Answered step by step

Verified Expert Solution

Question

1 Approved Answer

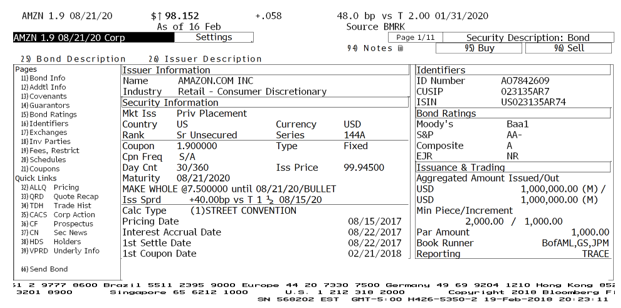

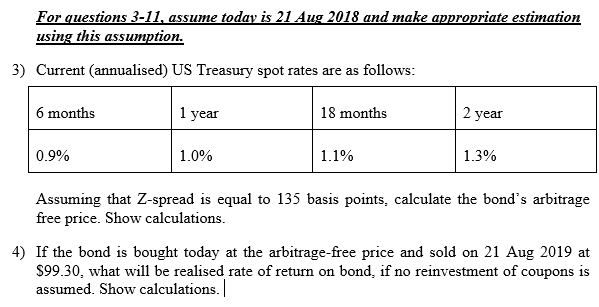

3201 9900 0600 Drami1 551125959000 Europe 4420,73307500 cor For questions 3-11, assume todav is 21Aug2018 and make appropriate estimation using this assumption. 3) Current (annualised)

3201 9900 0600 Drami1 551125959000 Europe 4420,73307500 cor For questions 3-11, assume todav is 21Aug2018 and make appropriate estimation using this assumption. 3) Current (annualised) US Treasury spot rates are as follows: Assuming that Z-spread is equal to 135 basis points, calculate the bond's arbitrage free price. Show calculations. 4) If the bond is bought today at the arbitrage-free price and sold on 21 Aug 2019 at $99.30, what will be realised rate of return on bond, if no reinvestment of coupons is assumed. Show calculations

3201 9900 0600 Drami1 551125959000 Europe 4420,73307500 cor For questions 3-11, assume todav is 21Aug2018 and make appropriate estimation using this assumption. 3) Current (annualised) US Treasury spot rates are as follows: Assuming that Z-spread is equal to 135 basis points, calculate the bond's arbitrage free price. Show calculations. 4) If the bond is bought today at the arbitrage-free price and sold on 21 Aug 2019 at $99.30, what will be realised rate of return on bond, if no reinvestment of coupons is assumed. Show calculations Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Day Trading Strategies And Risk Management

Authors: Richard N. Williams

1st Edition

979-8863610528