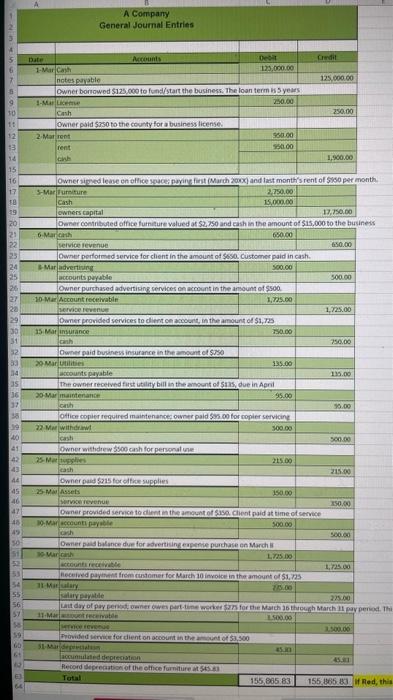

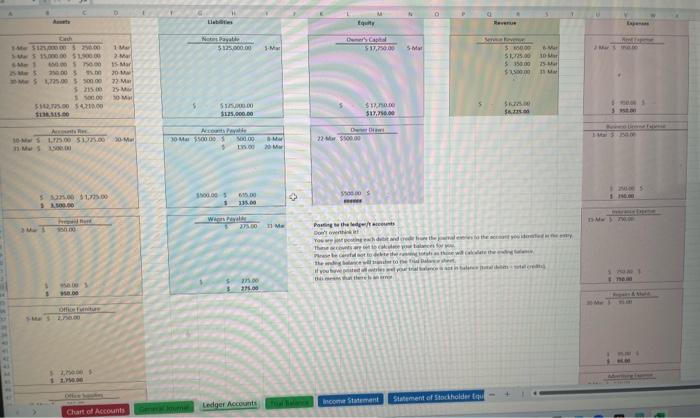

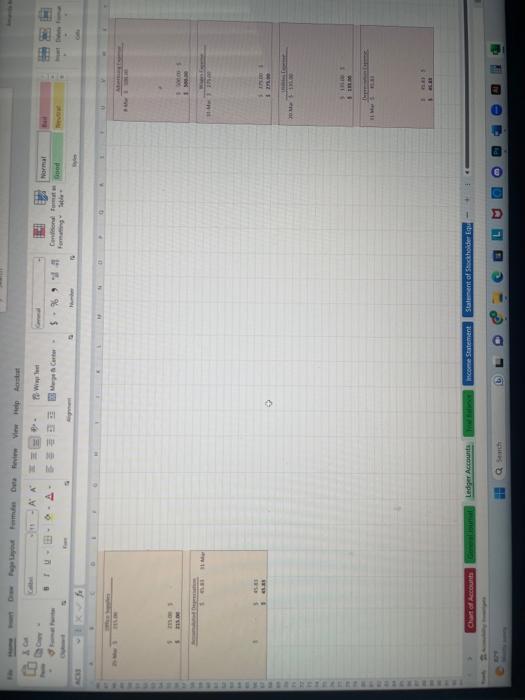

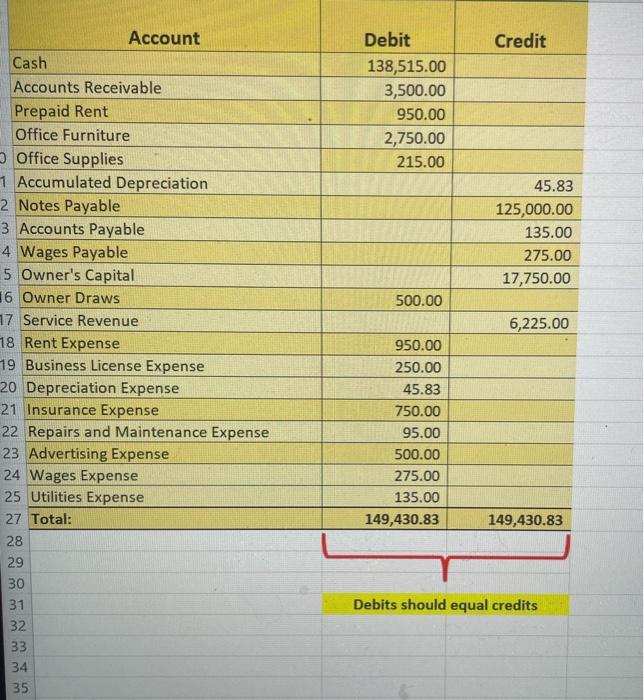

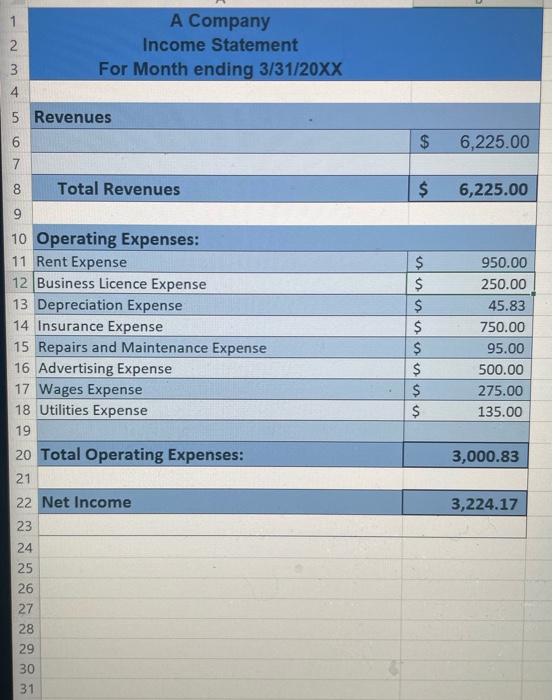

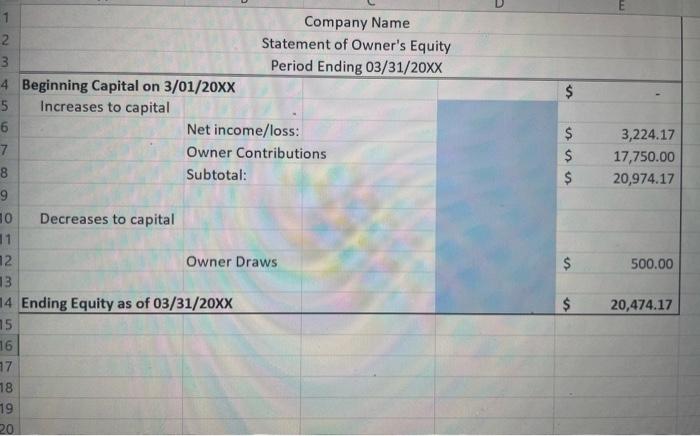

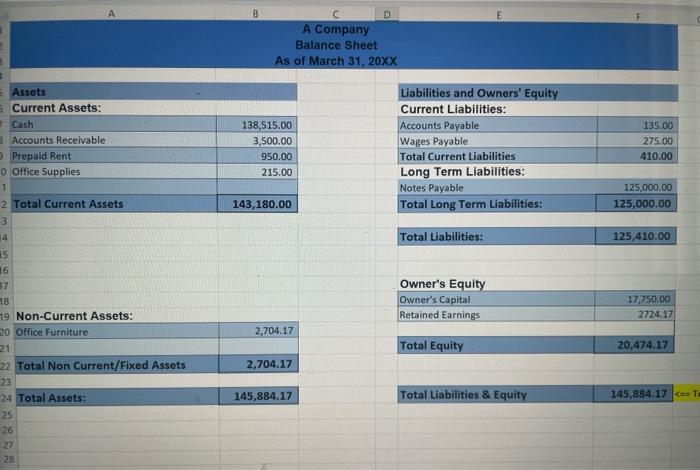

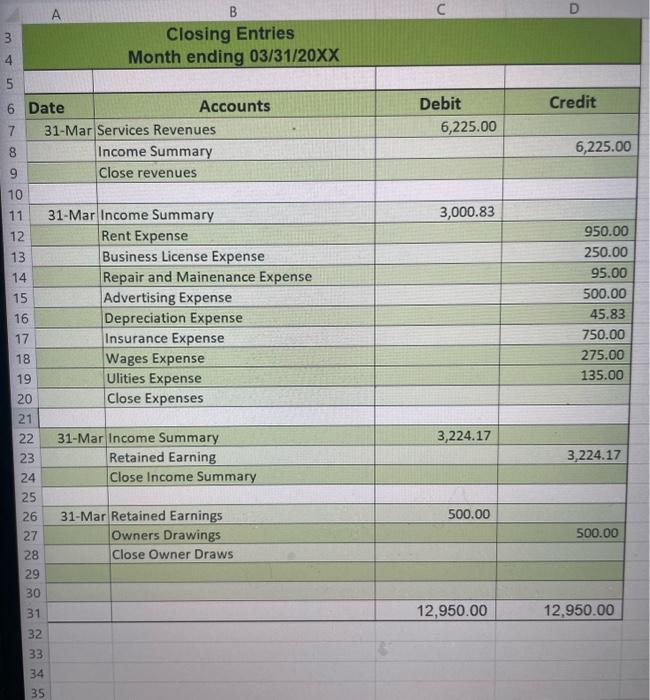

3. Summary: Write a summary of what the financial statements indicate about the company's financial health and performance. A. Purpose: Discuss the accounting process and the resulting financial statements as they relate to meeting the informationat needs of the user. B. Process; Explain the process used to produce accurate account balances and financial statements from the individual transaction data 1. Consider what is being communicated through each of the financial statements you prepared (income statement, statement of equity and balance sheet) and how this information will be used in business decision making and planning. C. Analysis: Explain the company's cash position, its net income as a percentage of sales, and its current liabilities to current assets position. D. Results: Discuss the results regarding profitability of the first month of operations: i. Consider how well the company is positioned to meet current liabilities. ii. Be sure to include the percentage of revenues that result in profitet income and the current ratio when discussing profitabiiity and liquidity based on the recorded month's results. iii. Consider key points in your observations of results: is the company operating profitably (what percent of revenues result in profitet income)? How well-poised are they to meet liabilities (discuss liquidity and current ratio)? E. Recommendations: Recommend a simple system of controls that can be implemented to ensure protection of company assets and the accuracy and integrity of their financial data as they anticipate further growth. i. Consider additional controls that will support the potential for adding merchandise and