Answered step by step

Verified Expert Solution

Question

1 Approved Answer

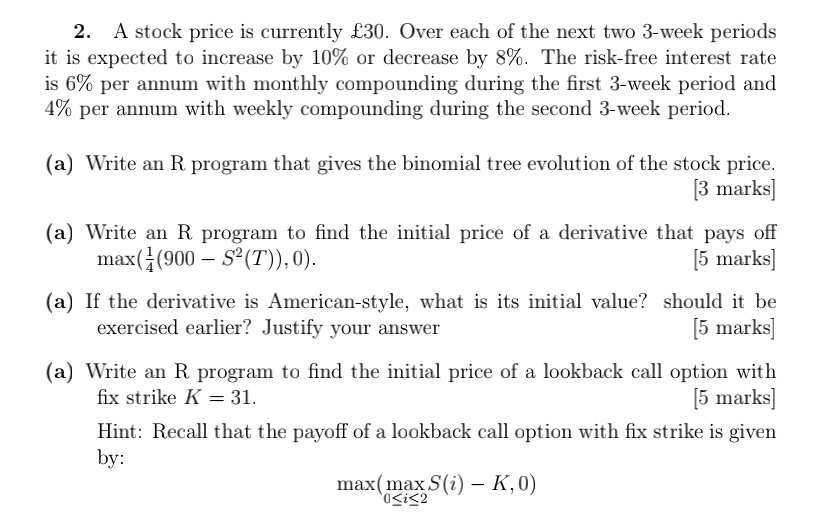

2. A stock price is currently 30. Over each of the next two 3-week periods it is expected to increase by 10% or decrease

2. A stock price is currently 30. Over each of the next two 3-week periods it is expected to increase by 10% or decrease by 8%. The risk-free interest rate is 6% per annum with monthly compounding during the first 3-week period and 4% per annum with weekly compounding during the second 3-week period. (a) Write an R program that gives the binomial tree evolution of the stock price. [3 marks] (a) Write an R program to find the initial price of a derivative that pays off max((900 S (T)), 0). [5 marks] (a) If the derivative is American-style, what is its initial value? should it be exercised earlier? Justify your answer [5 marks] (a) Write an R program to find the initial price of a lookback call option with fix strike K = 31. [5 marks] Hint: Recall that the payoff of a lookback call option with fix strike is given by: max(max S(i) - K, 0) 0

Step by Step Solution

★★★★★

3.51 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Certainly Below are R p...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Accounting

Authors: Fred Phillips, Robert Libby, Patricia Libby

5th edition

78025915, 978-1259115400, 1259115402, 978-0078025914