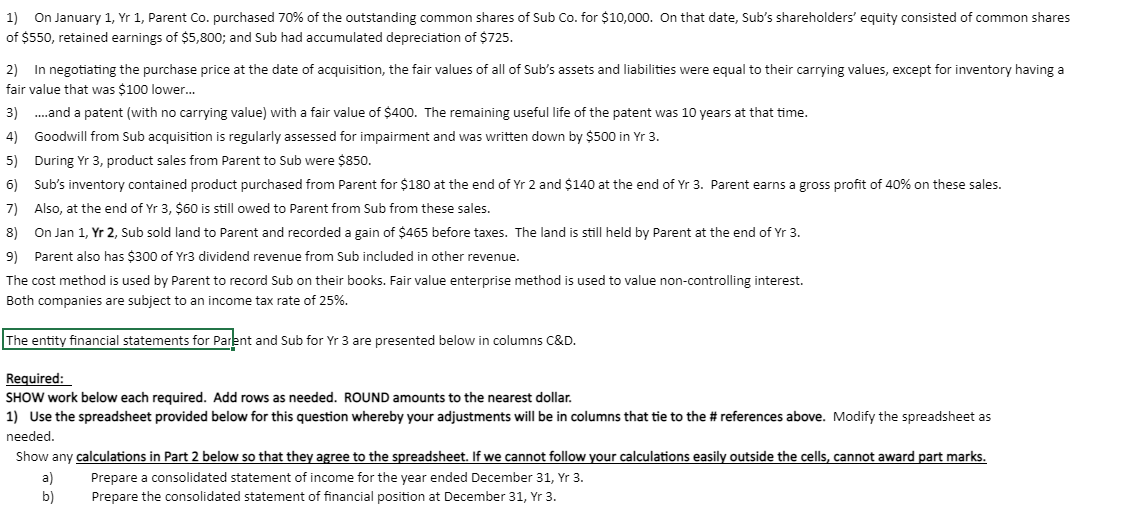

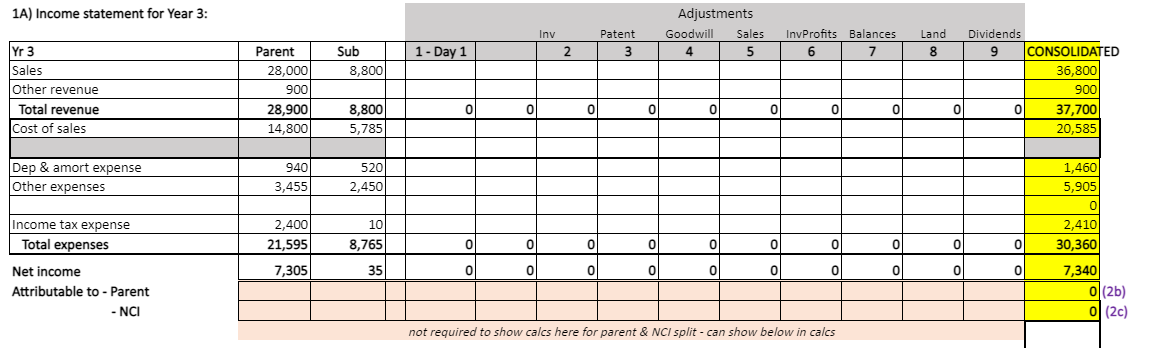

1) On January 1, Yr 1, Parent Co. purchased 70% of the outstanding common shares of Sub Co. for $10,000. On that date, Sub's shareholders' equity consisted of common shares of $550, retained earnings of $5,800; and Sub had accumulated depreciation of $725. 2) In negotiating the purchase price at the date of acquisition, the fair values of all of Sub's assets and liabilities were equal to their carrying values, except for inventory having a fair value that was $100 lower... 3) ....and a patent (with no carrying value) with a fair value of $400. The remaining useful life of the patent was 10 years at that time. 4) Goodwill from Sub acquisition is regularly assessed for impairment and was written down by $500 in Yr 3. 5) During Yr 3, product sales from Parent to Sub were $850. 6) Sub's inventory contained product purchased from Parent for $180 at the end of Yr 2 and $140 at the end of Yr 3. Parent earns a gross profit of 40% on these sales. 7) Also, at the end of yr 3, $60 is still owed to Parent from Sub from these sales. 8) On Jan 1, Yr 2, Sub sold land to Parent and recorded a gain of $465 before taxes. The land is still held by Parent at the end of Yr 3. 9) Parent also has $300 of Yr3 dividend revenue from Sub included in other revenue. The cost method is used by Parent to record Sub on their books. Fair value enterprise method is used to value non-controlling interest. Both companies are subject to an income tax rate of 25%. The entity financial statements for Parent and Sub for Yr 3 are presented below in columns C&D. Required: SHOW work below each required. Add rows as needed. ROUND amounts to the nearest dollar. 1) Use the spreadsheet provided below for this question whereby your adjustments will be in columns that tie to the # references above. Modify the spreadsheet as needed. Show any calculations in Part 2 below so that they agree to the spreadsheet. If we cannot follow your calculations easily outside the cells, cannot award part marks. a) Prepare a consolidated statement of income for the year ended December 31, Yr 3. b) Prepare the consolidated statement of financial position at December 31, Yr 3. 1A) Income statement for Year 3: Inv Patent 3 Adjustments Goodwill Sales 4 5 InvProfits Balances 6 7 Land 8 Parent 1 - Day 1 2 Sub 8,800 Yr 3 Sales Other revenue Total revenue Cost of sales 28,000 900 28,900 14,800 Dividends 9 CONSOLIDATED 36,800 900 0 37,700 20,585 01 0 0 0 0 ol 0 01 0 8,800 5,785 Dep & amort expense Other expenses 9401 3,455 520 2,4501 2,400 21,595 10 8,765 1,460 5,905 0 2,410 30,360 7,340 0 (25) 0 0 0 0 0 0 0 0 Income tax expense Total expenses Net income Attributable to - Parent - NCI 0 7,305 35 0 0 0 0 0 0 0 0 0 0 (20) not required to show calcs here for parent & NCI split - can show below in cales 1B) Balance Sheet at Dec 31, Yr 3: Inv Patent 3 Goodwill 4 Sales 5 Parent 1 - Day 1 2 Cash Accounts Receivable Inventory Land PP&E-cost - accum depreciation Investment in Sub 2,000 4,200 5,930 3,000 8,000 (2,865) 10,000 Sub 800 1,950 4,100 780 3,450 (1,320) InvProfits Balances LandProfit Dividends 6 7 8 9 CONSOLIDATED 2,800 6,150 10,030 3,780 11,450 (4,185 10,000 0 0 0 0 Total 30,265 9,760 0 0 40,025 Accounts payable Other liabilities Common shares Retained earnings Non-controlling interest Total 2,100 2,250 2,000 23,915 940 1,540 550 6,730 3,040 3,7901 2,550 30,645 (20) 0 (2) 40,025 30,265 9,760 0 0 0 0 0 ol 0 not required to break out R/E & NCI calculations here if show in part 2(d) & (e) 2) Show Calculations for: (add rows as needed) A) Goodwill: B) Income attributable to Parent C) Income/(loss) attributable to NCI D) Consolidated Retained earnings Dec 31, Year 3 E) Non-controlling interest Dec 31, Year 3 F) Other calculations, (ie intercompany profits) 1) On January 1, Yr 1, Parent Co. purchased 70% of the outstanding common shares of Sub Co. for $10,000. On that date, Sub's shareholders' equity consisted of common shares of $550, retained earnings of $5,800; and Sub had accumulated depreciation of $725. 