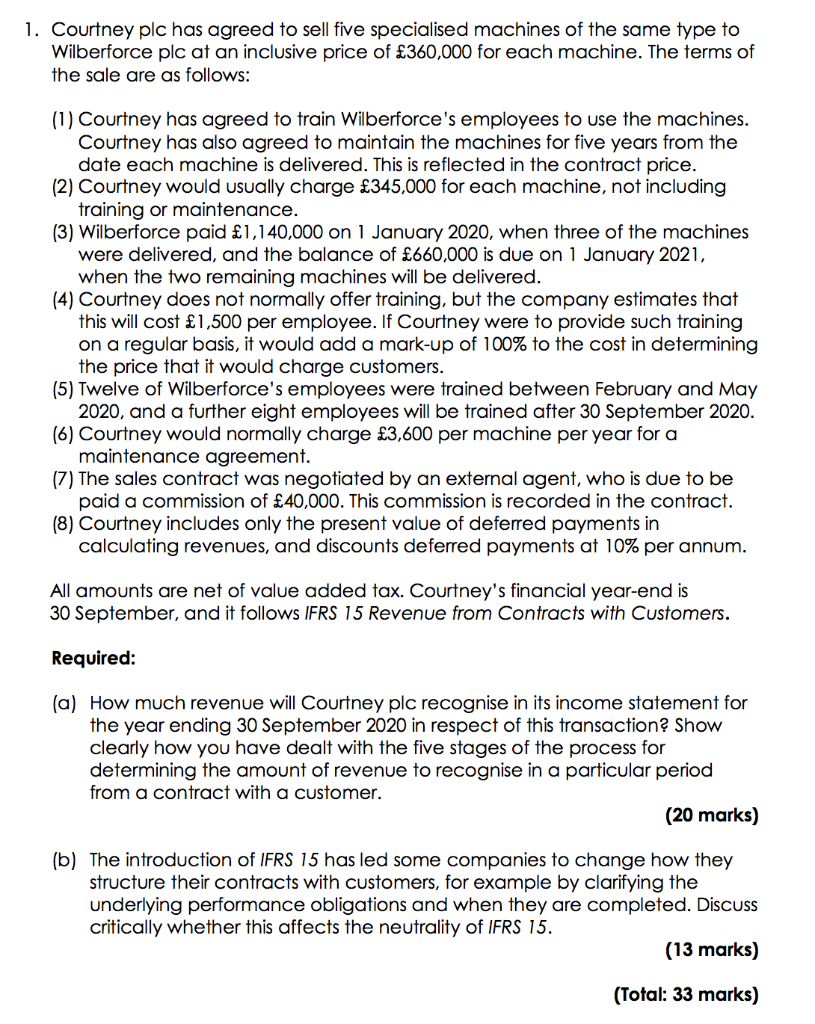

1. Courtney plc has agreed to sell five specialised machines of the same type to Wilberforce plc at an inclusive price of 360,000 for each machine. The terms of the sale are as follows: (1) Courtney has agreed to train Wilberforce's employees to use the machines. Courtney has also agreed to maintain the machines for five years from the date each machine is delivered. This is reflected in the contract price. (2) Courtney would usually charge 345,000 for each machine, not including training or maintenance. (3) Wilberforce paid 1,140,000 on 1 January 2020, when three of the machines were delivered, and the balance of 660,000 is due on 1 January 2021, when the two remaining machines will be delivered. (4) Courtney does not normally offer training, but the company estimates that this will cost 1,500 per employee. If Courtney were to provide such training on a regular basis, it would add a mark-up of 100% to the cost in determining the price that it would charge customers. (5) Twelve of Wilberforce's employees were trained between February and May 2020, and a further eight employees will be trained after 30 September 2020. (6) Courtney would normally charge 3,600 per machine per year for a maintenance agreement. (7) The sales contract was negotiated by an external agent, who is due to be paid a commission of 40,000. This commission is recorded in the contract. (8) Courtney includes only the present value of deferred payments in calculating revenues, and discounts deferred payments at 10% per annum. All amounts are net of value added tax. Courtney's financial year-end is 30 September, and it follows IFRS 15 Revenue from Contracts with Customers. Required: (a) How much revenue will Courtney plc recognise in its income statement for the year ending 30 September 2020 in respect of this transaction? Show clearly how you have dealt with the five stages of the process for determining the amount of revenue to recognise in a particular period from a contract with a customer. (20 marks) (b) The introduction of IFRS 15 has led some companies to change how they structure their contracts with customers, for example by clarifying the underlying performance obligations and when they are completed. Discuss critically whether this affects the neutrality of IFRS 15. (13 marks) (Total: 33 marks) 1. Courtney plc has agreed to sell five specialised machines of the same type to Wilberforce plc at an inclusive price of 360,000 for each machine. The terms of the sale are as follows: (1) Courtney has agreed to train Wilberforce's employees to use the machines. Courtney has also agreed to maintain the machines for five years from the date each machine is delivered. This is reflected in the contract price. (2) Courtney would usually charge 345,000 for each machine, not including training or maintenance. (3) Wilberforce paid 1,140,000 on 1 January 2020, when three of the machines were delivered, and the balance of 660,000 is due on 1 January 2021, when the two remaining machines will be delivered. (4) Courtney does not normally offer training, but the company estimates that this will cost 1,500 per employee. If Courtney were to provide such training on a regular basis, it would add a mark-up of 100% to the cost in determining the price that it would charge customers. (5) Twelve of Wilberforce's employees were trained between February and May 2020, and a further eight employees will be trained after 30 September 2020. (6) Courtney would normally charge 3,600 per machine per year for a maintenance agreement. (7) The sales contract was negotiated by an external agent, who is due to be paid a commission of 40,000. This commission is recorded in the contract. (8) Courtney includes only the present value of deferred payments in calculating revenues, and discounts deferred payments at 10% per annum. All amounts are net of value added tax. Courtney's financial year-end is 30 September, and it follows IFRS 15 Revenue from Contracts with Customers. Required: (a) How much revenue will Courtney plc recognise in its income statement for the year ending 30 September 2020 in respect of this transaction? Show clearly how you have dealt with the five stages of the process for determining the amount of revenue to recognise in a particular period from a contract with a customer. (20 marks) (b) The introduction of IFRS 15 has led some companies to change how they structure their contracts with customers, for example by clarifying the underlying performance obligations and when they are completed. Discuss critically whether this affects the neutrality of IFRS 15. (13 marks) (Total: 33 marks)