11-4 What do you feel are the best justifications for Alibaba to issue the IPO in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

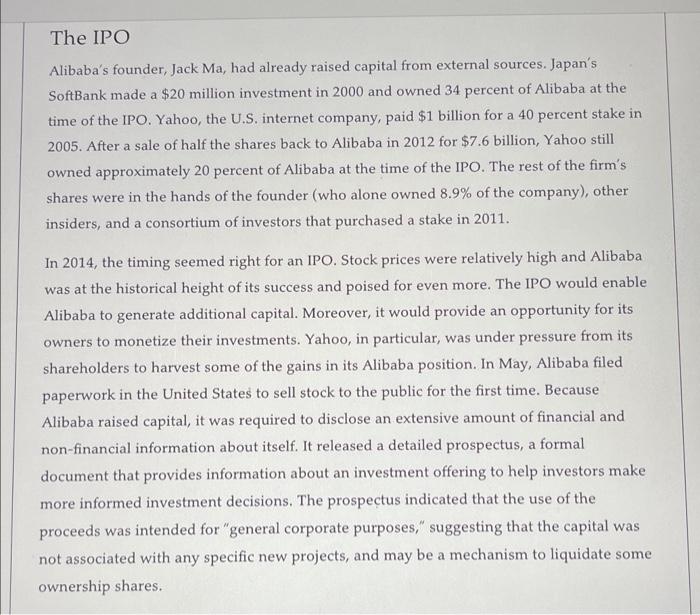

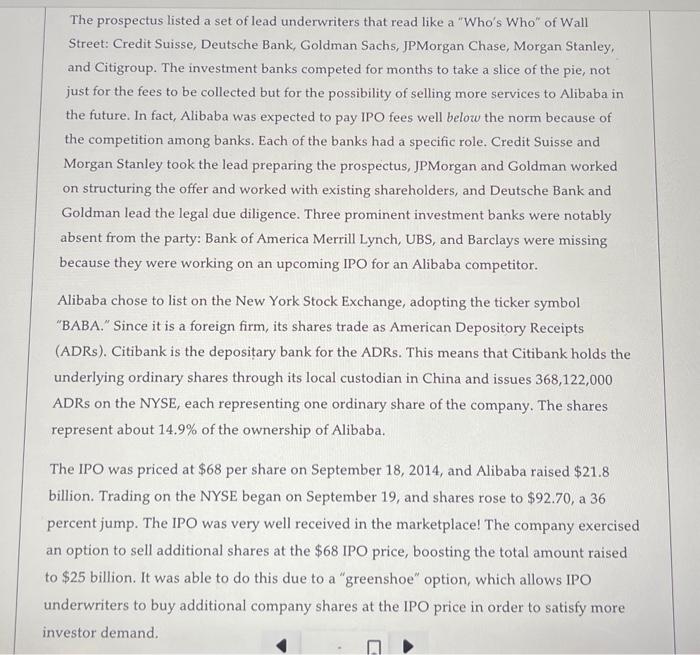

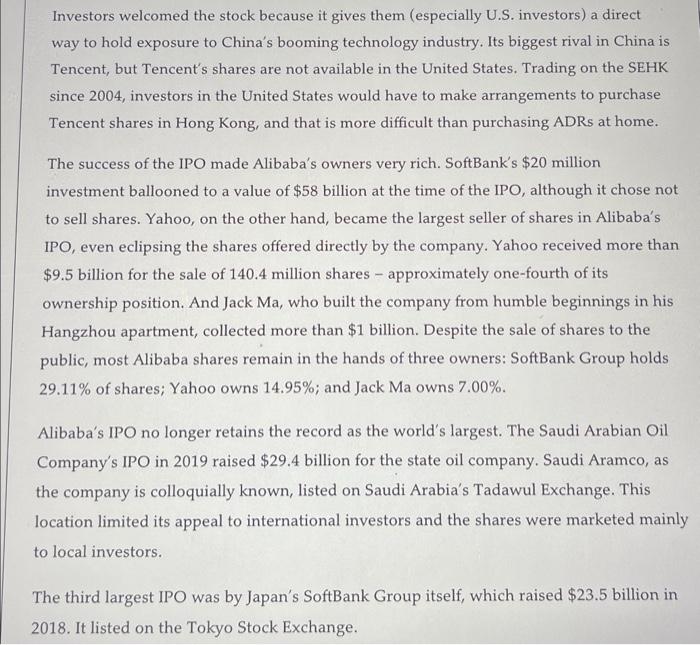

11-4 What do you feel are the best justifications for Alibaba to issue the IPO in New York? Are there any downsides to their decision to list in New York? The IPO Alibaba's founder, Jack Ma, had already raised capital from external sources. Japan's SoftBank made a $20 million investment in 2000 and owned 34 percent of Alibaba at the time of the IPO. Yahoo, the U.S. internet company, paid $1 billion for a 40 percent stake in 2005. After a sale of half the shares back to Alibaba in 2012 for $7.6 billion, Yahoo still owned approximately 20 percent of Alibaba at the time of the IPO. The rest of the firm's shares were in the hands of the founder (who alone owned 8.9% of the company), other insiders, and a consortium of investors that purchased a stake in 2011. In 2014, the timing seemed right for an IPO. Stock prices were relatively high and Alibaba was at the historical height of its success and poised for even more. The IPO would enable Alibaba to generate additional capital. Moreover, it would provide an opportunity for its owners to monetize their investments. Yahoo, in particular, was under pressure from its shareholders to harvest some of the gains in its Alibaba position. In May, Alibaba filed paperwork in the United States to sell stock to the public for the first time. Because Alibaba raised capital, it was required to disclose an extensive amount of financial and non-financial information about itself. It released a detailed prospectus, a formal document that provides information about an investment offering to help investors make more informed investment decisions. The prospectus indicated that the use of the proceeds was intended for "general corporate purposes," suggesting that the capital was not associated with any specific new projects, and may be a mechanism to liquidate some ownership shares. The prospectus listed a set of lead underwriters that read like a "Who's Who" of Wall Street: Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Citigroup. The investment banks competed for months to take a slice of the pie, not just for the fees to be collected but for the possibility of selling more services to Alibaba in the future. In fact, Alibaba was expected to pay IPO fees well below the norm because of the competition among banks. Each of the banks had a specific role. Credit Suisse and Morgan Stanley took the lead preparing the prospectus, JPMorgan and Goldman worked on structuring the offer and worked with existing shareholders, and Deutsche Bank and Goldman lead the legal due diligence. Three prominent investment banks were notably absent from the party: Bank of America Merrill Lynch, UBS, and Barclays were missing because they were working on an upcoming IPO for an Alibaba competitor. Alibaba chose to list on the New York Stock Exchange, adopting the ticker symbol "BABA." Since it is a foreign firm, its shares trade as American Depository Receipts (ADRs). Citibank is the depositary bank for the ADRs. This means that Citibank holds the underlying ordinary shares through its local custodian in China and issues 368,122,000 ADRs on the NYSE, each representing one ordinary share of the company. The shares represent about 14.9% of the ownership of Alibaba. The IPO was priced at $68 per share on September 18, 2014, and Alibaba raised $21.8 billion. Trading on the NYSE began on September 19, and shares rose to $92.70, a 36 percent jump. The IPO was very