2) In negotiating the purchase price at the date of acquisition, the fair values of all of Sub's assets and liabilities were equal to their carrying values, except for inventory having a fair value that was $100 lower... 3) ....and a patent (with no carrying value) with a fair value of $400. The remaining useful life of the patent was 10 years at that time. 4) Goodwill from Sub acquisition is regularly assessed for impairment and was written down by $500 in Yr 3. 5) During Yr 3, product sales from Parent to Sub were $850. 6) Sub's inventory contained product purchased from Parent for $180 at the end of Yr 2 and $140 at the end of Yr 3. Parent earns a gross profit of 40% on these sales. 7) Also, at the end of yr 3, $60 is still owed to Parent from Sub from these sales. 8) On Jan 1, Yr 2, Sub sold land to Parent and recorded a gain of $465 before taxes. The land is still held by Parent at the end of Yr 3. 9) Parent also has $300 of Yr3 dividend revenue from Sub included in other revenue. The cost method is used by Parent to record Sub on their books. Fair value enterprise method is used to value non-controlling interest. Both companies are subject to an income tax rate of 25%. The entity financial statements for Parent and Sub for Yr 3 are presented below in columns C&D. Required: SHOW work below each required. Add rows as needed. ROUND amounts to the nearest dollar. 1) Use the spreadsheet provided below for this question whereby your adjustments will be in columns that tie to the # references above. Modify the spreadsheet as needed. Show any calculations in Part 2 below so that they agree to the spreadsheet. If we cannot follow your calculations easily outside the cells, cannot award part marks. a) Prepare a consolidated statement of income for the year ended December 31, Yr 3. b) Prepare the consolidated statement of financial position at December 31, Yr 3. 1A) Income statement for Year 3: Inv Patent 3 Adjustments Goodwill Sales 4 5 InvProfits Balances 6 7 Land 8 Parent 1 - Day 1 2 Sub 8,800 Yr 3 Sales Other revenue Total revenue Cost of sales 28,000 900 28,900 14,800 Dividends 9 CONSOLIDATED 36,800 900 0 37,700 20,585 01 0 0 0 0 ol 0 01 0 8,800 5,785 Dep & amort expense Other expenses 9401 3,455 520 2,4501 2,400 21,595 10 8,765 1,460 5,905 0 2,410 30,360 7,340 0 (25) 0 0 0 0 0 0 0 0 Income tax expense Total expenses Net income Attributable to - Parent - NCI 0 7,305 35 0 0 0 0 0 0 0 0 0 0 (20) not required to show calcs here for parent & NCI split - can show below in cales 1B) Balance Sheet at Dec 31, Yr 3: Inv Patent 3 Goodwill 4 Sales 5 Parent 1 - Day 1 2 Cash Accounts Receivable Inventory Land PP&E-cost - accum depreciation Investment in Sub 2,000 4,200 5,930 3,000 8,000 (2,865) 10,000 Sub 800 1,950 4,100 780 3,450 (1,320) InvProfits Balances LandProfit Dividends 6 7 8 9 CONSOLIDATED 2,800 6,150 10,030 3,780 11,450 (4,185 10,000 0 0 0 0 Total 30,265 9,760 0 0 40,025 Accounts payable Other liabilities Common shares Retained earnings Non-controlling interest Total 2,100 2,250 2,000 23,915 940 1,540 550 6,730 3,040 3,7901 2,550 30,645 (20) 0 (2) 40,025 30,265 9,760 0 0 0 0 0 ol 0 not required to break out R/E & NCI calculations here if show in part 2(d) & (e) 2) Show Calculations for: (add rows as needed) A) Goodwill: B) Income attributable to Parent C) Income/(loss) attributable to NCI D) Consolidated Retained earnings Dec 31, Year 3 E) Non-controlling interest Dec 31, Year 3 F) Other calculations, (ie intercompany profits)