Answered step by step

Verified Expert Solution

Question

1 Approved Answer

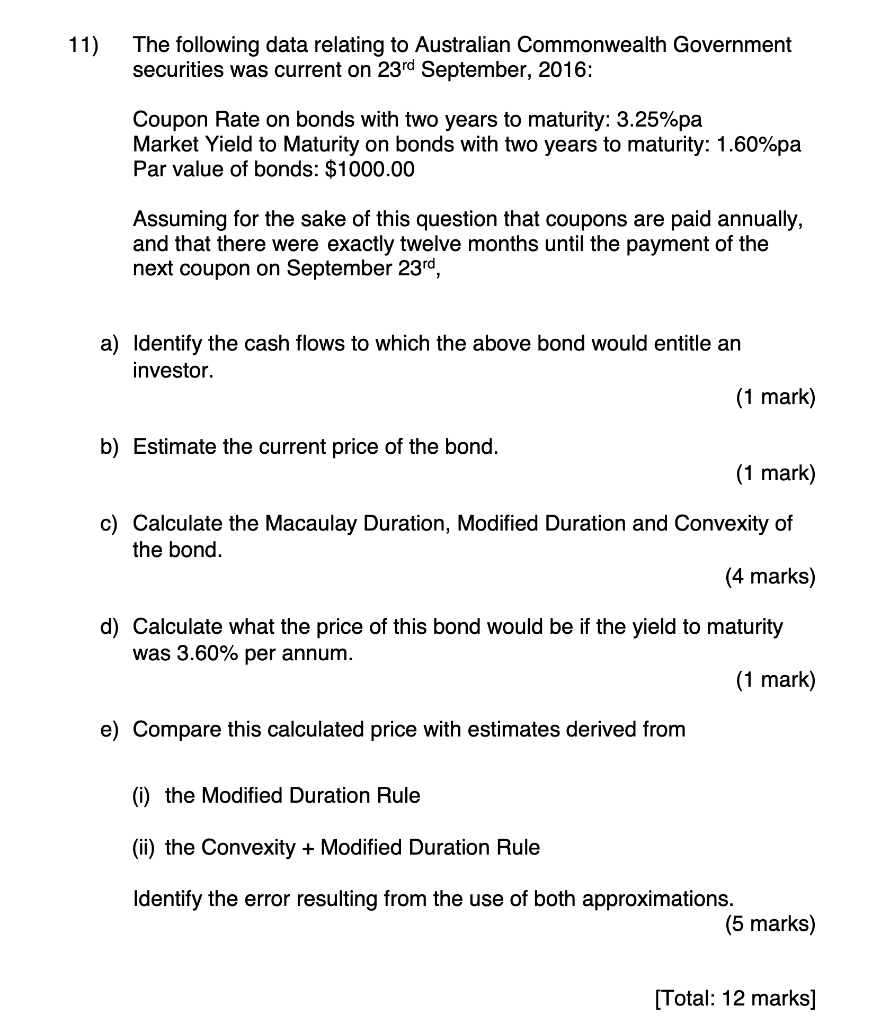

11) The following data relating to Australian Commonwealth Government securities was current on 23rd September, 2016: Coupon Rate on bonds with two years to maturity:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Achieving Financial Stability In America

Authors: Misook Yu CFP

1st Edition

1732024510, 978-1732024519