well received in the marketplace! The company exercised an option to sell additional shares at the $68 IPO price, boosting the total amount raised to $25 billion. It was able to do this due to a "greenshoe" option, which allows IPO underwriters to buy additional company shares at the IPO price in order to satisfy more investor demand. Investors welcomed the stock because it gives them (especially U.S. investors) a direct way to hold exposure to China's booming technology industry. Its biggest rival in China is Tencent, but Tencent's shares are not available in the United States. Trading on the SEHK since 2004, investors in the United States would have to make arrangements to purchase Tencent shares in Hong Kong, and that is more difficult than purchasing ADRs at home. The success of the IPO made Alibaba's owners very rich. SoftBank's $20 million investment ballooned to a value of $58 billion at the time of the IPO, although it chose not to sell shares. Yahoo, on the other hand, became the largest seller of shares in Alibaba's IPO, even eclipsing the shares offered directly by the company. Yahoo received more than $9.5 billion for the sale of 140.4 million shares approximately one-fourth of its ownership position. And Jack Ma, who built the company from humble beginnings in his Hangzhou apartment, collected more than $1 billion. Despite the sale of shares to the public, most Alibaba shares remain in the hands of three owners: SoftBank Group holds 29.11% of shares; Yahoo owns 14.95%; and Jack Ma owns 7.00%. Alibaba's IPO no longer retains the record as the world's largest. The Saudi Arabian Oil Company's IPO in 2019 raised $29.4 billion for the state oil company. Saudi Aramco, as the company is colloquially known, listed on Saudi Arabia's Tadawul Exchange. This location limited its appeal to international investors and the shares were marketed mainly to local investors. The third largest IPO was by Japan's SoftBank Group itself, which raised $23.5 billion in 2018. It listed on the Tokyo Stock Exchange. 11-4 What do you feel are the best justifications for Alibaba to issue the IPO in New York? Are there any downsides to their decision to list in New York? The IPO Alibaba's founder, Jack Ma, had already raised capital from external sources. Japan's SoftBank made a $20 million investment in 2000 and owned 34 percent of Alibaba at the time of the IPO. Yahoo, the U.S. internet company, paid $1 billion for a 40 percent stake in 2005. After a sale of half the shares back to Alibaba in 2012 for $7.6 billion, Yahoo still owned approximately 20 percent of Alibaba at the time of the IPO. The rest of the firm's shares were in the hands of the founder (who alone owned 8.9% of the company), other insiders, and a consortium of investors that purchased a stake in 2011. In 2014, the timing seemed right for an IPO. Stock prices were relatively high and Alibaba was at the historical height of its success and poised for even more. The IPO would enable Alibaba to generate additional capital. Moreover, it would provide an opportunity for its owners to monetize their investments. Yahoo, in particular, was under pressure from its shareholders to harvest some of the gains in its Alibaba position. In May, Alibaba filed paperwork in the United States to sell stock to the public for the first time. Because Alibaba raised capital, it was required to disclose an extensive amount of financial and non-financial information about itself. It released a detailed prospectus, a formal document that provides information about an investment offering to help investors make more informed investment decisions. The prospectus indicated that the use of the