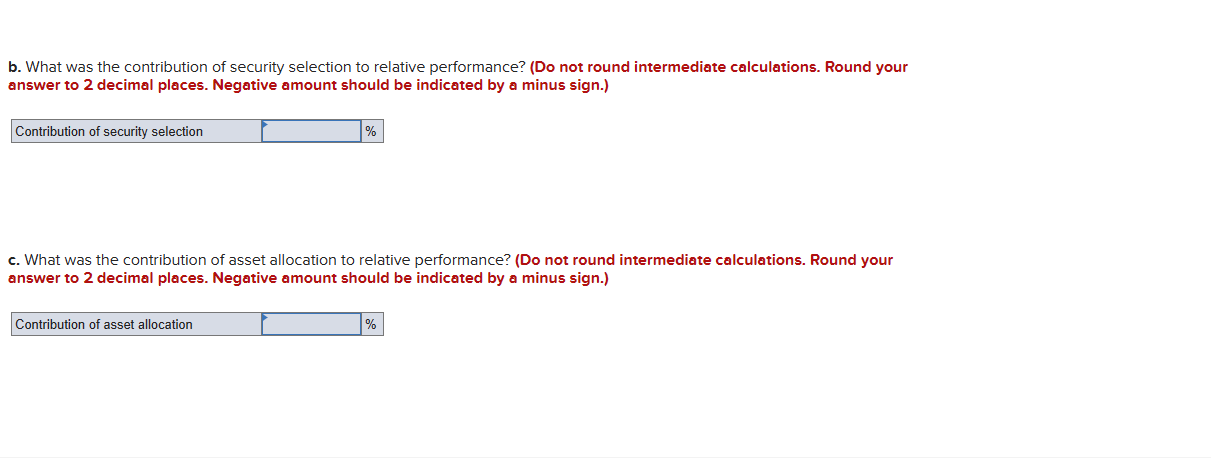

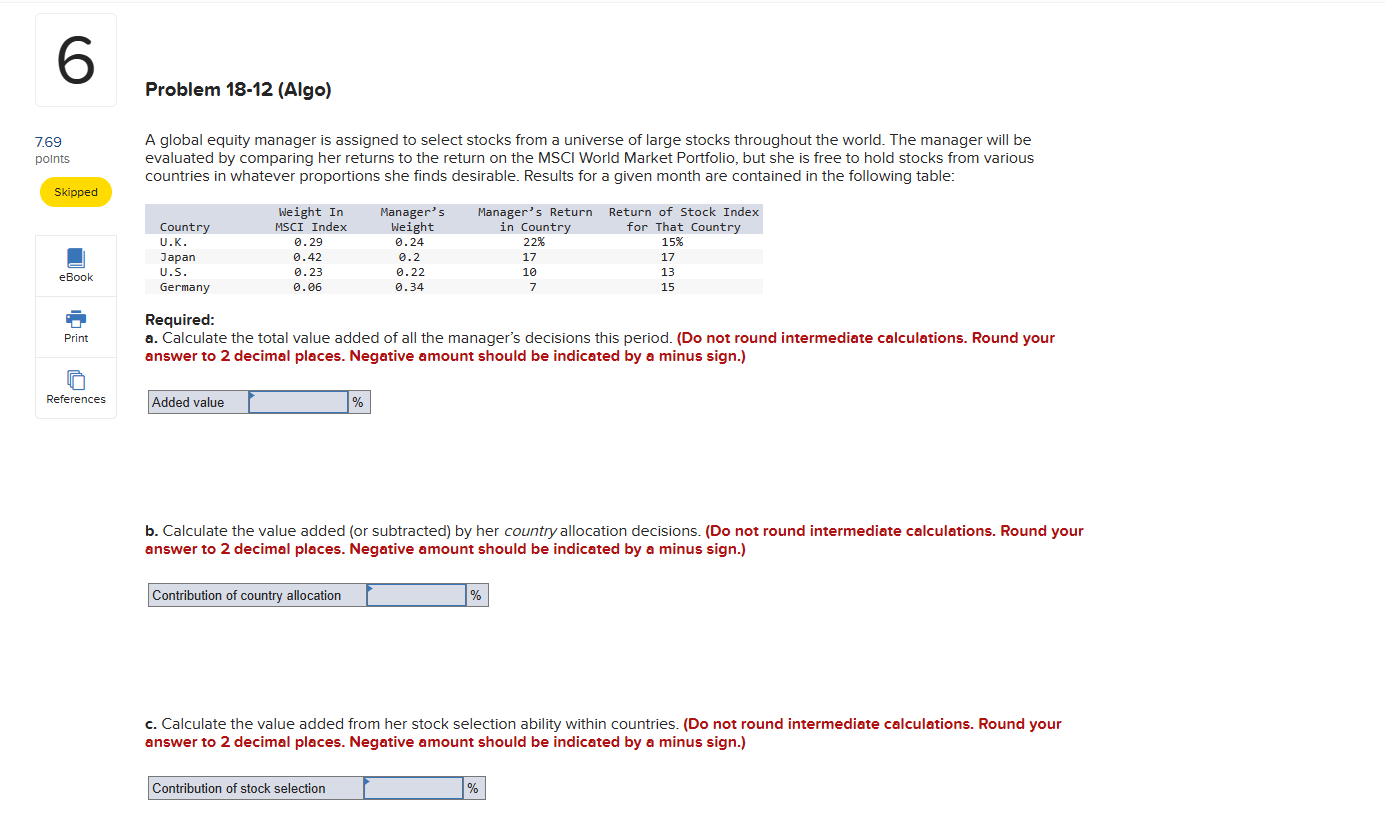

769 points References Problem 18-9 (Algo) Consider the two (excess return) index-model regressicon results for stocks A and B. The risk-free rate over the period was 5%, and the market's average return was 13%. Performance is measured using an index model regression on excess returns. Stock A Stock B Index model regression estimates 1% + 1.2(ry - '"_f) 2% + 0.8(rpy - "'fj R-square 0.685 @.451 Residual standard deviation, o(e) 10.8% 19.6% Standard deviation of excess returns 22.1% 25.9% Required: a. Calculate the following statistics for each stock: (Do not round intermediate calculations. Round your answers to 4 decimal places.) i. Alpha ii. Information ratio iii. Sharpe ratio iv. Treynor measure b. Which stock is the best cheice under the following circumstances? i. This is the only risky asset to be held by the investor. ii. This stock will be mixed with the rest of the investor's portfolio, currently composed solely of holdings in the market-index fund. iii. This iz one of many stocks that the investor is analyzing to form an actively managed stock portfolio. 769 points Skipped References Problem 18-11 (Algo) Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return of each sector of the manager's portfolio in column 1, the fraction of the portfolio allocated to each sector in column 2, the benchmark or neutral sector allocations in column 3, and the returns of sector indices in column 4. Actual Return Actual Weight Benchmark Weight Index Return Equity 2% 8.5 a.4 2.5% (S&P 588) Bonds 1.8 8.3 a.4 2 (Barclay's Aggregate) Cash 0.6 @.2 @.2 8.7 Required: a-1. What was the manager's return in the month? (Do not round intermediate calculations. Input all amounts as positive values. Round your answer to 2 decimal places.) The manager's return in the month is | % a-2. What was her overperformance or underperformance? (Do not round intermediate calculations. Input all amounts as positive values. Round your answer to 2 decimal places.) L % b. What was the contribution of security selection to relative performance? (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of security selection | |% . What was the contribution of asset allocation to relative performance? (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of asset allocation | |% 769 points Skipped References Problem 18-12 (Alge) A global equity manager is assigned to select stocks from a universe of large stocks throughout the world. The manager will be evaluated by comparing her returns to the return on the MSCI World Market Portfelio, but she is free to hold stocks from various countries in whatever proportions she finds desirable. Results for a given month are contained in the following table: Weight In Manager's Manager's Return Return of Stock Index Country MSCI Index Weight in Country for That Country U.K. .29 0.24 22% 15% Japan 8.42 a.2 17 17 U.s. 09.23 8.22 1@ 13 Germany 8.86 0.34 7 15 Required: a. Calculate the total value added of all the manager's decisions this period. (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Added value | % b. Calculate the value added (or subtracted) by her couniry allocation decisions. (Do net round intermediate calculatiens. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of country allocation % <. Calculate the value added from her stock selection ability within countries. (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Contribution of stock selection | %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access with AI-Powered Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance