Answered step by step

Verified Expert Solution

Question

1 Approved Answer

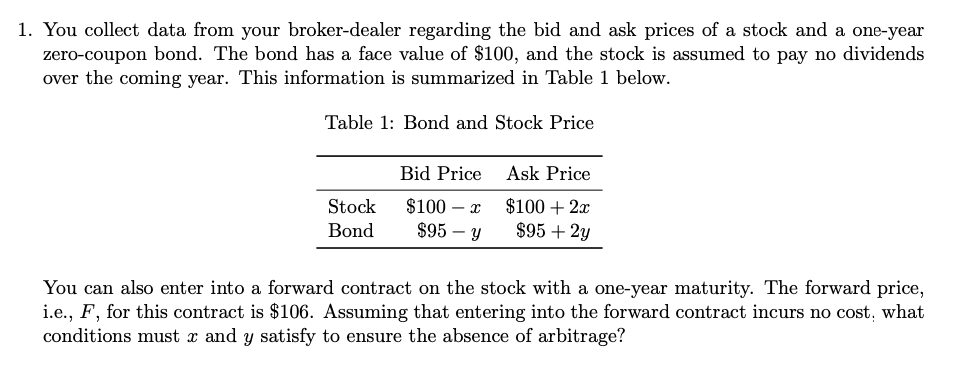

1 . You collect data from your broker - dealer regarding the bid and ask prices of a stock and a one - year zero

You collect data from your brokerdealer regarding the bid and ask prices of a stock and a oneyear zerocoupon bond. The bond has a face value of $ and the stock is assumed to pay no dividends over the coming year. This information is summarized in Table below.

Table : Bond and Stock Price

You can also enter into a forward contract on the stock with a oneyear maturity. The forward price, ie F for this contract is $ Assuming that entering into the forward contract incurs no cost what conditions must x and y satisfy to ensure the absence of arbitrage?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Finance

Authors: Scott Besley, Eugene F. Brigham

6th edition

9781305178045, 1285429648, 1305178041, 978-1285429649