Answered step by step

Verified Expert Solution

Question

1 Approved Answer

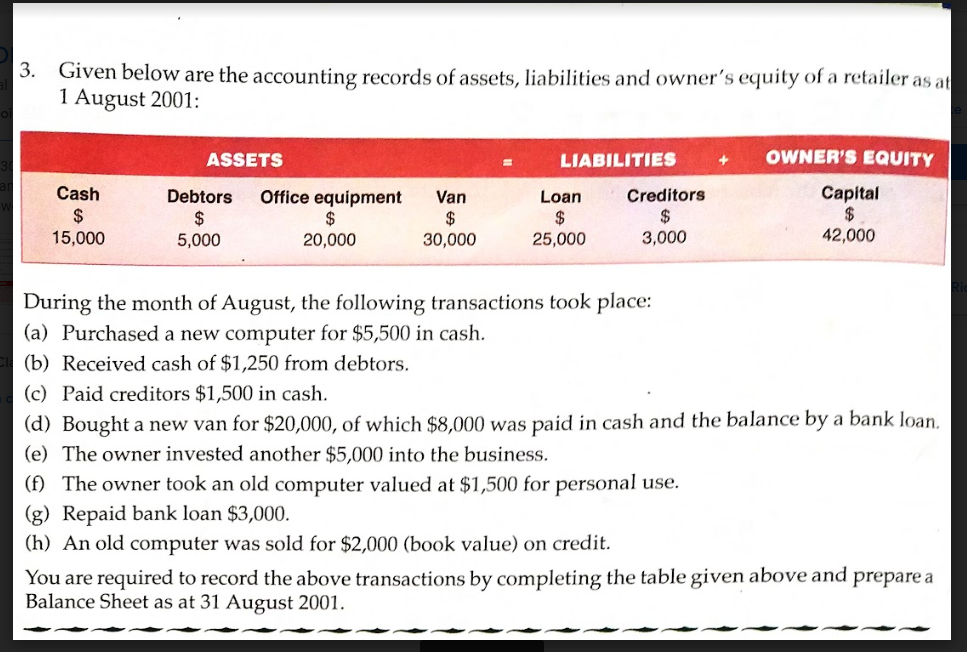

3. Given below are the accounting records of assets, liabilities and owner's equity of a retailer as a 1 August 2001: During the month of

3. Given below are the accounting records of assets, liabilities and owner's equity of a retailer as a 1 August 2001: During the month of August, the following transactions took place: (a) Purchased a new computer for $5,500 in cash. (b) Received cash of $1,250 from debtors. (c) Paid creditors $1,500 in cash. (d) Bought a new van for $20,000, of which $8,000 was paid in cash and the balance by a bank loan. (e) The owner invested another $5,000 into the business. (f) The owner took an old computer valued at $1,500 for personal use. (g) Repaid bank loan $3,000. (h) An old computer was sold for $2,000 (book value) on credit. You are required to record the above transactions by completing the table given above and prepare a Balance Sheet as at 31 August 2001

3. Given below are the accounting records of assets, liabilities and owner's equity of a retailer as a 1 August 2001: During the month of August, the following transactions took place: (a) Purchased a new computer for $5,500 in cash. (b) Received cash of $1,250 from debtors. (c) Paid creditors $1,500 in cash. (d) Bought a new van for $20,000, of which $8,000 was paid in cash and the balance by a bank loan. (e) The owner invested another $5,000 into the business. (f) The owner took an old computer valued at $1,500 for personal use. (g) Repaid bank loan $3,000. (h) An old computer was sold for $2,000 (book value) on credit. You are required to record the above transactions by completing the table given above and prepare a Balance Sheet as at 31 August 2001 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Internal Auditing A Guide For The New Auditor

Authors: David Galloway

3rd Edition

0894136917, 9780894136917