Question

3. Compute expected return of the hedge fund on December 31, 2020 (this is the return that the hedge fund expects to earn over the

3. Compute expected return of the hedge fund on December 31, 2020 (this is the return that the hedge fund expects to earn over the year 2021). The answer should be given in decimal form (e.g., 1 % is 0.01). Hint: the sign matters!

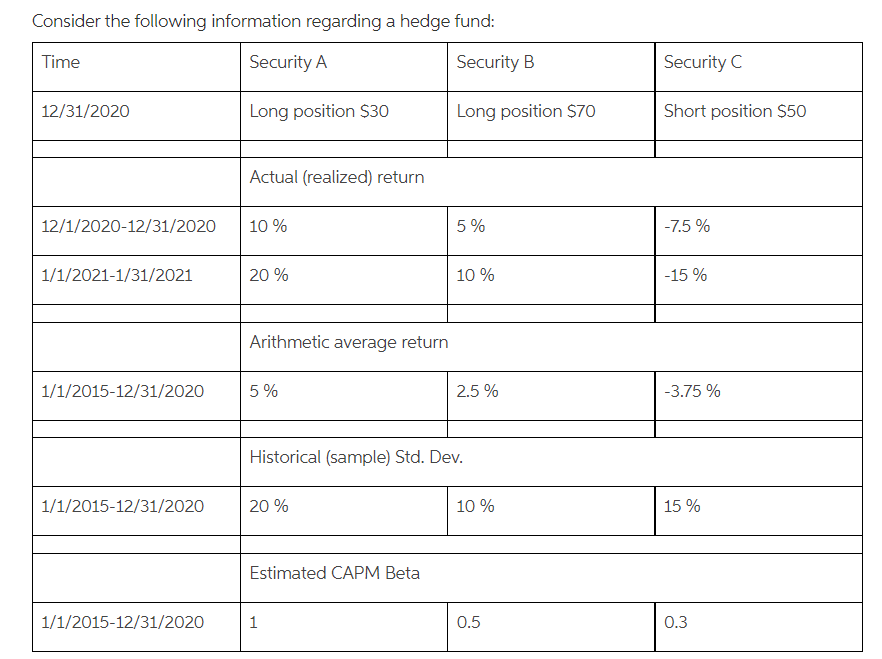

Consider the following information regarding a hedge fund: Time Security A Security B Security C 12/31/2020 Long position $30 Long position $70 Short position $50 Actual realized) return 12/1/2020-12/31/2020 10 % 5 % -7.5 % 1/1/2021-1/31/2021 20 % 10 % -15% Arithmetic average return 1/1/2015-12/31/2020 5 % 2.5 % -3.75 % Historical (sample) Std. Dev. 1/1/2015-12/31/2020 20 % 10 % 15 % Estimated CAPM Beta 1/1/2015-12/31/2020 1 0.5 0.3 Consider the following information regarding a hedge fund: Time Security A Security B Security C 12/31/2020 Long position $30 Long position $70 Short position $50 Actual realized) return 12/1/2020-12/31/2020 10 % 5 % -7.5 % 1/1/2021-1/31/2021 20 % 10 % -15% Arithmetic average return 1/1/2015-12/31/2020 5 % 2.5 % -3.75 % Historical (sample) Std. Dev. 1/1/2015-12/31/2020 20 % 10 % 15 % Estimated CAPM Beta 1/1/2015-12/31/2020 1 0.5 0.3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modeling Financial Time Series With S PLUS

Authors: Eric Zivot, Jiahui Wang

2nd Edition

0387279652, 0387323481, 9780387279657, 9780387323480