proceeds was intended for "general corporate purposes," suggesting that the capital was not associated with any specific new projects, and may be a mechanism to liquidate some ownership shares. The prospectus listed a set of lead underwriters that read like a "Who's Who" of Wall Street: Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Citigroup. The investment banks competed for months to take a slice of the pie, not just for the fees to be collected but for the possibility of selling more services to Alibaba in the future. In fact, Alibaba was expected to pay IPO fees well below the norm because of the competition among banks. Each of the banks had a specific role. Credit Suisse and Morgan Stanley took the lead preparing the prospectus, JPMorgan and Goldman worked on structuring the offer and worked with existing shareholders, and Deutsche Bank and Goldman lead the legal due diligence. Three prominent investment banks were notably absent from the party: Bank of America Merrill Lynch, UBS, and Barclays were missing because they were working on an upcoming IPO for an Alibaba competitor. Alibaba chose to list on the New York Stock Exchange, adopting the ticker symbol "BABA." Since it is a foreign firm, its shares trade as American Depository Receipts (ADRs). Citibank is the depositary bank for the ADRs. This means that Citibank holds the underlying ordinary shares through its local custodian in China and issues 368,122,000 ADRs on the NYSE, each representing one ordinary share of the company. The shares represent about 14.9% of the ownership of Alibaba. The IPO was priced at $68 per share on September 18, 2014, and Alibaba raised $21.8 billion. Trading on the NYSE began on September 19, and shares rose to $92.70, a 36 percent jump. The IPO was very well received in the marketplace! The company exercised an option to sell additional shares at the $68 IPO price, boosting the total amount raised to $25 billion. It was able to do this due to a "greenshoe" option, which allows IPO underwriters to buy additional company shares at the IPO price in order to satisfy more investor demand. Investors welcomed the stock because it gives them (especially U.S. investors) a direct way to hold exposure to China's booming technology industry. Its biggest rival in China is Tencent, but Tencent's shares are not available in the United States. Trading on the SEHK since 2004, investors in the United States would have to make arrangements to purchase Tencent shares in Hong Kong, and that is more difficult than purchasing ADRs at home. The success of the IPO made Alibaba's owners very rich. SoftBank's $20 million investment ballooned to a value of $58 billion at the time of the IPO, although it chose not to sell shares. Yahoo, on the other hand, became the largest seller of shares in Alibaba's IPO, even eclipsing the shares offered directly by the company. Yahoo received more than $9.5 billion for the sale of 140.4 million shares approximately one-fourth of its ownership position. And Jack Ma, who built the company from humble beginnings in his Hangzhou apartment, collected more than $1 billion. Despite the sale of shares to the public, most Alibaba shares remain in the hands of three owners: SoftBank Group holds 29.11% of shares; Yahoo owns 14.95%; and Jack Ma owns 7.00%. Alibaba's IPO no longer retains the record as the world's largest. The Saudi Arabian Oil Company's IPO in 2019 raised $29.4 billion for the state oil company. Saudi Aramco, as the company is colloquially known, listed on Saudi Arabia's Tadawul Exchange. This location limited its appeal to international investors and the shares were marketed mainly to local investors. The third largest IPO was by Japan's SoftBank Group itself, which raised $23.5 billion in 2018. It listed on the Tokyo Stock Exchange. 