Question

1.) What is the total equivalent units of production for conversion to Department X? 2.) What is the percentage of completion (work done) for the

1.) What is the total equivalent units of production for conversion to Department X?

2.) What is the percentage of completion (work done) for the work in process-Sept. 30 in terms of conversion to Department X?

3.) What is the total current cost of materials added in September to Department X?

4.) What is the total current cost of conversion added in September to Department X?

5.) How much is the total unit cost for September to Department X?

6.) How much is the total cost of the work in process on September 30 to Department X?

7.) How much is the amount of materials charged to work in process , Septermber 1 to Department Y?

8.) How much is the amount of conversion cost charged to work in process, September 1 to Department Y?

9.) How much is the value of finished goods already transferred to "Bodega" during September to Department Y?

10.) How much is the total cost of the work in process on September 30 to Department Y?

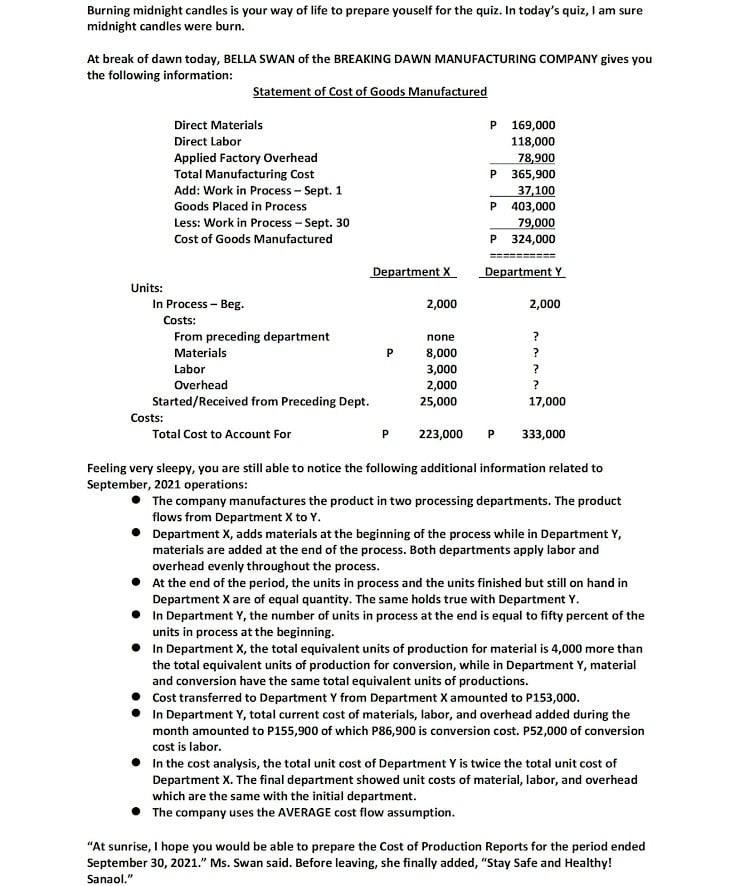

Burning midnight candles is your way of life to prepare youself for the quiz. In today's quiz, I am sure midnight candles were burn. At break of dawn today, BELLA SWAN of the BREAKING DAWN MANUFACTURING COMPANY gives you the following information: Statement of Cost of Goods Manufactured Direct Materials Direct Labor Applied Factory Overhead Total Manufacturing Cost Add: Work in Process - Sept. 1 Goods Placed in Process Less: Work in Process - Sept. 30 Cost of Goods Manufactured Units: In Process - Beg. Department X 2,000 P 169,000 118,000 78,900 P 365,900 37,100 P 403,000 79,000 P 324,000 Department Y 2,000 Costs: From preceding department none Materials P 8,000 ? Labor 3,000 ? Overhead 2,000 ? Started/Received from Preceding Dept. 25,000 17,000 Costs: Total Cost to Account For P 223,000 P 333,000 Feeling very sleepy, you are still able to notice the following additional information related to September, 2021 operations: The company manufactures the product in two processing departments. The product flows from Department X to Y. Department X, adds materials at the beginning of the process while in Department Y, materials are added at the end of the process. Both departments apply labor and overhead evenly throughout the process. At the end of the period, the units in process and the units finished but still on hand in Department X are of equal quantity. The same holds true with Department Y. In Department Y, the number of units in process at the end is equal to fifty percent of the units in process at the beginning. In Department X, the total equivalent units of production for material is 4,000 more than the total equivalent units of production for conversion, while in Department Y, material and conversion have the same total equivalent units of productions. Cost transferred to Department Y from Department X amounted to P153,000. In Department Y, total current cost of materials, labor, and overhead added during the month amounted to P155,900 of which P86,900 is conversion cost. P52,000 of conversion cost is labor. In the cost analysis, the total unit cost of Department Y is twice the total unit cost of Department X. The final department showed unit costs of material, labor, and overhead which are the same with the initial department. The company uses the AVERAGE cost flow assumption. "At sunrise, I hope you would be able to prepare the Cost of Production Reports for the period ended September 30, 2021." Ms. Swan said. Before leaving, she finally added, "Stay Safe and Healthy! Sanaol."

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray Garrison, Eric Noreen, Peter Brewer

16th edition

1259307417, 978-1260153132, 1260153134, 978-1259307416