Answered step by step

Verified Expert Solution

Question

1 Approved Answer

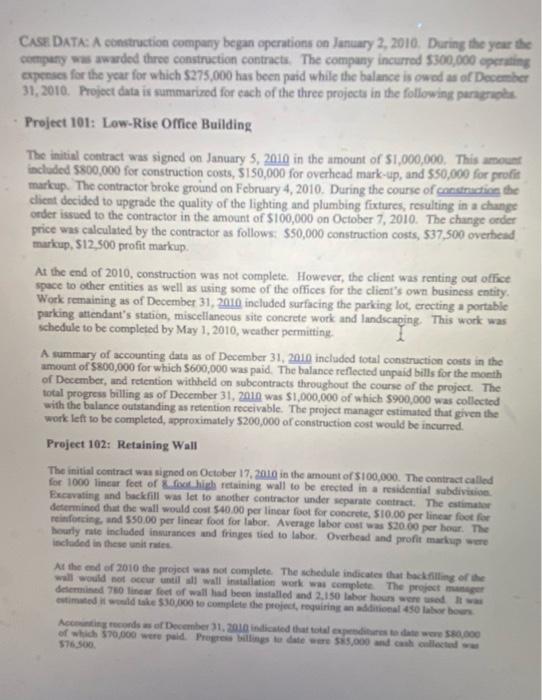

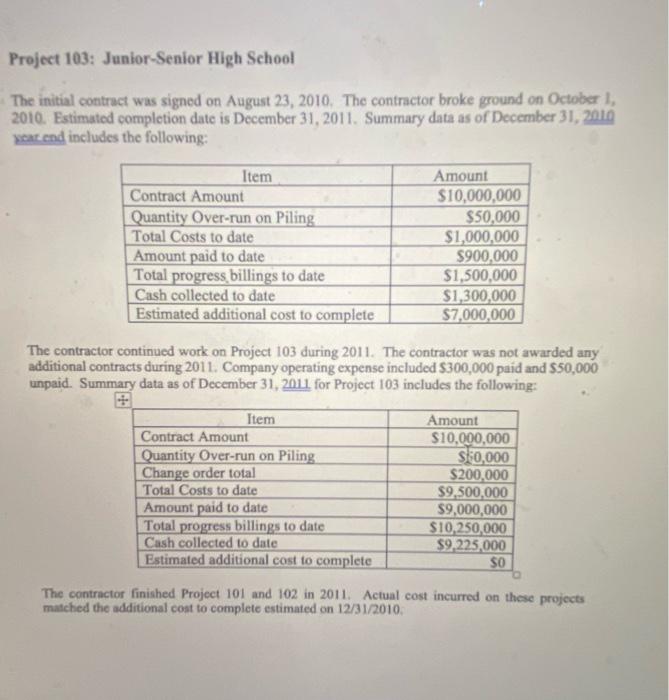

2-7 please CAE DATA: A construction company began operations on January 2, 2010. Daring the year the coenpary was awarded three construction contracts. The company

