Answered step by step

Verified Expert Solution

Question

1 Approved Answer

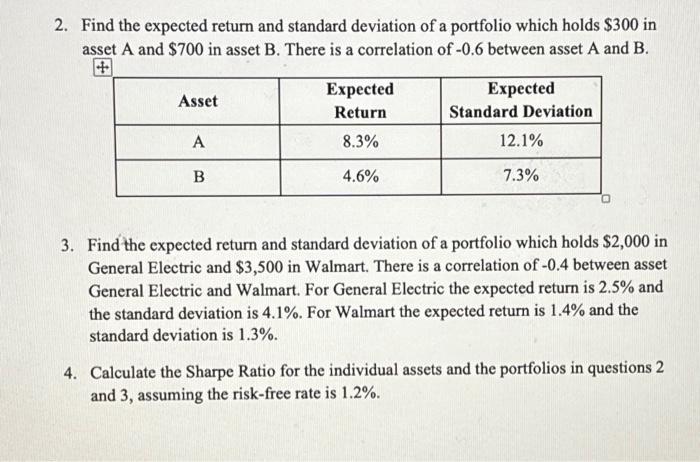

2. Find the expected return and standard deviation of a portfolio which holds $300 in asset A and $700 in asset B. There is

2. Find the expected return and standard deviation of a portfolio which holds $300 in asset A and $700 in asset B. There is a correlation of -0.6 between asset A and B. + Expected Asset Expected Return Standard Deviation A 8.3% 12.1% B 4.6% 7.3% 3. Find the expected return and standard deviation of a portfolio which holds $2,000 in General Electric and $3,500 in Walmart. There is a correlation of -0.4 between asset General Electric and Walmart. For General Electric the expected return is 2.5% and the standard deviation is 4.1%. For Walmart the expected return is 1.4% and the standard deviation is 1.3%. 4. Calculate the Sharpe Ratio for the individual assets and the portfolios in questions 2 and 3, assuming the risk-free rate is 1.2%.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

13th International Edition

1265533199, 978-1265533199