Answered step by step

Verified Expert Solution

Question

1 Approved Answer

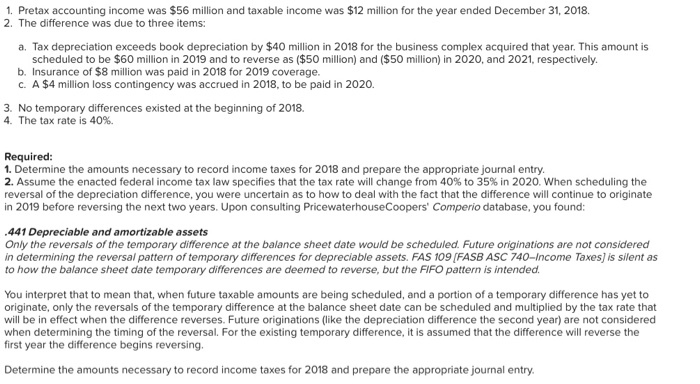

1. Pretax accounting income was $56 million and taxable income was $12 million for the year ended December 31, 2018. 2. The difference was due

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISO 27001 Lead Auditor Study Guide Achieving Excellence In Information Security The Ultimate ISO 27001 Lead Auditor Preparation Handbook

Authors: Erik Rorstrom

1st Edition

B0BZFC9776, 979-8388407726