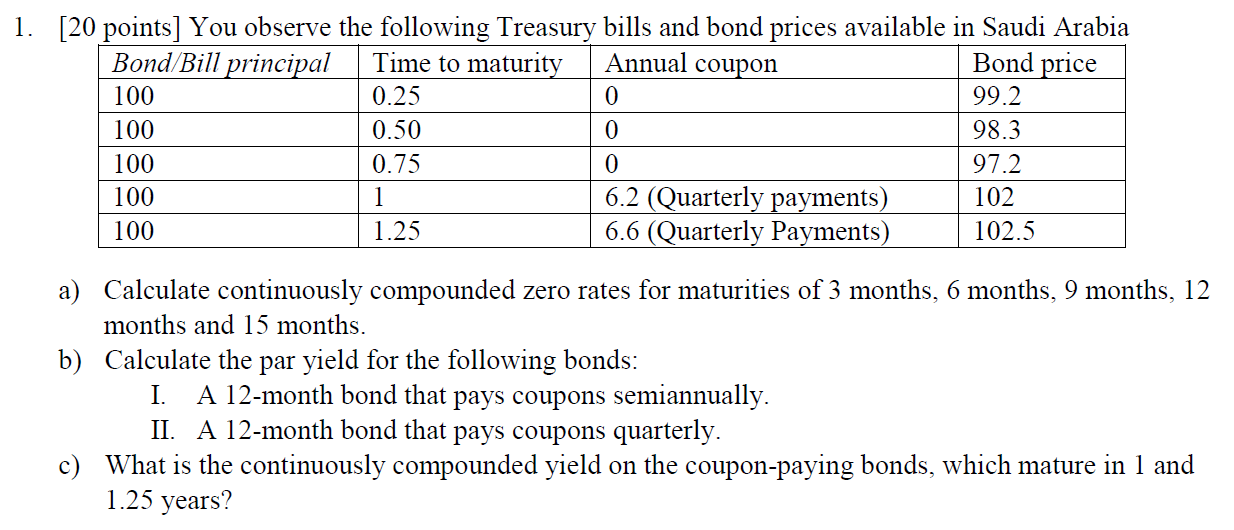

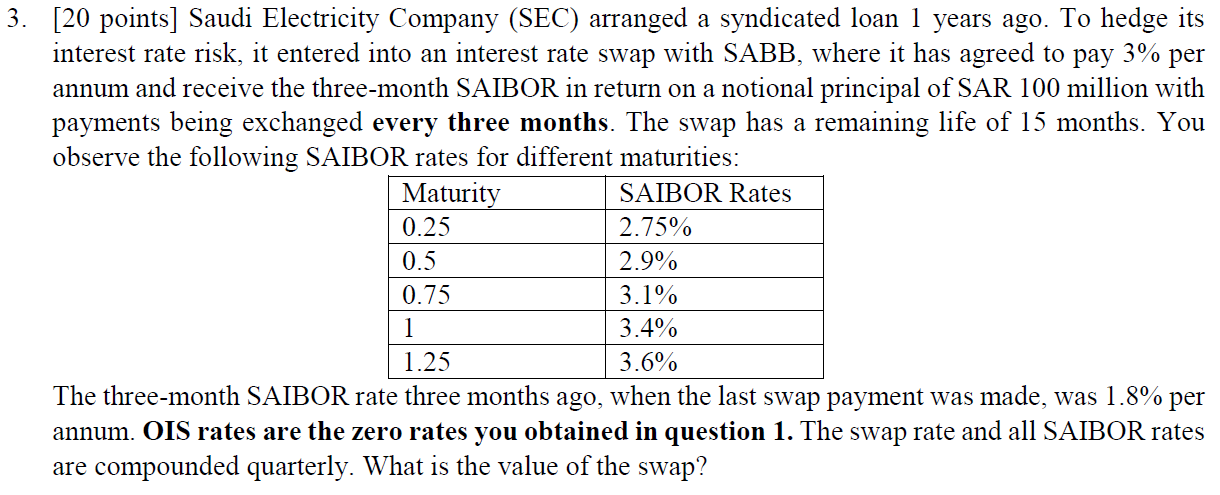

1. [20 points] You observe the following Treasury bills and bond prices available in Saudi Arabia Bond/Bill principal Time to maturity Annual coupon Bond price 100 0.25 0 99.2 100 0.50 98.3 100 0.75 97.2 100 6.2 (Quarterly payments) 102 100 1.25 6.6 (Quarterly Payments) 102.5 0 0 a) Calculate continuously compounded zero rates for maturities of 3 months, 6 months, 9 months, 12 months and 15 months. b) Calculate the par yield for the following bonds: I. A 12-month bond that pays coupons semiannually. II. A 12-month bond that pays coupons quarterly. c) What is the continuously compounded yield on the coupon-paying bonds, which mature in 1 and 1.25 years? 3. [20 points] Saudi Electricity Company (SEC) arranged a syndicated loan 1 years ago. To hedge its interest rate risk, it entered into an interest rate swap with SABB, where it has agreed to pay 3% per annum and receive the three-month SAIBOR in return on a notional principal of SAR 100 million with payments being exchanged every three months. The swap has a remaining life of 15 months. You observe the following SAIBOR rates for different maturities: Maturity SAIBOR Rates 0.25 2.75% 0.5 2.9% 0.75 3.1% 3.4% 1.25 3.6% The three-month SAIBOR rate three months ago, when the last swap payment was made, was 1.8% per annum. OIS rates are the zero rates you obtained in question 1. The swap rate and all SAIBOR rates are compounded quarterly. What is the value of the swap? 4. [15 points] You observed that a trader has entered into an interest rate swap that has a tenor of 1.5 years and payments based on SAR 100 million notional are exchanged every quarter. This swap exchanges SAIBOR rates for a 3.75% fixed rate (again all rates are compounded quarterly). Using the bootstrapping method, what is the 15x18 forward SAIBOR rate if the zero rates and the SAIBOR rate are those in questions 1 and 3 and the 18-month zero rate is 4.7% with continuous compounding. 