Answered step by step

Verified Expert Solution

Question

1 Approved Answer

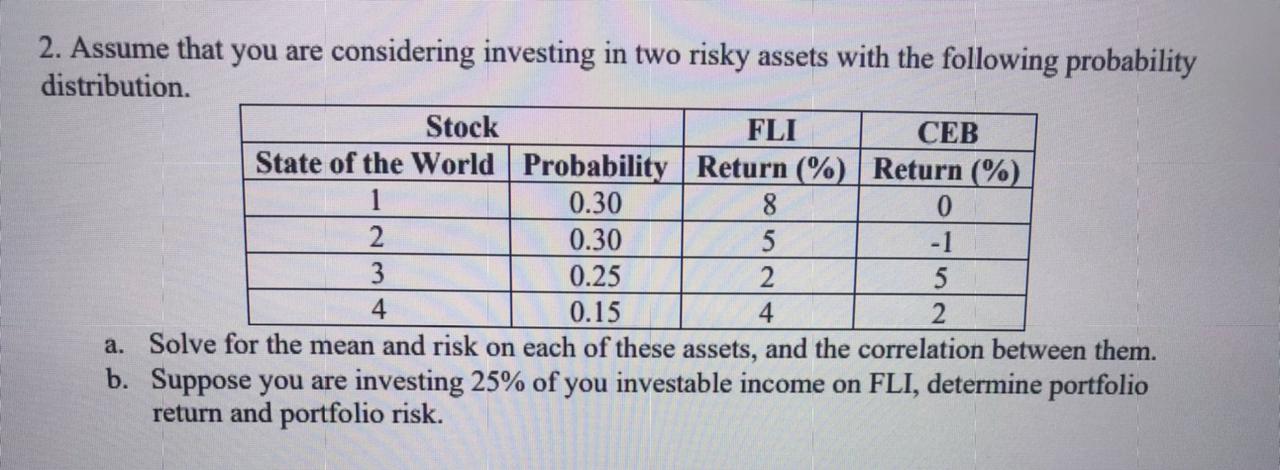

2. Assume that you are considering investing in two risky assets with the following probability distribution. Stock State of the World Probability 1 0.30

2. Assume that you are considering investing in two risky assets with the following probability distribution. Stock State of the World Probability 1 0.30 2 FLI CEB Return (%) Return (%) 8 0 5 -1 5 2 0.30 0.25 0.15 a. Solve for the mean and risk on each of these assets, and the correlation between them. b. Suppose you are investing 25% of you investable income on FLI, determine portfolio return and portfolio risk. 3 4 2 4

Step by Step Solution

★★★★★

3.43 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

a Stock 1 Mean return 038 032 0255 0154 5 Variance 03...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Algebra

Authors: Margaret L. Lial, John Hornsby, David I. Schneider, Callie Daniels

12th edition

134697022, 9780134313795 , 978-0134697024