Answered step by step

Verified Expert Solution

Question

1 Approved Answer

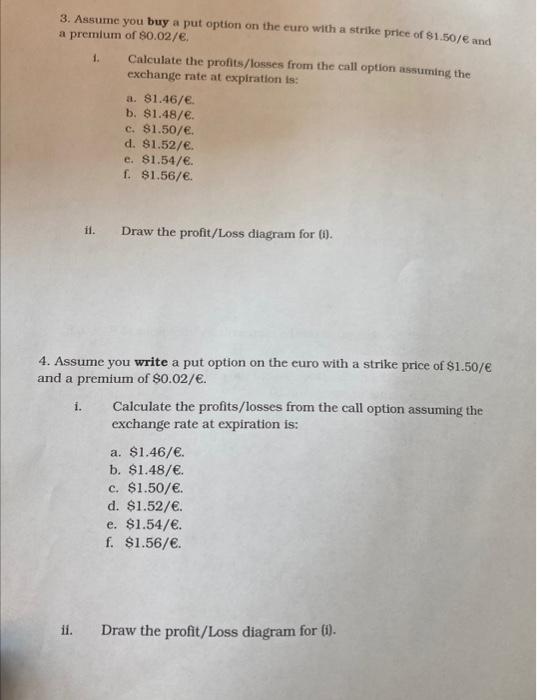

3. Assume you buy a put option on the euro with a strike price of $1.50/ and a premlum of $0.02/. 1. Calculate the profits/losses

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation Workbook

Authors: Tim Koller, Marc Goedhart, David Wessels, Jeffrey P. Lessard, McKinsey & Company

4th Edition

0471702161, 978-0471702160