Answered step by step

Verified Expert Solution

Question

1 Approved Answer

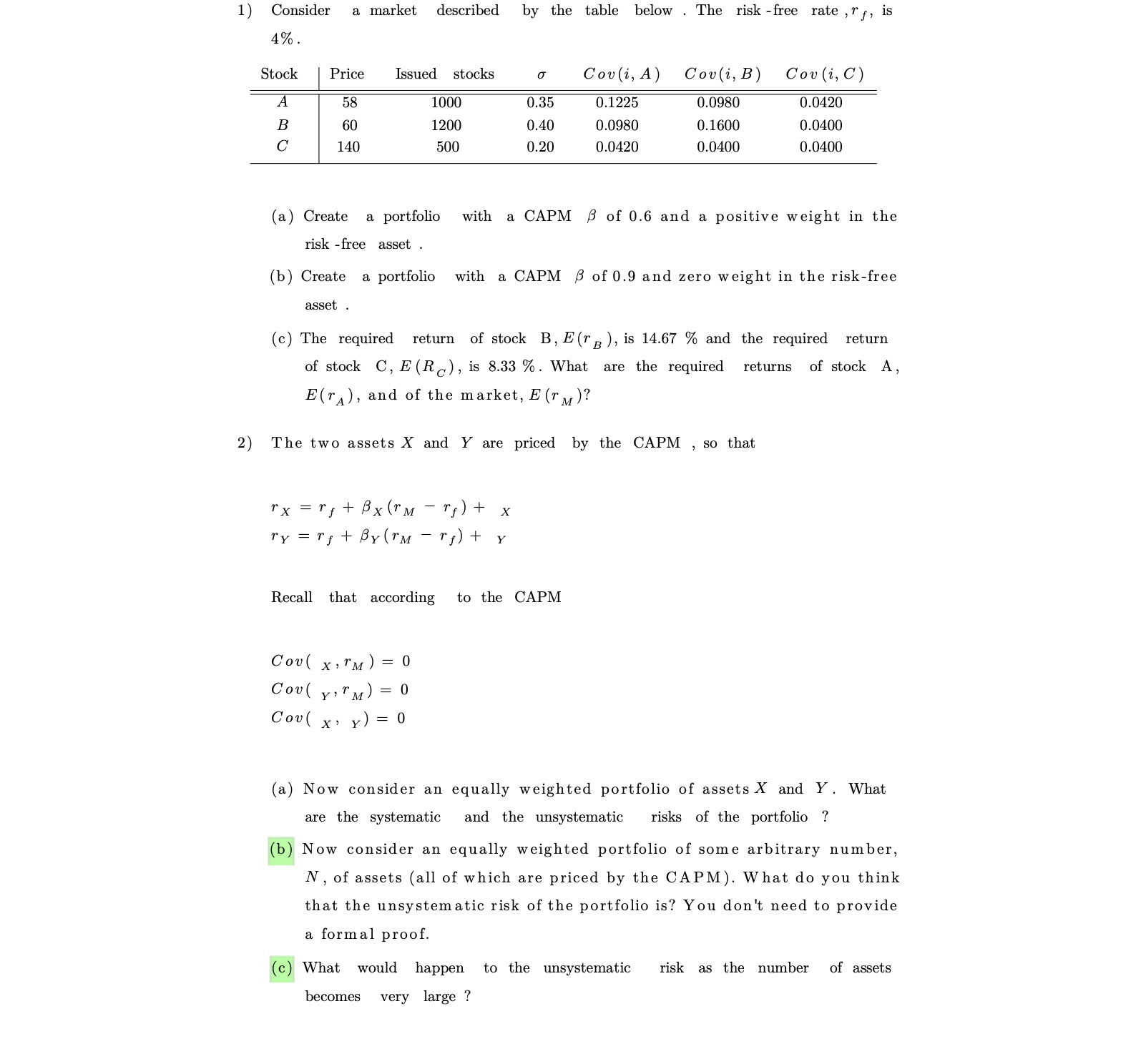

1) Consider a market described by the table below . The risk -free rate , ry, is 4% Stock | Price Issued stocks Cov(i, A)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Inflation, Unemployment And Capital Malformations

Authors: Bernard Schmitt, Xavier Bradley, Alvaro Cencini

1st Edition

0429767064, 9780429767067