Answered step by step

Verified Expert Solution

Question

1 Approved Answer

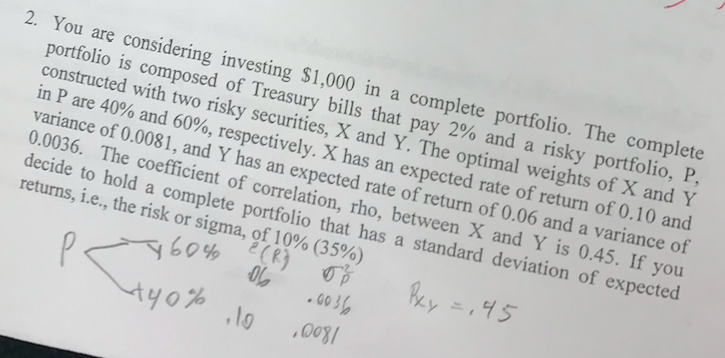

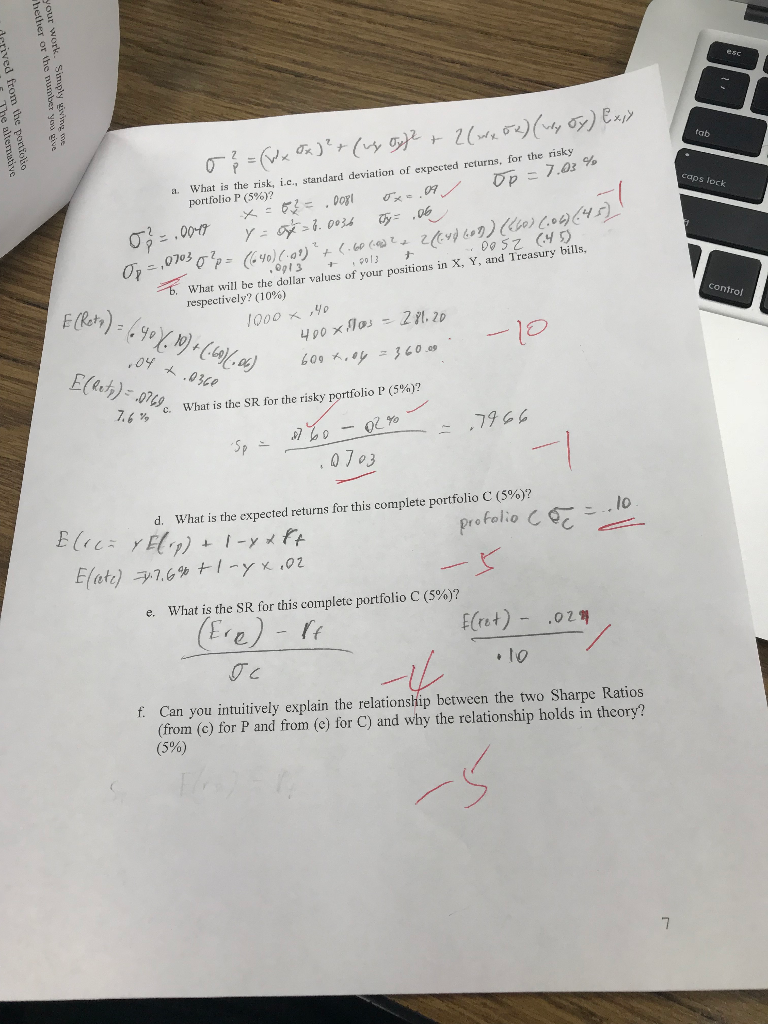

2. You are considering investing $1,000 in a complete portfolio. The complete portfolio is composed of Treasury bills that pay 2% and a risky portfolio,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: E. Thomas Garman, Raymond E. Forgue, Jonathan Fox

14th Edition

0357901495, 9780357901496