Answered step by step

Verified Expert Solution

Question

1 Approved Answer

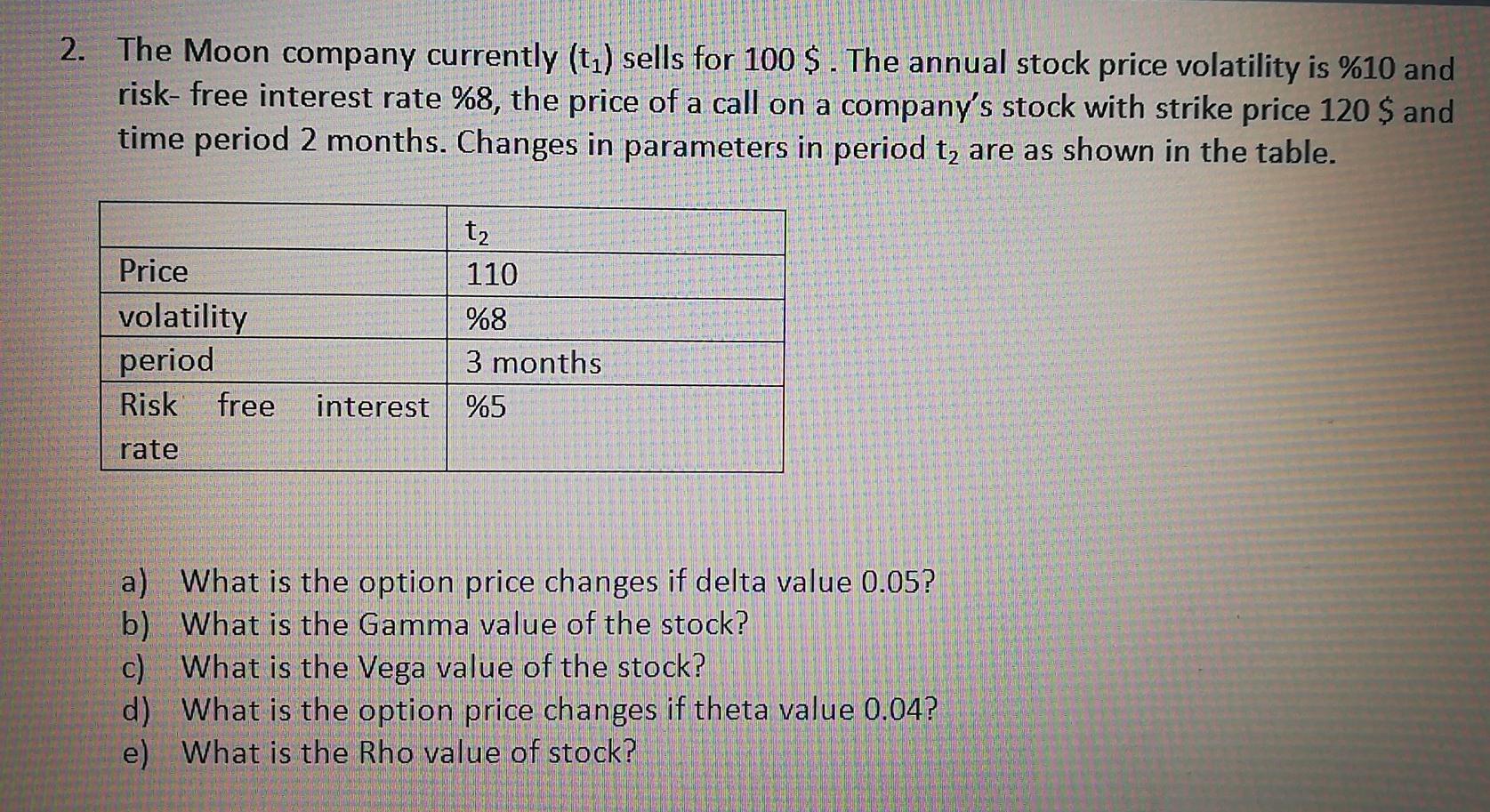

2. The Moon company currently (t1) sells for 100 $ . The annual stock price volatility is %10 and risk- free interest rate %8, the

2. The Moon company currently (t1) sells for 100 $ . The annual stock price volatility is %10 and risk- free interest rate %8, the price of a call on a company's stock with strike price 120 $ and time period 2 months. Changes in parameters in period ty are as shown in the table. Price volatility period Risk free t 110 %8 3 months %5 interest rate a) What is the option price changes if delta value 0.05? b) What is the Gamma value of the stock? c) What is the Vega value of the stock? d) What is the option price changes if theta value 0.04? e) What is the Rho value of stock

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Trade Finance

Authors: Indian Institute Of Banking & Finance

1st Edition

9386394723, 978-9386394729