2-7 please

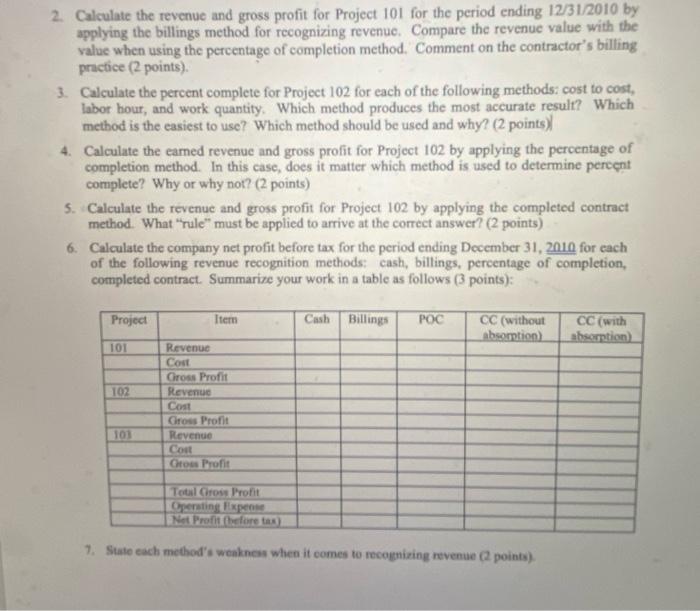

CAE DATA: A construction company began operations on January 2, 2010. Daring the year the coenpary was awarded three construction contracts. The company incurrod 5300,000 cperatieg experses for the year for which $275.000 has been paid while the balance is ow od as of December 31, 2010. Projoct data is summarized for each of the three projecta in the following paraerages. Project 101: Low-Rise Office Building The initial contract was signed on January 5,2010 in the amount of 51,000,000, This amocen included 5800,000 for construction costs, 5150,000 for overhead mark-up, and 550,000 for grufir markup. The contractor broke ground on February 4, 2010. During the course of constnuction the client decided to upgrade the quality of the lighting and plumbing fixtures, resulting in a changs order issued to the contractor in the amount of $100,000 on October 7, 2010. The change order price was calculated by the contractor as follows; 550,000 construction costs, 537,500 overbead markup, \$12,500 profit markup. At the end of 2010 , construction was not complete. However, the client was renting out office space to other entities as well as using some of the offices for the client's own business entity. Work remaining as of December 31,2010 included surfacing the parking lot, erecting a portable parking attendant's station, miscellaneous site concrete work and landscaping. This work was schedule to be completed by May 1,2010, weather permitting. A summary of accounting date as of December 31,2010 included total conseruction conts in the amount of 5800,000 for which $600,000 was paid. The balance reflected unpaid bills for the month of December, and retention withheld on subcontracts throughout the course of the project. The total progress billing as of December 31, 2010 was $1,000,000 of which $900,000 was collected with the balance outatanding as retention receivable. The project manager estimated that given the work left to be completed, approximately $200,000 of construction cost would be incurred. Project 102: Retaining Wall The initial centract was signed on October 17,2010 in the amount of $100,000. The cnntract called for 1000 linear foet of g foct. high retaining wall to be erected in a residential subdivition. Exeavating and backfill was let to anotber contractor under separate contract, The cotimatar deternined that the wall would cost 540.00per linear foot for concrote, 510.00 per linear foot for reinforring and 580.00 per linear foot for labor. Average labor cout was $2000 per howar. The hourly mate included insurances and fringes tied to labor. Overhead and profit markip were ischided in these unit rates. At the eed of 2010 the projoct was not complete. The whedule indicates that back filling of the wall would not occur timeil all wall inataliation work was complete The project maneger desermined 750 linear fert of wall had beos installed and 2.150 labor hours aere used A wat Project 103: Junior-Senior High School The initial contract was signed on August 23, 2010. The contractor broke ground on October 1, 2010. Estimated completion date is December 31, 2011. Summary data as of December 31, 2010 yeacend includes the following: The contractor continued work on Project 103 during 2011. The contractor was not awarded any additional contracts during 2011. Company operating expense included $300,000 paid and $50,000 unpaid. Summary data as of December 31, 2011 for Project 103 includes the following: The contractor finished Project 101 and 102 in 2011 . Actual cost incurred on these projects matched the additional cost to complete estimated on 12/31/2010. 2. Calculate the revenue and gross profit for Project 101 for the period ending 12/31/2010 by applying the billings method for recognizing revenue. Compare the revenue value with the value when using the percentage of completion method. Comment on the contractor's billing practice (2 points). 3. Calculate the percent complete for Project 102 for each of the following methods: cost to cost, labor hour, and work quantity. Which method produces the most accurate result? Which method is the easiest to use? Which method should be used and why? (2 points)) 4. Calculate the eamed revenue and gross profit for Project 102 by applying the percentage of completion method. In this case, does it matter which method is used to determine pereent complete? Why or why not? ( 2 points) 5. Calculate the revenue and gross profit for Project 102 by applying the completed contract method. What "rule" must be applied to arrive at the correct answer? (2 points) 6. Calculate the company net profit before tax for the period ending December 31,2010 for each of the following revenue recognition methods: cash, billings, percentage of completion, completed contract. Summarize your work in a table as follows ( 3 points): 7. State each method's weakncs when it comes to recognizing nevenue ( 2 points). CAE DATA: A construction company began operations on January 2, 2010. Daring the year the coenpary was awarded three construction contracts. The