Answered step by step

Verified Expert Solution

Question

1 Approved Answer

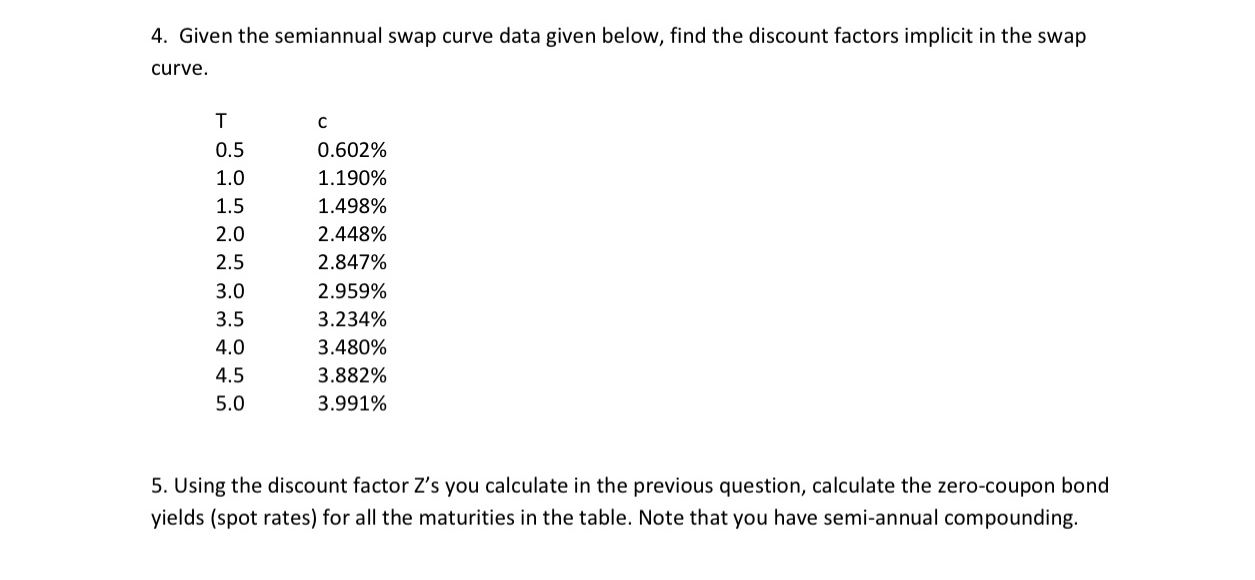

4. Given the semiannual swap curve data given below, find the discount factors implicit in the swap curve. T C 0.5 0.602% 1.0 1.190%

4. Given the semiannual swap curve data given below, find the discount factors implicit in the swap curve. T C 0.5 0.602% 1.0 1.190% 1.5 1.498% 2.0 2.448% 2.5 2.847% 3.0 2.959% 3.5 3.234% 4.0 3.480% 4.5 3.882% 5.0 3.991% 5. Using the discount factor Z's you calculate in the previous question, calculate the zero-coupon bond yields (spot rates) for all the maturities in the table. Note that you have semi-annual compounding.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey Rosen, Ted Gayer

10th edition

9781259716874, 78021685, 1259716872, 978-0078021688