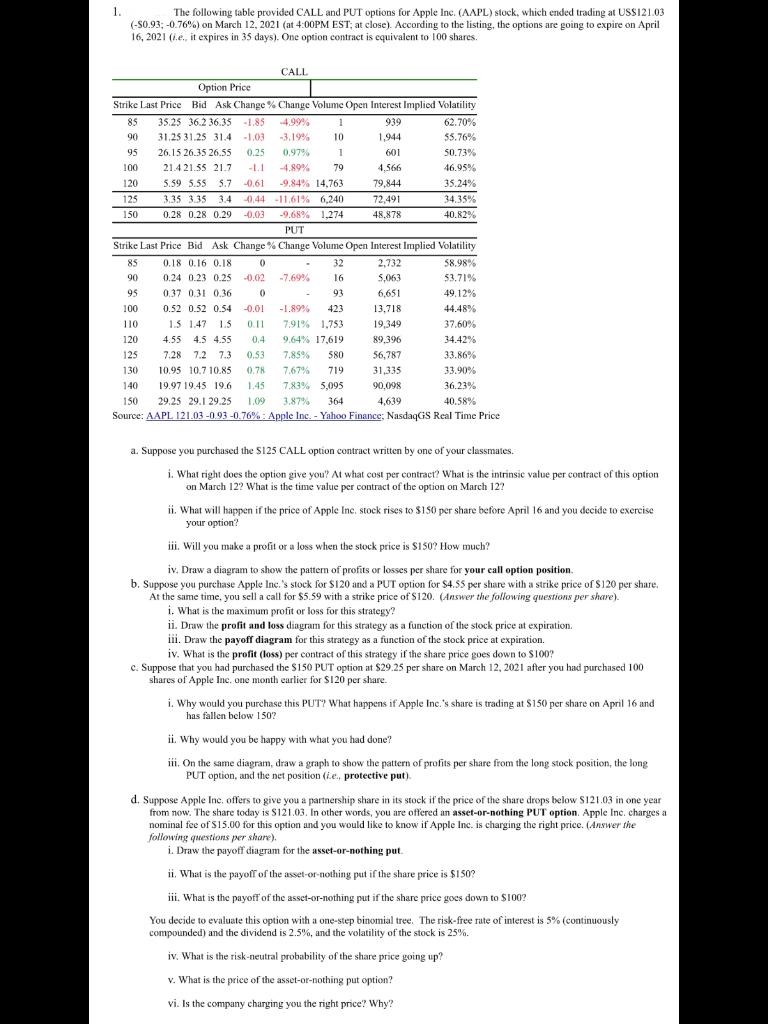

1. The following table provided CALL and PUT options for Apple Inc. (AAPL) stock, which ended trading at US$121.03 (-50.93; -0.76%) on March 12, 2021 (at 4:00PM EST, at close). According to the listing, the options are going to expire on April 16, 2021 (1.e. it expires in 35 days). One option contract is equivalent to 100 shares. $0.73% CALL Option Price Strike Last Price Bid Ask Change % Change Volume Open Interest Implied Volatility 85 35.25 36.2 36.35 -1.85 4.99% 1 939 62.70% 90 31.25 31.25 31.4 -1.03 -3.19% 10 1,944 55.76% 95 26.15 26.35 26.55 0.25 0.97% 1 601 100 21.4 21.55 21.7 -11 -4.89% 79 4,566 46.95% 120 5.59 5.55 5.7 -0.61 -9.84% 14,763 79,844 35.24% 125 3.35 3.35 3.4 -0,44 -0.44 -11.61% 6,240 72.491 34.35% 150 0.28 0.28 0.29 -0.03 -9.68% 1.274 48.878 40.82% PUT Strike Last Price Bid Ask Change % Change Volume Open Interest Implied Volatility 85 0.18 0.16 0.18 0 32 2,732 58.98% 90 0.24 0.23 0.25 -0.02 -7.69% 16 5,063 53.71% 95 0.37 0.31 0.36 0 93 6.651 49.12% 100 0.52 0.52 0.54 -0.01 -1.89% 423 13.718 44.48% 110 1.5 1.47 1.5 0.11 7.91% 1.753 19,349 37.60% 120 4.55 4.5 4.55 0.4 9.64% 17,619 89.396 34.42% 125 7.28 7.2 7.3 0.53 7.85% 580 56,787 33.86% 130 10.95 10.7 10.85 0.78 7.67% 719 31,335 33.90% 140 19.97 19.45 19.6 1.45 7.83% 5,095 90,098 36.23% 150 29.25 29.129.25 1.09 3.87% 364 4,639 40.58% Source: AAPL 121.03 -0.93 -0.76%: Apple Inc. - Yahoo Finance, NasdaqGS Real Time Price a. Suppose you purchased the S125 CALL option contract written by one of your classmates. 1. What right does the option give you? At what cost per contract? What is the intrinsic value per contract of this option on March 12? What is the time value per contract of the option on March 12? i. What will happen if the price of Apple Inc. stock rises to $150 per share before April 16 and you decide to exercise your option? iii. Will you make a profit or a loss when the stock price is $150? How much? iv. Draw a diagram to show the pattern of profits or losses per share for your call option position. b. Suppose you purchase Apple Inc.'s stock for S120 and a PUT option for $4.55 per share with a strike price of S120 per share, At the same time, you sell a call for $5.59 with a strike price of S120. (Answer the following questions per share). i. What is the maximum profit or loss for this strategy? ii. Draw the profit and loss diagram for this strategy as a function of the stock price at expiration iii. Draw the payoff diagram for this strategy as a function of the stock price at expiration. iv. What is the profit (loss) per contract of this strategy if the share price goes down to S100? c. Suppose that you had purchased the $150 PUT option at $29.25 per share on March 12, 2021 after you had purchased 100 shares of Apple Inc. one month earlier for $120 per share. i. Why would you purchase this PUT? What happens if Apple Inc.'s share is trading at $150 per share on April 16 and has fallen below 150? ii. Why would you be happy with what you had done? iii. On the same diagram, draw a graph to show the pattern of profits per share from the long stock position, the long PUT option, and the net position (ie, protective put) d. Suppose Apple Inc. offers to give you a partnership share in its stock if the price of the share drops below S121.03 in one year from now. The share today is $121.03. In other words, you are offered an asset-or-nothing PUT option Apple Inc. charges a nominal fee of $15.00 for this option and you would like to know if Apple Inc. is charging the right price.(Answer the following questions per share), i. Draw the payoff diagram for the asset-or-nothing put 1. What is the payoff of the asset-or-nothing put if the share price is $150? iii. What is the payoff of the asset-or-nothing put if the share price goes down to $100? You decide to evaluate this option with a one-step binomial tree. The risk-free rate of interest is 5% (continuously compounded) and the dividend is 2.5%, and the volatility of the stock is 25%. iv. What is the risk-neutral probability of the share price going up? v. What is the price of the asset-or-nothing put option? vi. Is the company charging you the right price? Why