company incurrod 5300,000 cperatieg experses for the year for which $275.000 has been paid while the balance is ow od as of December 31, 2010. Projoct data is summarized for each of the three projecta in the following paraerages. Project 101: Low-Rise Office Building The initial contract was signed on January 5,2010 in the amount of 51,000,000, This amocen included 5800,000 for construction costs, 5150,000 for overhead mark-up, and 550,000 for grufir markup. The contractor broke ground on February 4, 2010. During the course of constnuction the client decided to upgrade the quality of the lighting and plumbing fixtures, resulting in a changs order issued to the contractor in the amount of $100,000 on October 7, 2010. The change order price was calculated by the contractor as follows; 550,000 construction costs, 537,500 overbead markup, \$12,500 profit markup. At the end of 2010 , construction was not complete. However, the client was renting out office space to other entities as well as using some of the offices for the client's own business entity. Work remaining as of December 31,2010 included surfacing the parking lot, erecting a portable parking attendant's station, miscellaneous site concrete work and landscaping. This work was schedule to be completed by May 1,2010, weather permitting. A summary of accounting date as of December 31,2010 included total conseruction conts in the amount of 5800,000 for which $600,000 was paid. The balance reflected unpaid bills for the month of December, and retention withheld on subcontracts throughout the course of the project. The total progress billing as of December 31, 2010 was $1,000,000 of which $900,000 was collected with the balance outatanding as retention receivable. The project manager estimated that given the work left to be completed, approximately $200,000 of construction cost would be incurred. Project 102: Retaining Wall The initial centract was signed on October 17,2010 in the amount of $100,000. The cnntract called for 1000 linear foet of g foct. high retaining wall to be erected in a residential subdivition. Exeavating and backfill was let to anotber contractor under separate contract, The cotimatar deternined that the wall would cost 540.00per linear foot for concrote, 510.00 per linear foot for reinforring and 580.00 per linear foot for labor. Average labor cout was $2000 per howar. The hourly mate included insurances and fringes tied to labor. Overhead and profit markip were ischided in these unit rates. At the eed of 2010 the projoct was not complete. The whedule indicates that back filling of the wall would not occur timeil all wall inataliation work was complete The project maneger desermined 750 linear fert of wall had beos installed and 2.150 labor hours aere used A wat Project 103: Junior-Senior High School The initial contract was signed on August 23, 2010. The contractor broke ground on October 1, 2010. Estimated completion date is December 31, 2011. Summary data as of December 31, 2010 yeacend includes the following: The contractor continued work on Project 103 during 2011. The contractor was not awarded any additional contracts during 2011. Company operating expense included $300,000 paid and $50,000 unpaid. Summary data as of December 31, 2011 for Project 103 includes the following: The contractor finished Project 101 and 102 in 2011 . Actual cost incurred on these projects matched the additional cost to complete estimated on 12/31/2010. 2. Calculate the revenue and gross profit for Project 101 for the period ending 12/31/2010 by applying the billings method for recognizing revenue. Compare the revenue value with the value when using the percentage of completion method. Comment on the contractor's billing practice (2 points). 3. Calculate the percent complete for Project 102 for each of the following methods: cost to cost, labor hour, and work quantity. Which method produces the most accurate result? Which method is the easiest to use? Which method should be used and why? (2 points)) 4. Calculate the eamed revenue and gross profit for Project 102 by applying the percentage of completion method. In this case, does it matter which method is used to determine pereent complete? Why or why not? ( 2 points) 5. Calculate the revenue and gross profit for Project 102 by applying the completed contract method. What "rule" must be applied to arrive at the correct answer? (2 points) 6. Calculate the company net profit before tax for the period ending December 31,2010 for each of the following revenue recognition methods: cash, billings, percentage of completion, completed contract. Summarize your work in a table as follows ( 3 points): 7. State each method's weakncs when it comes to recognizing nevenue ( 2 points) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Internal Audit Handbook Management With The SAP Audit Roadmap

Authors: Henning Kagermann, William Kinney, Karlheinz Küting, Claus-Peter Weber, Z. Keil, C. Boecker, J. Busch, O. Bussiek, M. H. Christ, P. Eckes, M. Falk, P. S. Greenberg, B. Reichert, M. Wolf

2008th Edition

3642430392, 978-3642430398