Answered step by step

Verified Expert Solution

Question

1 Approved Answer

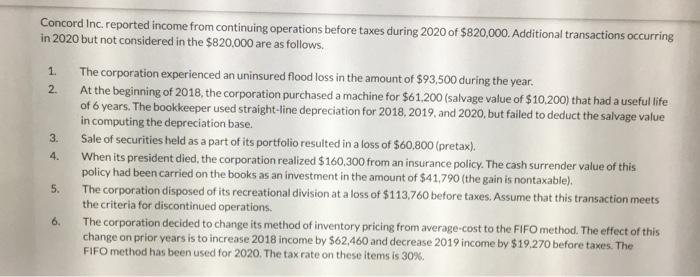

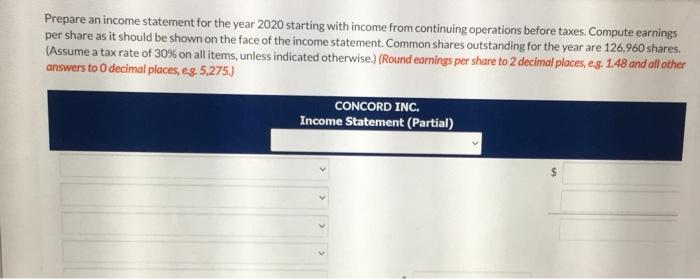

1. 2. Concord Inc. reported income from continuing operations before taxes during 2020 of $820,000. Additional transactions occurring in 2020 but not considered in the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: J. David Spiceland ,Wayne M. Thomas ,Don Herrmann

2nd Revised Edition

0071088385, 978-0071088381