11-4 What do you feel are the best justifications for Alibaba to issue the IPO in New York? Are there any downsides to their decision to list in New York? The IPO Alibaba's founder, Jack Ma, had already raised capital from external sources. Japan's SoftBank made a $20 million investment in 2000 and owned 34 percent of Alibaba at the time of the IPO. Yahoo, the U.S. internet company, paid $1 billion for a 40 percent stake in 2005. After a sale of half the shares back to Alibaba in 2012 for $7.6 billion, Yahoo still owned approximately 20 percent of Alibaba at the time of the IPO. The rest of the firm's shares were in the hands of the founder (who alone owned 8.9% of the company), other insiders, and a consortium of investors that purchased a stake in 2011. In 2014, the timing seemed right for an IPO. Stock prices were relatively high and Alibaba was at the historical height of its success and poised for even more. The IPO would enable Alibaba to generate additional capital. Moreover, it would provide an opportunity for its owners to monetize their investments. Yahoo, in particular, was under pressure from its shareholders to harvest some of the gains in its Alibaba position. In May, Alibaba filed paperwork in the United States to sell stock to the public for the first time. Because Alibaba raised capital, it was required to disclose an extensive amount of financial and non-financial information about itself. It released a detailed prospectus, a formal document that provides information about an investment offering to help investors make more informed investment decisions. The prospectus indicated that the use of the proceeds was intended for "general corporate purposes," suggesting that the capital was not associated with any specific new projects, and may be a mechanism to liquidate some ownership shares. The prospectus listed a set of lead underwriters that read like a "Who's Who" of Wall Street: Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Citigroup. The investment banks competed for months to take a slice of the pie, not just for the fees to be collected but for the possibility of selling more services to Alibaba in the future. In fact, Alibaba was expected to pay IPO fees well below the norm because of the competition among banks. Each of the banks had a specific role. Credit Suisse and Morgan Stanley took the lead preparing the prospectus, JPMorgan and Goldman worked on structuring the offer and worked with existing shareholders, and Deutsche Bank and Goldman lead the legal due diligence. Three prominent investment banks were notably absent from the party: Bank of America Merrill Lynch, UBS, and Barclays were missing because they were working on an upcoming IPO for an Alibaba competitor. Alibaba chose to list on the New York Stock Exchange, adopting the ticker symbol "BABA." Since it is a foreign firm, its shares trade as American Depository Receipts (ADRs). Citibank is the depositary bank for the ADRs. This means that Citibank holds the underlying ordinary shares through its local custodian in China and issues 368,122,000 ADRs on the NYSE, each representing one ordinary share of the company. The shares represent about 14.9% of the ownership of Alibaba. The IPO was priced at $68 per share on September 18, 2014, and Alibaba raised $21.8 billion. Trading on the NYSE began on September 19, and shares rose to $92.70, a 36 percent jump. The IPO was very well received in the marketplace! The company exercised an option to sell additional shares at the $68 IPO price, boosting the