Answered step by step

Verified Expert Solution

Question

1 Approved Answer

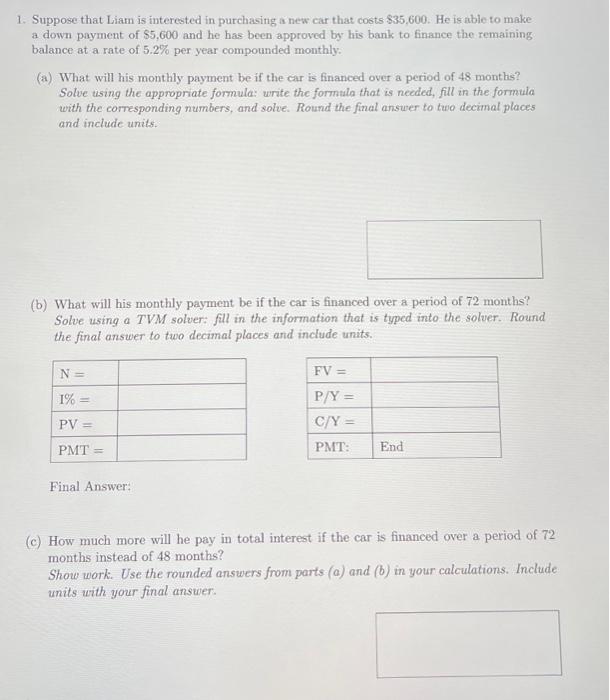

1. Suppose that Liam is interested in purchasing a new car that costs $35,600. He is able to make a down payment of $5,600 and

1. Suppose that Liam is interested in purchasing a new car that costs $35,600. He is able to make a down payment of $5,600 and he has been approved by his bank to finance the remaining balance at a rate of 5.2% per year compounded monthly. (a) What will his monthly payment be if the car is financed over a period of 48 months? Solve using the appropriate formula: write the formula that is needed, fill in the formula with the corresponding numbers, and solve. Round the final answer to two decimal places and include units. (b) What will his monthly payment be if the car is financed over a period of 72 months? Solve using a TVM solver: fill in the information that is typed into the solver. Round the final answer to two decimal places and include units. N = 1% = PV = PMT = Final Answer: FV = P/Y = C/Y = PMT: End (c) How much more will he pay in total interest if the car is financed over a period of 72 months instead of 48 months? Show work. Use the rounded answers from parts (a) and (b) in your calculations. Include units with your final answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Funds Private Equity Hedge And All Core Structures

Authors: Matthew Hudson

1st Edition

1118790405, 978-1118790403