Answered step by step

Verified Expert Solution

Question

1 Approved Answer

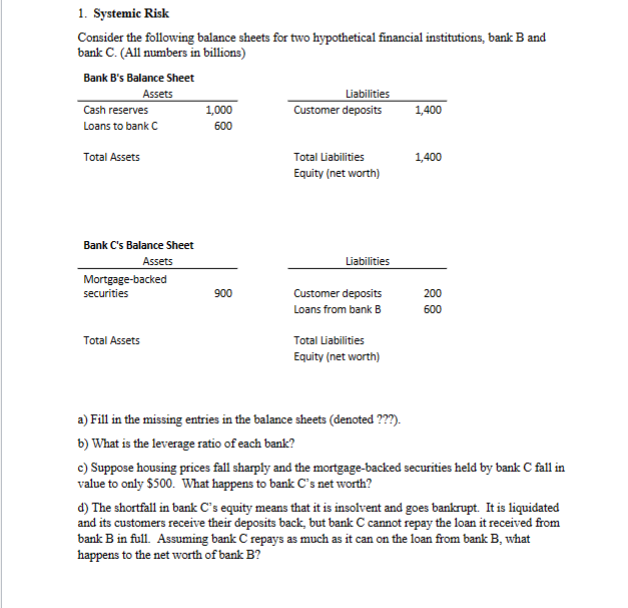

1. Systemic Risk Consider the following balance sheets for two hypothetical financial institutions, bank B and bank C. (All numbers in billions) a) Fill in

1. Systemic Risk Consider the following balance sheets for two hypothetical financial institutions, bank B and bank C. (All numbers in billions) a) Fill in the missing entries in the balance sheets (denoted ???). b) What is the leverage ratio of each bank? c) Suppose housing prices fall sharply and the mortgage-backed securities held by bank C fall in value to only $500. What happens to bank Cs net worth? d) The shortfall in bank C 's equity means that it is insolvent and goes bankrupt. It is liquidated and its customers receive their deposits back, but bank C cannot repay the loan it received from bank B in full. Assuming bank C repays as much as it can on the loan from bank B, what happens to the net worth of bank B

1. Systemic Risk Consider the following balance sheets for two hypothetical financial institutions, bank B and bank C. (All numbers in billions) a) Fill in the missing entries in the balance sheets (denoted ???). b) What is the leverage ratio of each bank? c) Suppose housing prices fall sharply and the mortgage-backed securities held by bank C fall in value to only $500. What happens to bank Cs net worth? d) The shortfall in bank C 's equity means that it is insolvent and goes bankrupt. It is liquidated and its customers receive their deposits back, but bank C cannot repay the loan it received from bank B in full. Assuming bank C repays as much as it can on the loan from bank B, what happens to the net worth of bank B Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi

2nd Edition

0471012556, 978-0471012559