Question

1. Given the mean returns, standard deviations of returns, and correlation coefficient of two risky assets X & Y as follows : Form portfolios from

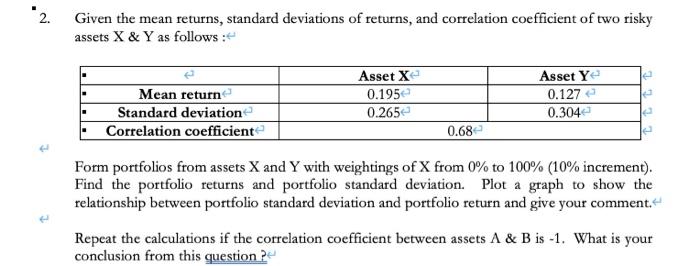

1. Given the mean returns, standard deviations of returns, and correlation coefficient of two risky assets X & Y as follows :

Form portfolios from assets X and Y with weightings of X from 0% to 100% (10% increment). Find the portfolio returns and portfolio standard deviation. Plot a graph to show the relationship between portfolio standard deviation and portfolio return and give your comment.

Repeat the calculations if the correlation coefficient between assets A & B is -1. What is your conclusion from this question ?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Project Finance

Authors: E.R. Yescombe

1st Edition

0127708510, 978-0127708515