Question

1. Debit card/student loans/ checking account 2. For between 500 1000/ without a dollar limitation 3. Whenever its continent/only for emergencies 4. Managing your cash

1. Debit card/student loans/ checking account

2. For between 500 1000/ without a dollar limitation

3. Whenever its continent/only for emergencies

4. Managing your cash wisely/living beyond your means

5. When u decide to write a check for them/ based on a regular disbursement schedule

6. Doesnt/ does require

7. For 25k or more/ without a dollar limitation

8. When you have spare money/ once a year/ once month

9. Size of your home/equity in your home

10. Less/More

Please show work on the calculation part in addition to checking my answers for fill in the blank

11. Increase/Decrease

12. Do/ do not

13. Secured with an additional mortgage on your house/ unsecured

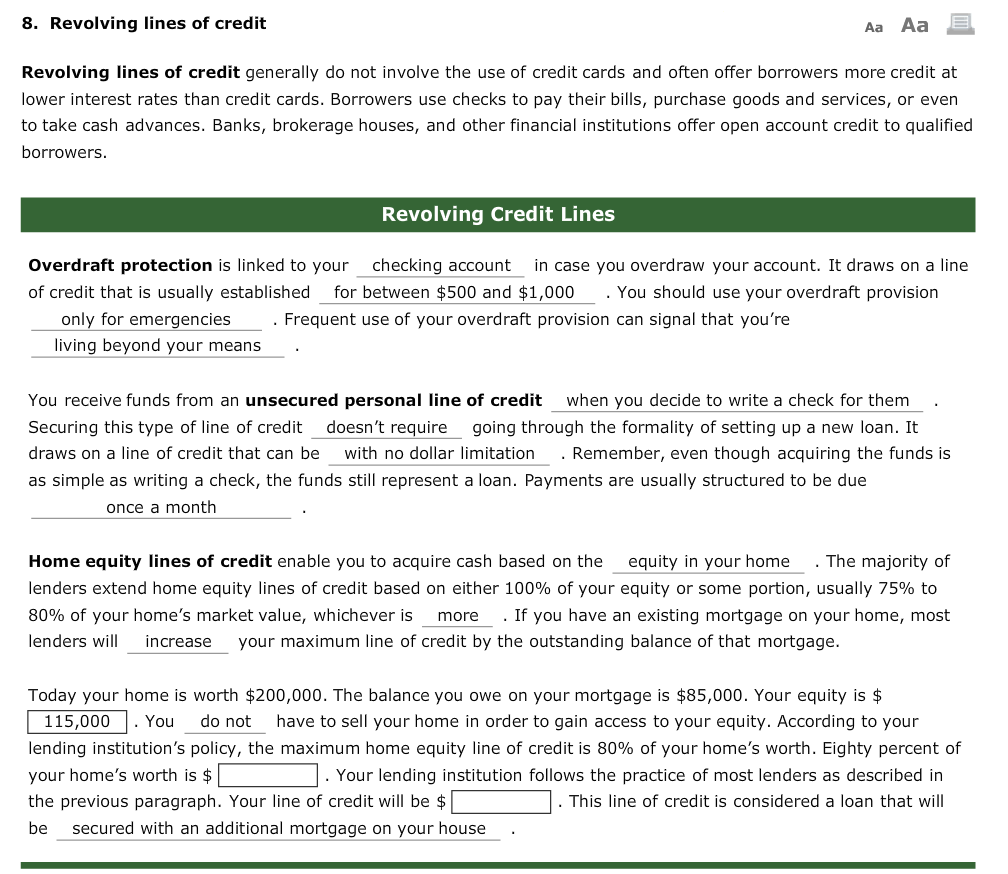

8. Revolving lines of credit Aa Aa E Revolving lines of credit generally do not involve the use of credit cards and often offer borrowers more credit at lower interest rates than credit cards. Borrowers use checks to pay their bills, purchase goods and services, or even to take cash advances. Banks, brokerage houses, and other financial institutions offer open account credit to qualified borrowers. Revolving Credit Lines Overdraft protection is linked to your checking account in case you overdraw your account. It draws on a line of credit that is usually established for between $500 and $1,000 . You should use your overdraft provision only for emergencies Frequent use of your overdraft provision can signal that you're living beyond your means You receive funds from an unsecured personal line of credit when you decide to write a check for them . Securing this type of line of credit doesn't require going through the formality of setting up a new loan. It draws on a line of credit that can be with no dollar limitation Remember, even though acquiring the funds is as simple as writing a check, the funds still represent a loan. Payments are usually structured to be due once a month Home equity lines of credit enable you to acquire cash based on the equity in your home. The majority of lenders extend home equity lines of credit based on either 100% of your equity or some portion, usually 75% to 80% of your home's market value, whichever is more . If you have an existing mortgage on your home, most lenders will increase your maximum line of credit by the outstanding balance of that mortgage. Today your home is worth $200,000. The balance you owe on your mortgage is $85,000. Your equity is $ 115,000 . You do not have to sell your home in order to gain access to your equity. According to your lending institution's policy, the maximum home equity line of credit is 80% of your home's worth. Eighty percent of your home's worth is $ . Your lending institution follows the practice of most lenders as described in the previous paragraph. Your line of credit will be $ 1. This line of credit is considered a loan that will be secured with an additional mortgage on your house 8. Revolving lines of credit Aa Aa E Revolving lines of credit generally do not involve the use of credit cards and often offer borrowers more credit at lower interest rates than credit cards. Borrowers use checks to pay their bills, purchase goods and services, or even to take cash advances. Banks, brokerage houses, and other financial institutions offer open account credit to qualified borrowers. Revolving Credit Lines Overdraft protection is linked to your checking account in case you overdraw your account. It draws on a line of credit that is usually established for between $500 and $1,000 . You should use your overdraft provision only for emergencies Frequent use of your overdraft provision can signal that you're living beyond your means You receive funds from an unsecured personal line of credit when you decide to write a check for them . Securing this type of line of credit doesn't require going through the formality of setting up a new loan. It draws on a line of credit that can be with no dollar limitation Remember, even though acquiring the funds is as simple as writing a check, the funds still represent a loan. Payments are usually structured to be due once a month Home equity lines of credit enable you to acquire cash based on the equity in your home. The majority of lenders extend home equity lines of credit based on either 100% of your equity or some portion, usually 75% to 80% of your home's market value, whichever is more . If you have an existing mortgage on your home, most lenders will increase your maximum line of credit by the outstanding balance of that mortgage. Today your home is worth $200,000. The balance you owe on your mortgage is $85,000. Your equity is $ 115,000 . You do not have to sell your home in order to gain access to your equity. According to your lending institution's policy, the maximum home equity line of credit is 80% of your home's worth. Eighty percent of your home's worth is $ . Your lending institution follows the practice of most lenders as described in the previous paragraph. Your line of credit will be $ 1. This line of credit is considered a loan that will be secured with an additional mortgage on your houseStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance At Work

Authors: Valérie Boussard

1st Edition

113820403X, 978-1138204034