total amount raised to $25 billion. It was able to do this due to a "greenshoe" option, which allows IPO underwriters to buy additional company shares at the IPO price in order to satisfy more investor demand. Investors welcomed the stock because it gives them (especially U.S. investors) a direct way to hold exposure to China's booming technology industry. Its biggest rival in China is Tencent, but Tencent's shares are not available in the United States. Trading on the SEHK since 2004, investors in the United States would have to make arrangements to purchase Tencent shares in Hong Kong, and that is more difficult than purchasing ADRs at home. The success of the IPO made Alibaba's owners very rich. SoftBank's $20 million investment ballooned to a value of $58 billion at the time of the IPO, although it chose not to sell shares. Yahoo, on the other hand, became the largest seller of shares in Alibaba's IPO, even eclipsing the shares offered directly by the company. Yahoo received more than $9.5 billion for the sale of 140.4 million shares approximately one-fourth of its ownership position. And Jack Ma, who built the company from humble beginnings in his Hangzhou apartment, collected more than $1 billion. Despite the sale of shares to the public, most Alibaba shares remain in the hands of three owners: SoftBank Group holds 29.11% of shares; Yahoo owns 14.95%; and Jack Ma owns 7.00%. Alibaba's IPO no longer retains the record as the world's largest. The Saudi Arabian Oil Company's IPO in 2019 raised $29.4 billion for the state oil company. Saudi Aramco, as the company is colloquially known, listed on Saudi Arabia's Tadawul Exchange. This location limited its appeal to international investors and the shares were marketed mainly to local investors. The third largest IPO was by Japan's SoftBank Group itself, which raised $23.5 billion in 2018. It listed on the Tokyo Stock Exchange. 11-4 What do you feel are the best justifications for Alibaba to issue the IPO in New York? Are there any downsides to their decision to list in New York? The IPO Alibaba's founder, Jack Ma, had already raised capital from external sources. Japan's SoftBank made a $20 million investment in 2000 and owned 34 percent of Alibaba at the time of the IPO. Yahoo, the U.S. internet company, paid $1 billion for a 40 percent stake in 2005. After a sale of half the shares back to Alibaba in 2012 for $7.6 billion, Yahoo still owned approximately 20 percent of Alibaba at the time of the IPO. The rest of the firm's shares were in the hands of the founder (who alone owned 8.9% of the company), other insiders, and a consortium of investors that purchased a stake in 2011. In 2014, the timing seemed right for an IPO. Stock prices were relatively high and Alibaba was at the historical height of its success and poised for even more. The IPO would enable Alibaba to generate additional capital. Moreover, it would provide an opportunity for its owners to monetize their investments. Yahoo, in particular, was under pressure from its shareholders to harvest some of the gains in its Alibaba position. In May, Alibaba filed paperwork in the United States to sell stock to the public for the first time. Because Alibaba raised capital, it was required to disclose an extensive amount of financial and non-financial information about itself. It released a detailed prospectus, a formal document that provides information about an investment offering to help investors make more informed investment decisions. The prospectus indicated that the use of the proceeds was intended for "general corporate purposes," suggesting that the capital was not associated with any specific new projects, and