@ Chrome File Edit View History Bookmarks Profiles Tab Window Help @ @=m T Q & SunMay12 6:28 o0 0 N Netflix x | [

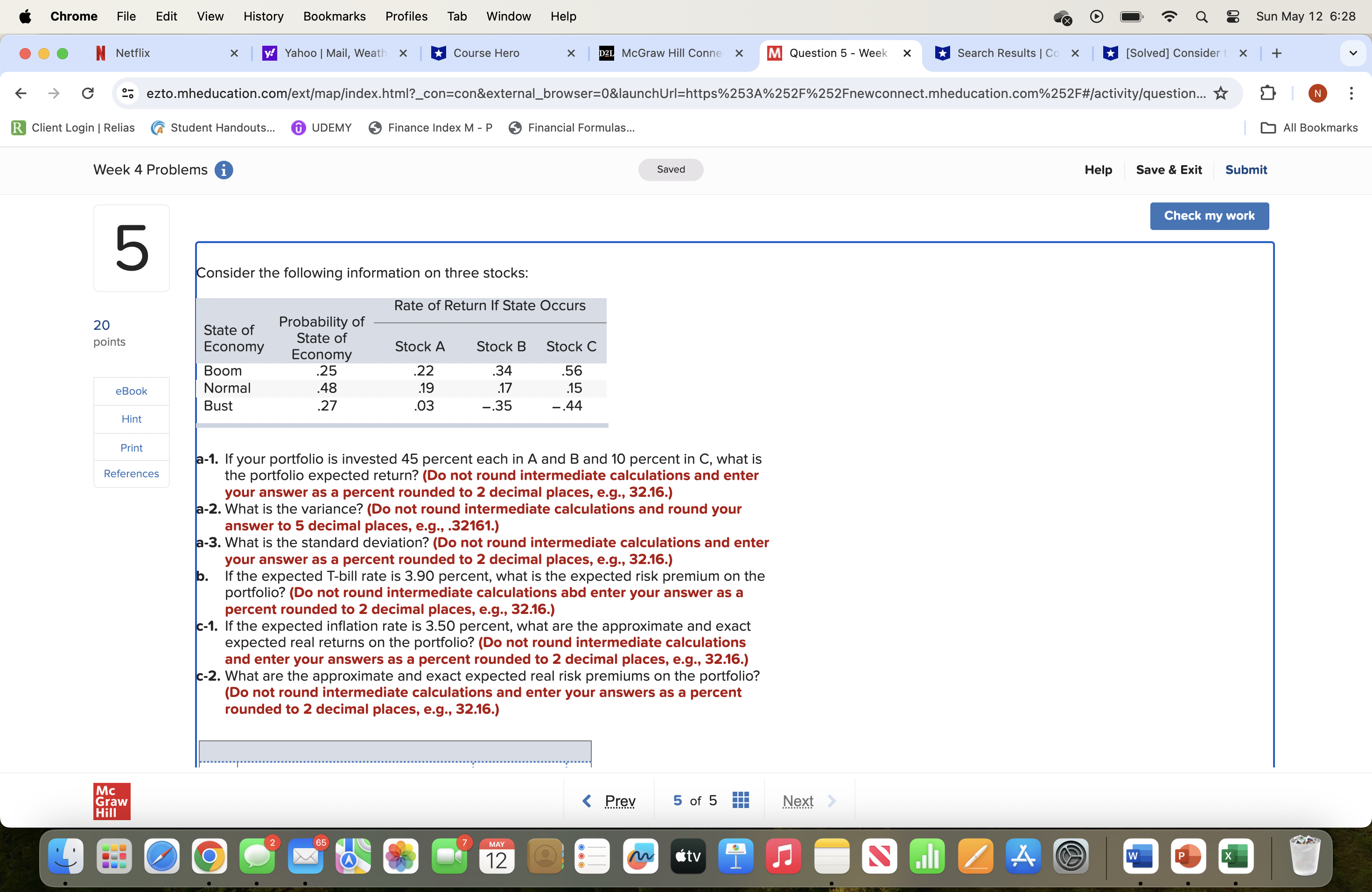

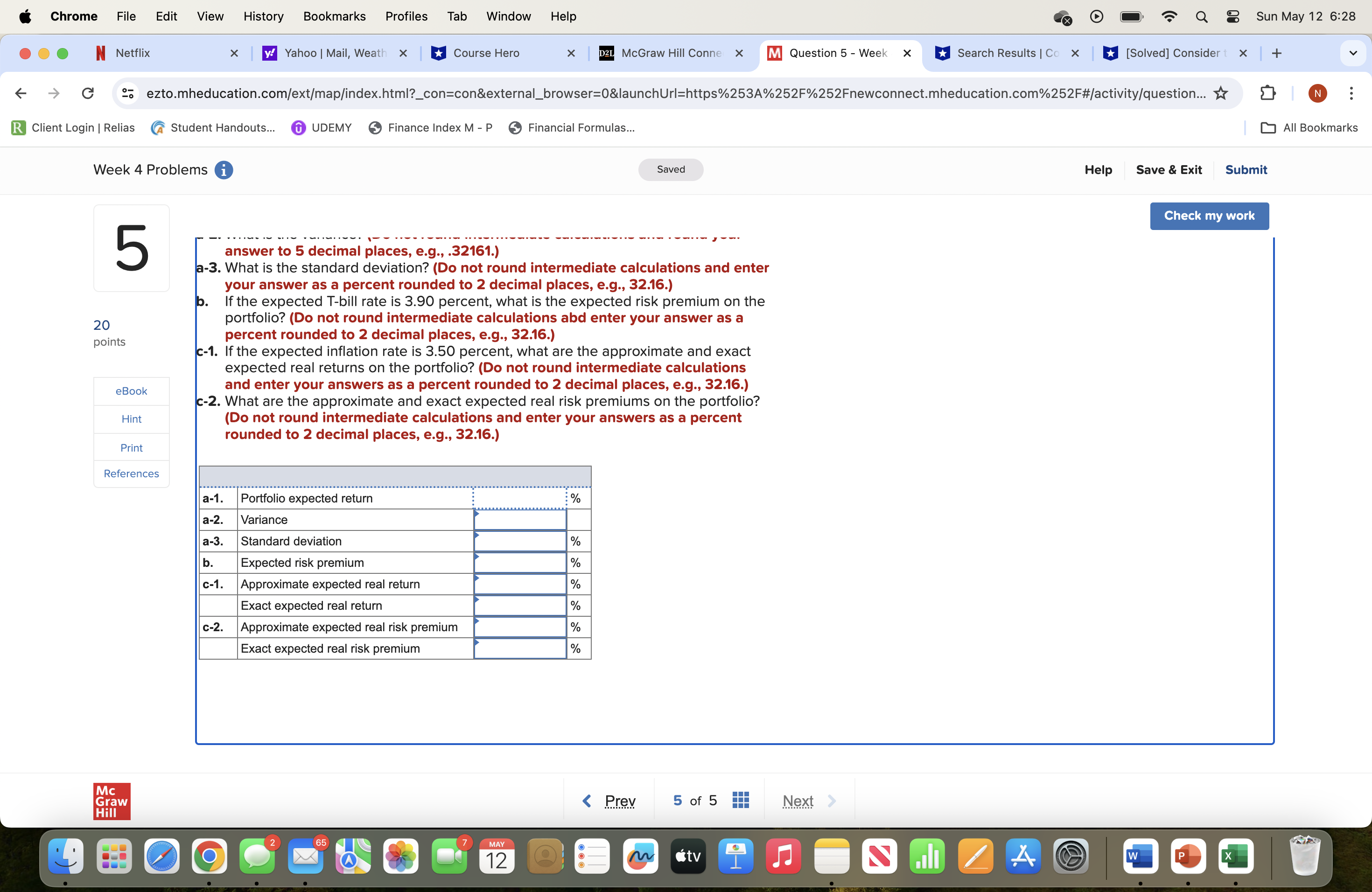

@ Chrome File Edit View History Bookmarks Profiles Tab Window Help @ @=m T Q & SunMay12 6:28 o0 0 N Netflix x | [ Yahoo | Mail, Weat! x | Rd Course Hero x | B McGrawHillConne % [W] Question5-Week x [ SearchResults|Cc x | BJ [Solved] Consider X | + v < 9@ 25 ezto.mheducation.com/ext/map/index.htm|?_con=con&external_browser=08&launchUrl=https%253A%252F%252Fnewconnect.mheducation.com%252F#/activity/question... 3} o % m Client Login | Relias @ Student Handouts... @ UDEMY @ Finance IndexM-P @ Financial Formulas... 3 All Bookmarks Week 4 Problems Saved Help Save & Exit Submit 5 onsider the following information on three stocks: Rate of Return If State Occurs 20_ . State of Prc;t;:gllg it points Economy Economy Stock A Stock B Stock C Boom .25 .22 .34 .56 eBook Normal .48 19 A7 15 Bust .27 .03 -35 -.44 Hint Print -1. If your portfolio is invested 45 percent each in A and B and 10 percent in C, what is References the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) -2. What is the variance? (Do not round intermediate calculations and round your answer to 5 decimal places, e.g., .32161.) -3. What is the standard deviation? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) If the expected T-bill rate is 3.90 percent, what is the expected risk premium on the portfolio? (Do not round intermediate calculations abd enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) -1. If the expected inflation rate is 3.50 percent, what are the approximate and exact expected real returns on the portfolio? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) -2. What are the approximate and exact expected real risk premiums on the portfolio? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) @ Chrome File Edit View History Bookmarks Profiles Tab Window Help o @ T Q & SunMay12 628 0 N Netix > C 25 ezto.mheducation.com/ext/map/index.html?_con=con&external_browser=0&launchUrl=https%253A%252F %252Fnewconnect.mheducation.com%252F#/activity/question... Y& D o 3 x | [ Yahoo | Mail, Weat! x | Rd Course Hero x | B McGraw HillConne X [ Question 5 - Week [} Client Login | Relias (7 Student Handouts... @ UDEMY @ Finance IndexM-P @ Financial Formulas... Week 4 Problems Saved 5 20 points eBook Hint Print References answer to 5 decimal places, e.g., .32161.) -3. What is the standard deviation? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) If the expected T-bill rate is 3.90 percent, what is the expected risk premium on the portfolio? (Do not round intermediate calculations abd enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) -1. If the expected inflation rate is 3.50 percent, what are the approximate and exact expected real returns on the portfolio? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) -2. What are the approximate and exact expected real risk premiums on the portfolio? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) Portfolio expected return Variance Standard deviation Expected risk premium Approximate expected real return Exact expected real return Approximate expected real risk premium Exact expected real risk premium u Search Results | C u [Solved] Consider = X + v 3 All Bookmarks Help Save & Exit Submit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance