Answered step by step

Verified Expert Solution

Question

1 Approved Answer

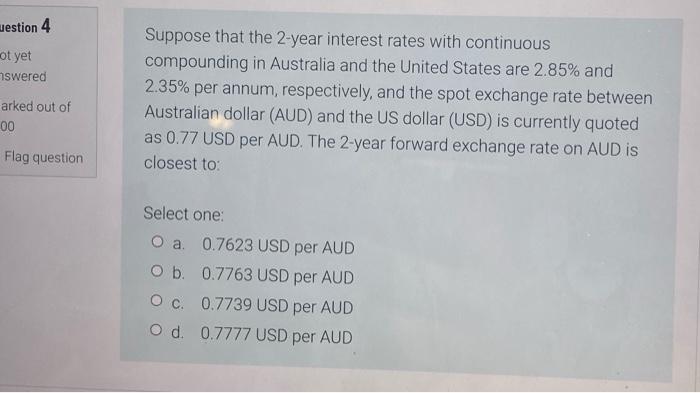

4 estion 4 ot yet swered arked out of 00 Suppose that the 2-year interest rates with continuous compounding in Australia and the United States

4

estion 4 ot yet swered arked out of 00 Suppose that the 2-year interest rates with continuous compounding in Australia and the United States are 2.85% and 2.35% per annum, respectively, and the spot exchange rate between Australian dollar (AUD) and the US dollar (USD) is currently quoted as 0.77 USD per AUD. The 2-year forward exchange rate on AUD is closest to Flag question Select one: O a 0.7623 USD per AUD O b. 0.7763 USD per AUD Oc. 0.7739 USD per AUD Od 0.7777 USD per AUD Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Reforming The Governance Of The Financial Sector

Authors: David Mayes , Geoffrey Wood

1st Edition

0415686849, 978-0415686846