may be a mechanism to liquidate some ownership shares. The prospectus listed a set of lead underwriters that read like a "Who's Who" of Wall Street: Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Citigroup. The investment banks competed for months to take a slice of the pie, not just for the fees to be collected but for the possibility of selling more services to Alibaba in the future. In fact, Alibaba was expected to pay IPO fees well below the norm because of the competition among banks. Each of the banks had a specific role. Credit Suisse and Morgan Stanley took the lead preparing the prospectus, JPMorgan and Goldman worked on structuring the offer and worked with existing shareholders, and Deutsche Bank and Goldman lead the legal due diligence. Three prominent investment banks were notably absent from the party: Bank of America Merrill Lynch, UBS, and Barclays were missing because they were working on an upcoming IPO for an Alibaba competitor. Alibaba chose to list on the New York Stock Exchange, adopting the ticker symbol "BABA." Since it is a foreign firm, its shares trade as American Depository Receipts (ADRs). Citibank is the depositary bank for the ADRs. This means that Citibank holds the underlying ordinary shares through its local custodian in China and issues 368,122,000 ADRs on the NYSE, each representing one ordinary share of the company. The shares represent about 14.9% of the ownership of Alibaba. The IPO was priced at $68 per share on September 18, 2014, and Alibaba raised $21.8 billion. Trading on the NYSE began on September 19, and shares rose to $92.70, a 36 percent jump. The IPO was very well received in the marketplace! The company exercised an option to sell additional shares at the $68 IPO price, boosting the total amount raised to $25 billion. It was able to do this due to a "greenshoe" option, which allows IPO underwriters to buy additional company shares at the IPO price in order to satisfy more investor demand. Investors welcomed the stock because it gives them (especially U.S. investors) a direct way to hold exposure to China's booming technology industry. Its biggest rival in China is Tencent, but Tencent's shares are not available in the United States. Trading on the SEHK since 2004, investors in the United States would have to make arrangements to purchase Tencent shares in Hong Kong, and that is more difficult than purchasing ADRs at home. The success of the IPO made Alibaba's owners very rich. SoftBank's $20 million investment ballooned to a value of $58 billion at the time of the IPO, although it chose not to sell shares. Yahoo, on the other hand, became the largest seller of shares in Alibaba's IPO, even eclipsing the shares offered directly by the company. Yahoo received more than $9.5 billion for the sale of 140.4 million shares approximately one-fourth of its ownership position. And Jack Ma, who built the company from humble beginnings in his Hangzhou apartment, collected more than $1 billion. Despite the sale of shares to the public, most Alibaba shares remain in the hands of three owners: SoftBank Group holds 29.11% of shares; Yahoo owns 14.95%; and Jack Ma owns 7.00%. Alibaba's IPO no longer retains the record as the world's largest. The Saudi Arabian Oil Company's IPO in 2019 raised $29.4 billion for the state oil company. Saudi Aramco, as the company is colloquially known, listed on Saudi Arabia's Tadawul Exchange. This location limited its appeal to international investors and the shares were marketed mainly to local investors. The third largest IPO was by Japan's SoftBank Group itself, which raised $23.5 billion in 2018. It listed on the Tokyo Stock Exchange.