additional assets with business growth/expansion. F. Asset Valuation: Discuss the treatment of current and long-term assets on the balance sheet. i. Discuss at least two different methods of depreciation. Consider how the methods of depreciation will be determined. ii. Discuss how LIFO, FIFO, and average methods will differ and provide examples of types of applicable merchandising iii. Consider how accounting will change with the addition of merchandise inventory. Introduction [In this section, include the purpose of the report. Describe the kind of information these financial statements provide to various aspects of the business.] Process [In this section you will discuss the process you used to generate accurate financial statement results for the business owner from the list of business transactions provided. Explain what is being communicated through each of the financial statements you prepared (income statement, statement of equity and balance sheet) and how this information will be used in business decision making and planning.] Financial Statement Analysis [This section should center on your analysis of the financial performance of the company based on the statements you prepared. Discuss key points on your observations of results: Is the company operating profitably (what percent of revenues result in profit net income)? How well poised are they to meet liabilities (discuss liquidity and current ration? Internal Controls [Provide suggestions for a simple system of internal controls to assist the owners in protecting assets and ensuring accuracy in financial data. Consider additional controls that will support the potential for adding merchundise and additional assets with business growth/expansion-] Looking to the Future [In response to the owner's request for additional information and support for future growth, discuss accounting considerations associated with the acquisition of additional long term/fixed assets, and the addition of merchandise inventory. How