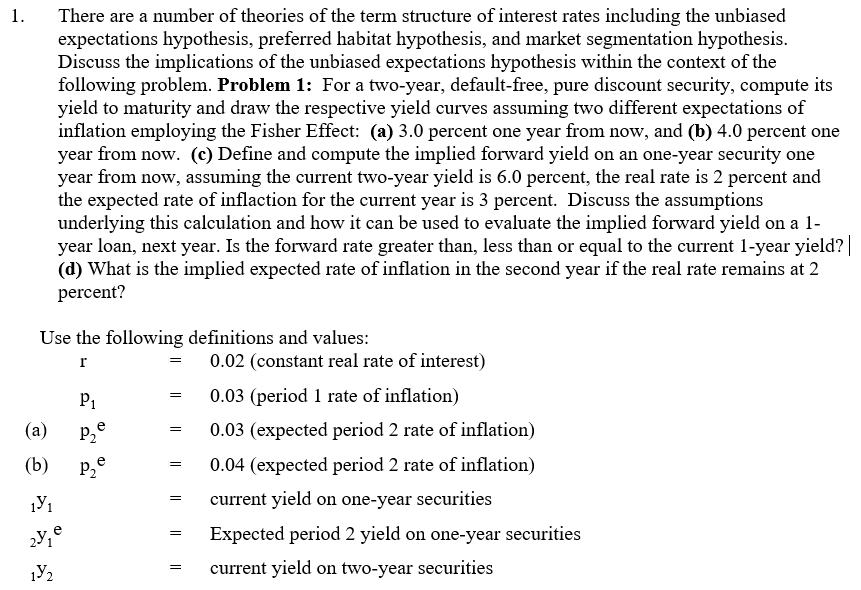

1. There are a number of theories of the term structure of interest rates including the unbiased expectations hypothesis, preferred habitat hypothesis, and market segmentation hypothesis. Discuss the implications of the unbiased expectations hypothesis within the context of the following problem. Problem 1: For a two-year, default-free, pure discount security, compute its yield to maturity and draw the respective yield curves assuming two different expectations of inflation employing the Fisher Effect: (a) 3.0 percent one year from now, and (b) 4.0 percent one year from now. (c) Define and compute the implied forward yield on an one-year security one year from now, assuming the current two-year yield is 6.0 percent, the real rate is 2 percent and the expected rate of inflaction for the current year is 3 percent. Discuss the assumptions underlying this calculation and how it can be used to evaluate the implied forward yield on a 1- year loan, next year. Is the forward rate greater than, less than or equal to the current 1-year yield? | (d) What is the implied expected rate of inflation in the second year if the real rate remains at 2 percent? P, Use the following definitions and values: = 0.02 (constant real rate of interest) P1 0.03 (period 1 rate of inflation) (a) 0.03 (expected period 2 rate of inflation) (6) 0.04 (expected period 2 rate of inflation) 19 current yield on one-year securities Expected period 2 yield on one-year securities 192 current yield on two-year securities = P2 2y, 1. There are a number of theories of the term structure of interest rates including the unbiased expectations hypothesis, preferred habitat hypothesis, and market segmentation hypothesis. Discuss the implications of the unbiased expectations hypothesis within the context of the following problem. Problem 1: For a two-year, default-free, pure discount security, compute its yield to maturity and draw the respective yield curves assuming two different expectations of inflation employing the Fisher Effect: (a) 3.0 percent one year from now, and (b) 4.0 percent one year from now. (c) Define and compute the implied forward yield on an one-year security one year from now, assuming the current two-year yield is 6.0 percent, the real rate is 2 percent and the expected rate of inflaction for the current year is 3 percent. Discuss the assumptions underlying this calculation and how it can be used to evaluate the implied forward yield on a 1- year loan, next year. Is the forward rate greater than, less than or equal to the current 1-year yield? | (d) What is the implied expected rate of inflation in the second year if the real rate remains at 2 percent? P, Use the following definitions and values: = 0.02 (constant real rate of interest) P1 0.03 (period 1 rate of inflation) (a) 0.03 (expected period 2 rate of inflation) (6) 0.04 (expected period 2 rate of inflation) 19 current yield on one-year securities Expected period 2 yield on one-year securities 192 current yield on two-year securities = P2 2y