Answered step by step

Verified Expert Solution

Question

1 Approved Answer

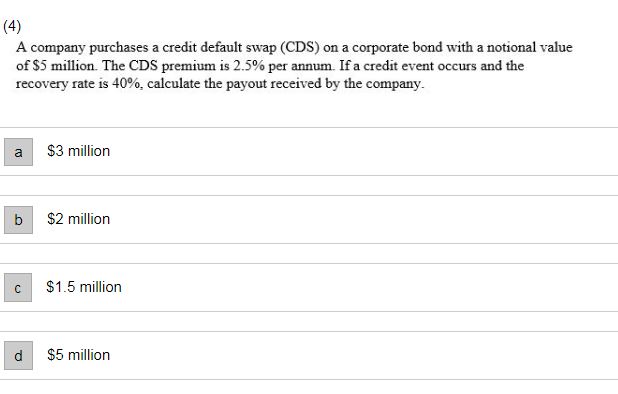

(4) A company purchases a credit default swap (CDS) on a corporate bond with a notional value of $5 million. The CDS premium is 2.5%

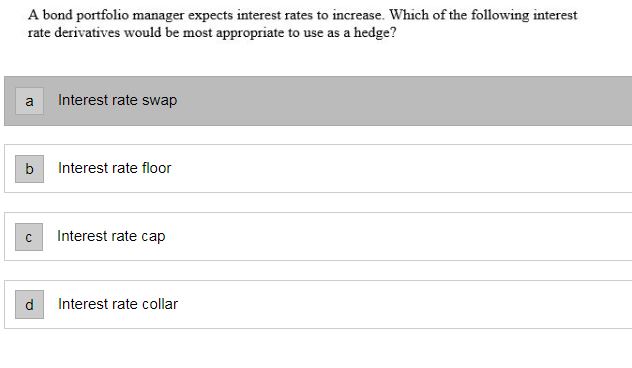

(4) A company purchases a credit default swap (CDS) on a corporate bond with a notional value of $5 million. The CDS premium is 2.5% per annum. If a credit event occurs and the recovery rate is 40%, calculate the payout received by the company. \$3 million \$2 million \$1.5 million $5 million A bond portfolio manager expects interest rates to increase. Which of the following interest rate derivatives would be most appropriate to use as a hedge? Interest rate swap Interest rate floor Interest rate cap Interest rate collar

(4) A company purchases a credit default swap (CDS) on a corporate bond with a notional value of $5 million. The CDS premium is 2.5% per annum. If a credit event occurs and the recovery rate is 40%, calculate the payout received by the company. \$3 million \$2 million \$1.5 million $5 million A bond portfolio manager expects interest rates to increase. Which of the following interest rate derivatives would be most appropriate to use as a hedge? Interest rate swap Interest rate floor Interest rate cap Interest rate collar Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Managerial Finance

Authors: Scott Besley, Eugene F. Brigham

13th Edition

0324258755, 9780324258752