Answered step by step

Verified Expert Solution

Question

1 Approved Answer

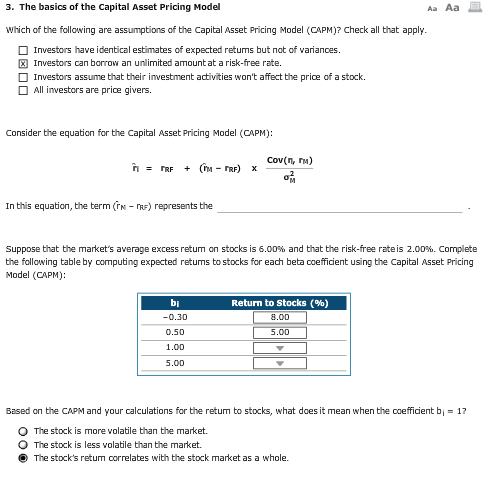

3. The basics of the Capital Asset Pricing Model Aa Aa which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Almanac Of Online Trading

Authors: Terry Wooten

1st Edition

0071358595, 978-0071358590