Answered step by step

Verified Expert Solution

Question

1 Approved Answer

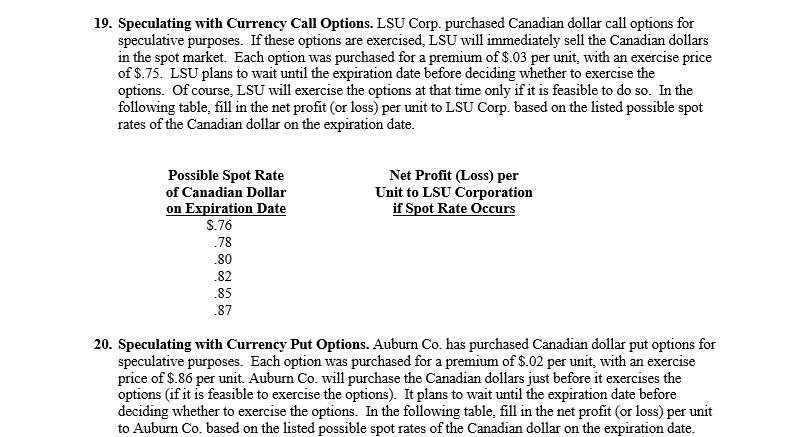

19. Speculating with Currency Call Options. LSU Corp. purchased Canadian dollar call options for speculative purposes. If these options are exercised, LSU will immediately

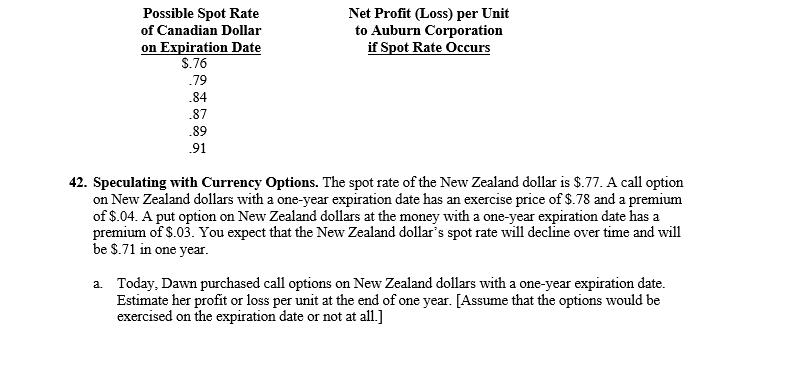

19. Speculating with Currency Call Options. LSU Corp. purchased Canadian dollar call options for speculative purposes. If these options are exercised, LSU will immediately sell the Canadian dollars in the spot market. Each option was purchased for a premium of $.03 per unit, with an exercise price of $.75. LSU plans to wait until the expiration date before deciding whether to exercise the options. Of course, LSU will exercise the options at that time only if it is feasible to do so. In the following table, fill in the net profit (or loss) per unit to LSU Corp. based on the listed possible spot rates of the Canadian dollar on the expiration date. Possible Spot Rate of Canadian Dollar on Expiration Date Net Profit (Loss) per Unit to LSU Corporation if Spot Rate Occurs $.76 .78 .80 .82 .85 .87 20. Speculating with Currency Put Options. Auburn Co. has purchased Canadian dollar put options for speculative purposes. Each option was purchased for a premium of $.02 per unit, with an exercise price of $.86 per unit. Auburn Co. will purchase the Canadian dollars just before it exercises the options (if it is feasible to exercise the options). It plans to wait until the expiration date before deciding whether to exercise the options. In the following table, fill in the net profit (or loss) per unit to Auburn Co. based on the listed possible spot rates of the Canadian dollar on the expiration date. Possible Spot Rate of Canadian Dollar on Expiration Date $.76 Net Profit (Loss) per Unit to Auburn Corporation if Spot Rate Occurs .79 .84 .87 .89 .91 42. Speculating with Currency Options. The spot rate of the New Zealand dollar is $.77. A call option on New Zealand dollars with a one-year expiration date has an exercise price of $.78 and a premium of $.04. A put option on New Zealand dollars at the money with a one-year expiration date has a premium of $.03. You expect that the New Zealand dollar's spot rate will decline over time and will be $.71 in one year. a. Today, Dawn purchased call options on New Zealand dollars with a one-year expiration date. Estimate her profit or loss per unit at the end of one year. [Assume that the options would be exercised on the expiration date or not at all.]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International financial management

Authors: Jeff Madura

9th Edition

978-0324593495, 324568207, 324568193, 032459349X, 9780324568202, 9780324568196, 978-0324593471