Answered step by step

Verified Expert Solution

Question

1 Approved Answer

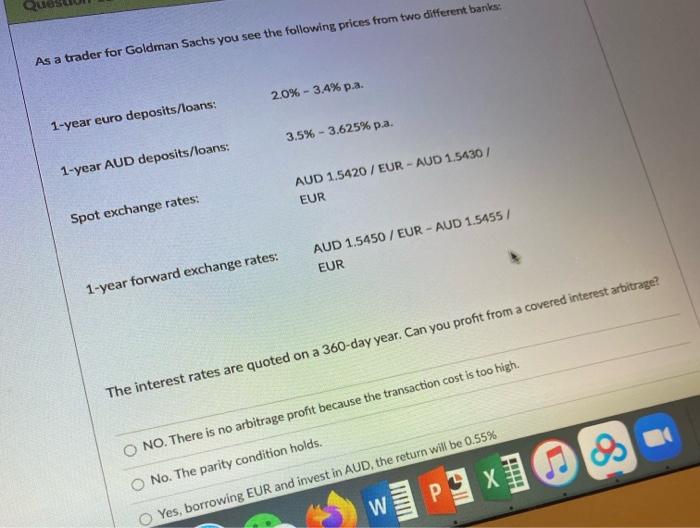

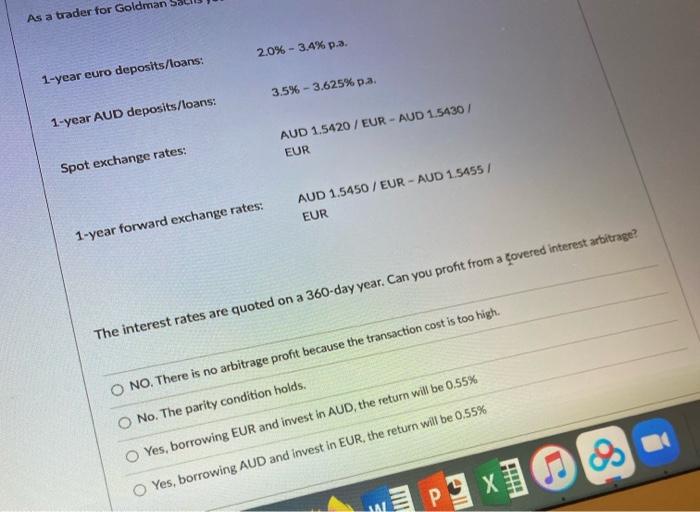

18 As a trader for Goldman Sachs you see the following prices from two different banks 2.0% - 3.4% p.a. 1-year euro deposits/loans: 3.5% -

18

As a trader for Goldman Sachs you see the following prices from two different banks 2.0% - 3.4% p.a. 1-year euro deposits/loans: 3.5% - 3.625% p.a. 1-year AUD deposits/loans: AUD 1.5420 / EUR - AUD 1.5430 / EUR Spot exchange rates: AUD 1.5450 / EUR - AUD 1.5455/ EUR 1-year forward exchange rates: The interest rates are quoted on a 360-day year. Can you profit from a covered interest arbitrage? O NO. There is no arbitrage profit because the transaction cost is too high. No. The parity condition holds. Yes, borrowing EUR and invest in AUD, the return will be 0.55% WI P9 x1 OS- As a trader for Goldman 2.0% - 3.4% p.a. 1-year euro deposits/loans: 35% - 3.625% pa 1-year AUD deposits/loans: AUD 1.5420 / EUR - AUD 1.5430 / EUR Spot exchange rates: AUD 1.5450 / EUR - AUD 1.5455/ EUR 1-year forward exchange rates: The interest rates are quoted on a 360-day year. Can you profit from a covered interest arbitrage? O NO. There is no arbitrage profit because the transaction cost is too high. No. The parity condition holds. Yes, borrowing EUR and invest in AUD, the return will be 0,55% Yes, borrowing AUD and invest in EUR, the return will be 0.55% x10 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stock Market Trading For Beginners

Authors: Irvin Tarr

1st Edition

1491885327, 978-1491885321