Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. We have a Put with an exercise price X=$50 selling at a put price of $6, a Call with an exercise price X=$60 selling

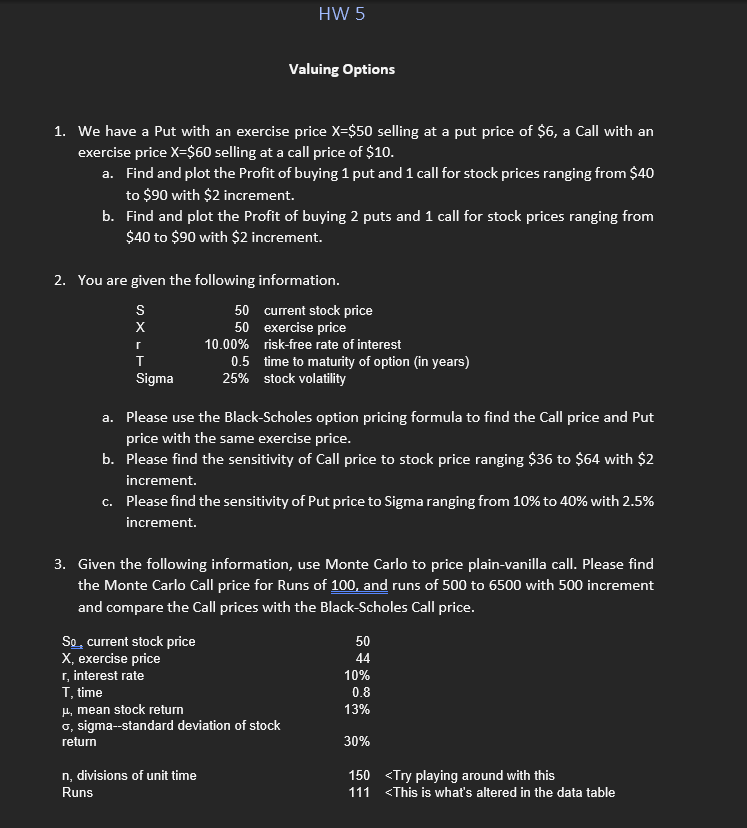

1. We have a Put with an exercise price X=$50 selling at a put price of $6, a Call with an exercise price X=$60 selling at a call price of $10. a. Find and plot the Profit of buying 1 put and 1 call for stock prices ranging from $40 to $90 with $2 increment. b. Find and plot the Profit of buying 2 puts and 1 call for stock prices ranging from $40 to $90 with $2 increment. 2. You are given the following information. SXrTSigma505010.00%0.525%currentstockpriceexercisepricerisk-freerateofinteresttimetomaturityofoption(inyears)stockvolatility a. Please use the Black-Scholes option pricing formula to find the Call price and Put price with the same exercise price. b. Please find the sensitivity of Call price to stock price ranging $36 to $64 with $2 increment. c. Please find the sensitivity of Put price to Sigma ranging from 10% to 40% with 2.5% increment. 3. Given the following information, use Monte Carlo to price plain-vanilla call. Please find the Monte Carlo Call price for Runs of 100 , and runs of 500 to 6500 with 500 increment and compare the Call prices with the Black-Scholes Call price. 1. We have a Put with an exercise price X=$50 selling at a put price of $6, a Call with an exercise price X=$60 selling at a call price of $10. a. Find and plot the Profit of buying 1 put and 1 call for stock prices ranging from $40 to $90 with $2 increment. b. Find and plot the Profit of buying 2 puts and 1 call for stock prices ranging from $40 to $90 with $2 increment. 2. You are given the following information. SXrTSigma505010.00%0.525%currentstockpriceexercisepricerisk-freerateofinteresttimetomaturityofoption(inyears)stockvolatility a. Please use the Black-Scholes option pricing formula to find the Call price and Put price with the same exercise price. b. Please find the sensitivity of Call price to stock price ranging $36 to $64 with $2 increment. c. Please find the sensitivity of Put price to Sigma ranging from 10% to 40% with 2.5% increment. 3. Given the following information, use Monte Carlo to price plain-vanilla call. Please find the Monte Carlo Call price for Runs of 100 , and runs of 500 to 6500 with 500 increment and compare the Call prices with the Black-Scholes Call price

1. We have a Put with an exercise price X=$50 selling at a put price of $6, a Call with an exercise price X=$60 selling at a call price of $10. a. Find and plot the Profit of buying 1 put and 1 call for stock prices ranging from $40 to $90 with $2 increment. b. Find and plot the Profit of buying 2 puts and 1 call for stock prices ranging from $40 to $90 with $2 increment. 2. You are given the following information. SXrTSigma505010.00%0.525%currentstockpriceexercisepricerisk-freerateofinteresttimetomaturityofoption(inyears)stockvolatility a. Please use the Black-Scholes option pricing formula to find the Call price and Put price with the same exercise price. b. Please find the sensitivity of Call price to stock price ranging $36 to $64 with $2 increment. c. Please find the sensitivity of Put price to Sigma ranging from 10% to 40% with 2.5% increment. 3. Given the following information, use Monte Carlo to price plain-vanilla call. Please find the Monte Carlo Call price for Runs of 100 , and runs of 500 to 6500 with 500 increment and compare the Call prices with the Black-Scholes Call price. 1. We have a Put with an exercise price X=$50 selling at a put price of $6, a Call with an exercise price X=$60 selling at a call price of $10. a. Find and plot the Profit of buying 1 put and 1 call for stock prices ranging from $40 to $90 with $2 increment. b. Find and plot the Profit of buying 2 puts and 1 call for stock prices ranging from $40 to $90 with $2 increment. 2. You are given the following information. SXrTSigma505010.00%0.525%currentstockpriceexercisepricerisk-freerateofinteresttimetomaturityofoption(inyears)stockvolatility a. Please use the Black-Scholes option pricing formula to find the Call price and Put price with the same exercise price. b. Please find the sensitivity of Call price to stock price ranging $36 to $64 with $2 increment. c. Please find the sensitivity of Put price to Sigma ranging from 10% to 40% with 2.5% increment. 3. Given the following information, use Monte Carlo to price plain-vanilla call. Please find the Monte Carlo Call price for Runs of 100 , and runs of 500 to 6500 with 500 increment and compare the Call prices with the Black-Scholes Call price Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started