1. [20 points] You observe the following Treasury bills and bond prices available in Saudi Arabia Bond/Bill principal Time to maturity Annual coupon Bond price 100 0.25 0 99.2 100 0.50 98.3 100 0.75 97.2 100 6.2 (Quarterly payments) 102 100 1.25 6.6 (Quarterly Payments) 102.5 0 0 a) Calculate continuously compounded zero rates for maturities of 3 months, 6 months, 9 months, 12 months and 15 months. b) Calculate the par yield for the following bonds: I. A 12-month bond that pays coupons semiannually. II. A 12-month bond that pays coupons quarterly. c) What is the continuously compounded yield on the coupon-paying bonds, which mature in 1 and 1.25 years? 3. [20 points] Saudi Electricity Company (SEC) arranged a syndicated loan 1 years ago. To hedge its interest rate risk, it entered into an interest rate swap with SABB, where it has agreed to pay 3% per annum and receive the three-month SAIBOR in return on a notional principal of SAR 100 million with payments being exchanged every three months. The swap has a remaining life of 15 months. You observe the following SAIBOR rates for different maturities: Maturity SAIBOR Rates 0.25 2.75% 0.5 2.9% 0.75 3.1% 3.4% 1.25 3.6% The three-month SAIBOR rate three months ago, when the last swap payment was made, was 1.8% per annum. OIS rates are the zero rates you obtained in question 1. The swap rate and all SAIBOR rates are compounded quarterly. What is the value of the swap? 4. [15 points] You observed that a trader has entered into an interest rate swap that has a tenor of 1.5 years and payments based on SAR 100 million notional are exchanged every quarter. This swap exchanges SAIBOR rates for a 3.75% fixed rate (again all rates are compounded quarterly). Using the bootstrapping method, what is the 15x18 forward SAIBOR rate if the zero rates and the SAIBOR rate are those in questions 1 and 3 and the 18-month zero rate is 4.7% with continuous compounding