Answered step by step

Verified Expert Solution

Question

1 Approved Answer

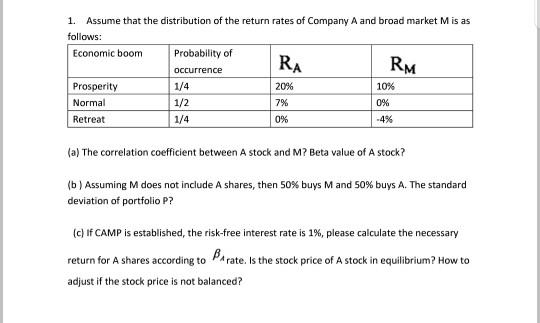

1. Assume that the distribution of the return rates of Company A and broad market M is as follows: Economic boom Probability of occurrence

1. Assume that the distribution of the return rates of Company A and broad market M is as follows: Economic boom Probability of occurrence RA RM Prosperity Normal Retreat 1/4 20% 10% 1/2 1/4 7% 0% 0% -4% (a) The correlation coefficient between A stock and M? Beta value of A stock? (b) Assuming M does not include A shares, then 50% buys M and 50% buys A. The standard deviation of portfolio P? (c) If CAMP is established, the risk-free interest rate is 1%, please calculate the necessary return for A shares according to Prate. Is the stock price of A stock in equilibrium? How to adjust if the stock price is not balanced?

Step by Step Solution

★★★★★

3.52 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Answer a To calculate the correlation coefficient between stock A and the market M we need to use the formula textCorrelation coefficient fractextCovarianceRA RMtextStandard deviationRAtextStandard de...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Precalculus

Authors: Jay Abramson

1st Edition

1938168348, 978-1938168345