Expert Answer:

Answer rating: 100% (QA)

Based on the text provided in the images there are several justifications for Alibaba to issue its Initial Public Offering IPO in New York as well as ... View the full answer

Related Book For

International Business

ISBN: 978-0133457230

15th edition

Authors: John Daniels, Lee Radebaugh, Daniel Sullivan

Posted Date:

Students also viewed these general management questions

-

Hopson Company incurred $900,000 of research and development costs in its laboratory to develop a new product. It spent $120,000 in legal fees for a patent granted on January 2, 2022. On July 31,...

-

It cost the contractor $13,750 to manufacture their first unit. The company expects to experience a 93% unit learning curve. Estimate the cost of the 14th unit.

-

What do you feel are the best justifications for Prada to issue the IPO in Hong Kong? Are there any downsides to their decision to list in Hong Kong?

-

A website that reviews recent movies lists 6 five-star films (the highest rating), 17 four-star films, 14 three-star films, 9 two-star films, and 4 one-star films. Make a frequency table for the data...

-

Write equations for the (a) saponification, (b) hydrogenation, and (c) hydrogenolysis of glyceryl trilaurate.

-

Kozy Enterprises is considering manufacturing a new product. It projects the cost of direct materials and rent for a range of output as shown below: Instructions (a) Diagram the behaviour of each...

-

You have been talking to someone who had read a few chapters of an accounting text some years ago. During your conversation the person made the following statements: (a) The income statement shows...

-

Call Systems Company, a telephone service and supply company, has just completed its fourth year of operations. The direct write-off method of recording bad debt expense has been used during the...

-

Fstimating Share Value Using the DCF Model e forecasted sales, NOPAT, and NOA for Colgate - Palmolive Company for 2 0 1 9 through 2 0 2 2 . Note: Complete the entire question in Excel and format each...

-

Exercise 6.1 Configuring Memory on Paper Objective: a computer is not performing as well as it used to. Windows 10 tool would the technician get the user to open to quickly tell how much RAM is...

-

Consider the linear programming problem: Maximize P : 60512 + 503; . m-i-ySSO 5m+10yg560 50$+20y S 1600 51220 3120 Use the simplex method to solve the problem. Use 5, t, and u as your slack variables...

-

Describe persistence design under NoSQL technologies.? What is NoSQL polyglot persistence?

-

The pace of economic and workplace change is faster than ever. How have people been affected by such changes in the past and how have they adapted? What lessons can we learn for success in the modern...

-

Revising organisational structures is often perceived as a way to improve efficiency, promote teamwork, create synergy or reduce costs. However, the management of your organisation is not clear on...

-

A company is considering buying a product at $15 per unit, the in-house manufacturing of the same product is $17. The fixed cost per unit is $3 is included in the $17 in-house product manufacturing...

-

List four main differences between document Nosql database and key-value NoSql database ?

-

Feather Friends, Inc., distributes a high-quality wooden birdhouse that sells for $80 per unit. Variable expenses are $40.00 per unit, and fixed expenses total $180,000 per year. Its operating...

-

Read the case study Richter: Information Technology at Hungarys Largest Pharma and answer the following question: How does the organization ensure the accuracy of the data it stores?

-

Why do you think it is important for Sony to manufacture more products in the United States and Europe and to also buy more from suppliers in other countries in Asia?

-

What threats exist to the future performance of the cruise-line industry and specifically of Carnival Cruise Lines? If you were in charge of Carnival, how would you (a) Try to prevent these threats...

-

How much do you think Danone's decision to set up a social business was motivated by wanting to be socially responsible versus believing the move would help its performance? Does the answer to this...

-

Compute margin of safety (Learning Objective 5)} Use the information from the Bay Cruiseline Data Set. If Bay Cruiseline sells 7,000 dinner cruises, compute the margin of safety: a. In units (dinner...

-

Compute and use operating leverage factor (Learning Objective 5) Suppose Kay sells 800 posters. Use the original data ( \(\$ 35\) sales price, \(\$ 21\) variable cost, \(\$ 7,000\) fixed expenses) to...

-

Compute margin of safety (Learning Objective 5) Consider Kay's e-tail poster business. Suppose Kay expects to sell 800 posters. Use the original data ( \(\$ 35\) sales price, \(\$ 21\) variable cost,...

Study smarter with the SolutionInn App