will the company account for the costs of long-term assets? How will the method of depreciation be determined? (Expand on 2 different methods of depreciation to demonstrate ideal application). How does accounting change with the addition of merchandise inventory? How will it be determined which inventory costing method to apply? (Discuss how the FIFO, LIFO, and Average methods differ and provide examples of the types of merchandising scenarios that would be ideally applicable in each case.)] Debits should equal credits Company Name Statement of Owner's Equity Period Ending 03/31/20XX Beginning Capital on 3/01/20XX Increases to capital Net income/loss: Owner Contributions Subtotal: Decreases to capital Owner Draws Ending Equity as of 03/31/20XX \begin{tabular}{|rr|} $ & \\ $ & 3,224.17 \\ $ & 17,750.00 \\ $ & 20,974.17 \\ \hline \end{tabular} A Company Balance Sheet As of March 31, 20X \begin{tabular}{|l|r|} \hline Assets \\ \hline Current Assets: \\ \hline Cash & \\ \hline Accounts Receivable & 138,515.00 \\ \hline Prepaid Rent & 3,500.00 \\ \hline Office Supplies & 950.00 \\ \hline & 215.00 \\ \hline Total Current Assets & 143,180.00 \\ \hline \end{tabular} Non-Current Assets: \begin{tabular}{|l|r|} \hline Office Furniture & 2,704.17 \\ \hline Total Non Current/Fixed Assets & 2,704.17 \\ \hline \end{tabular} Total Assets: 145,884,17 Liabilities and Owners' Equity Current Liabilities: \begin{tabular}{|l|r|} \hline Accounts Payable & 135.00 \\ \hline Wages Payable & 275.00 \\ \hline Total Current Liabilities & 410.00 \\ \hline \end{tabular} Long Term Liabilities: \begin{tabular}{|l|r|} \hline Notes Payable & 125,000.00 \\ \hline Total Long Term Liabilities: & 125,000.00 \\ \hline \end{tabular} \begin{tabular}{|l|r|} \hline Total Liabilities: & 125,410.00 \\ \hline \end{tabular} Owner's Equity \begin{tabular}{|l|r|} \hline Owner's Capital & 17,750.00 \\ \hline Retained Earnings & 2724.17 \\ \hline \end{tabular} Total Equity 20,474.17 Total Liabilities \& Equity 145,884,17