Answered step by step

Verified Expert Solution

Question

1 Approved Answer

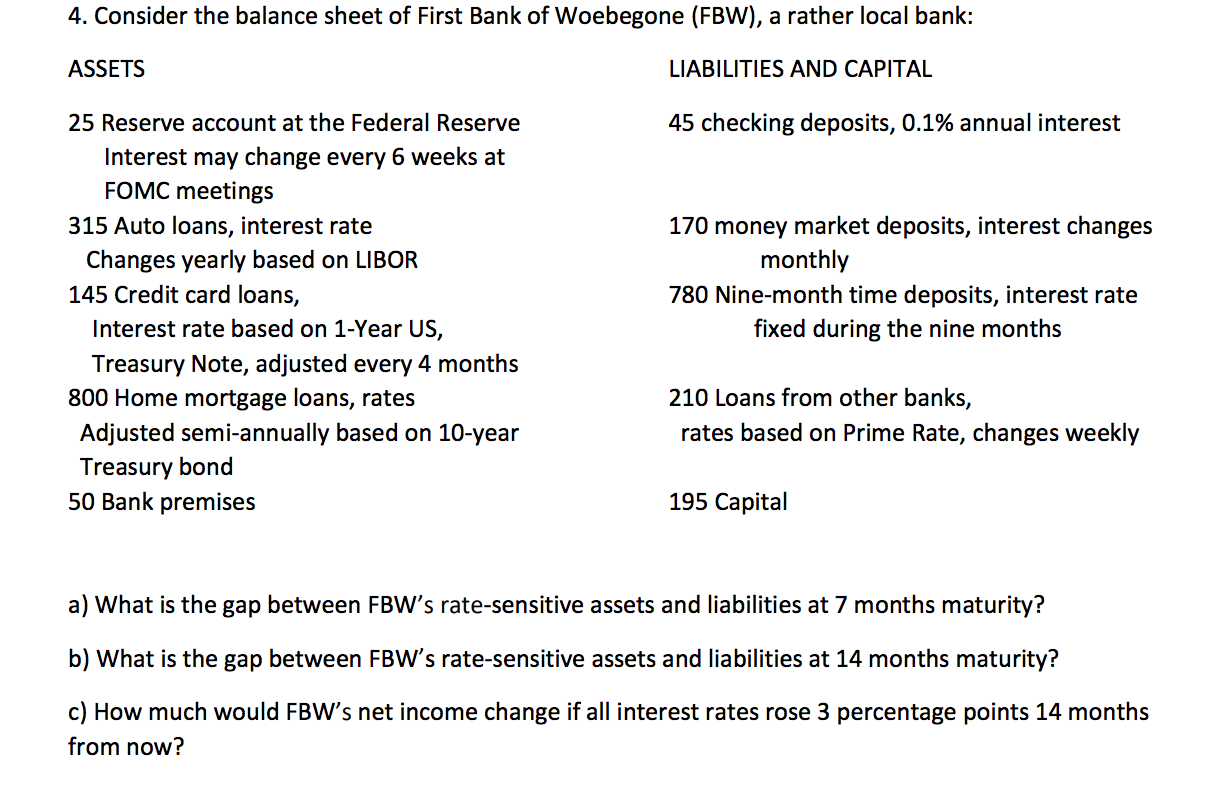

4. Consider the balance sheet of First Bank of Woebegone (FBW), a rather local bank: ASSETS LIABILITIES AND CAPITAL 45 checking deposits, 0.1% annual interest

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

AS9101D Auditing For Process Performance Combining Conformance And Effectiveness To Meet Customer Satisfaction

Authors: Chad Kymal

1st Edition

0873898079, 978-0873898072