Answered step by step

Verified Expert Solution

Question

1 Approved Answer

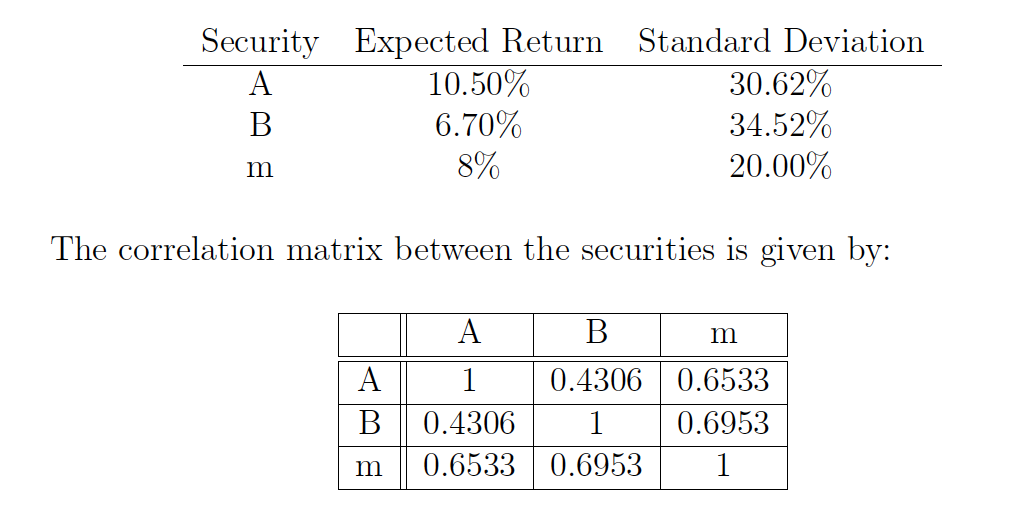

1. Suppose that you have the return to a securities A and B and the market portfolio m. You have the following information about these

1. Suppose that you have the return to a securities \A" and \B" and the

market portfolio \m." You have the following information about these

three securities:

(See picture attached)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Economics and Business Strategy

Authors: Michael R. baye

7th Edition

978-0073375960, 71267441, 73375969, 978-0071267441