Answered step by step

Verified Expert Solution

Question

1 Approved Answer

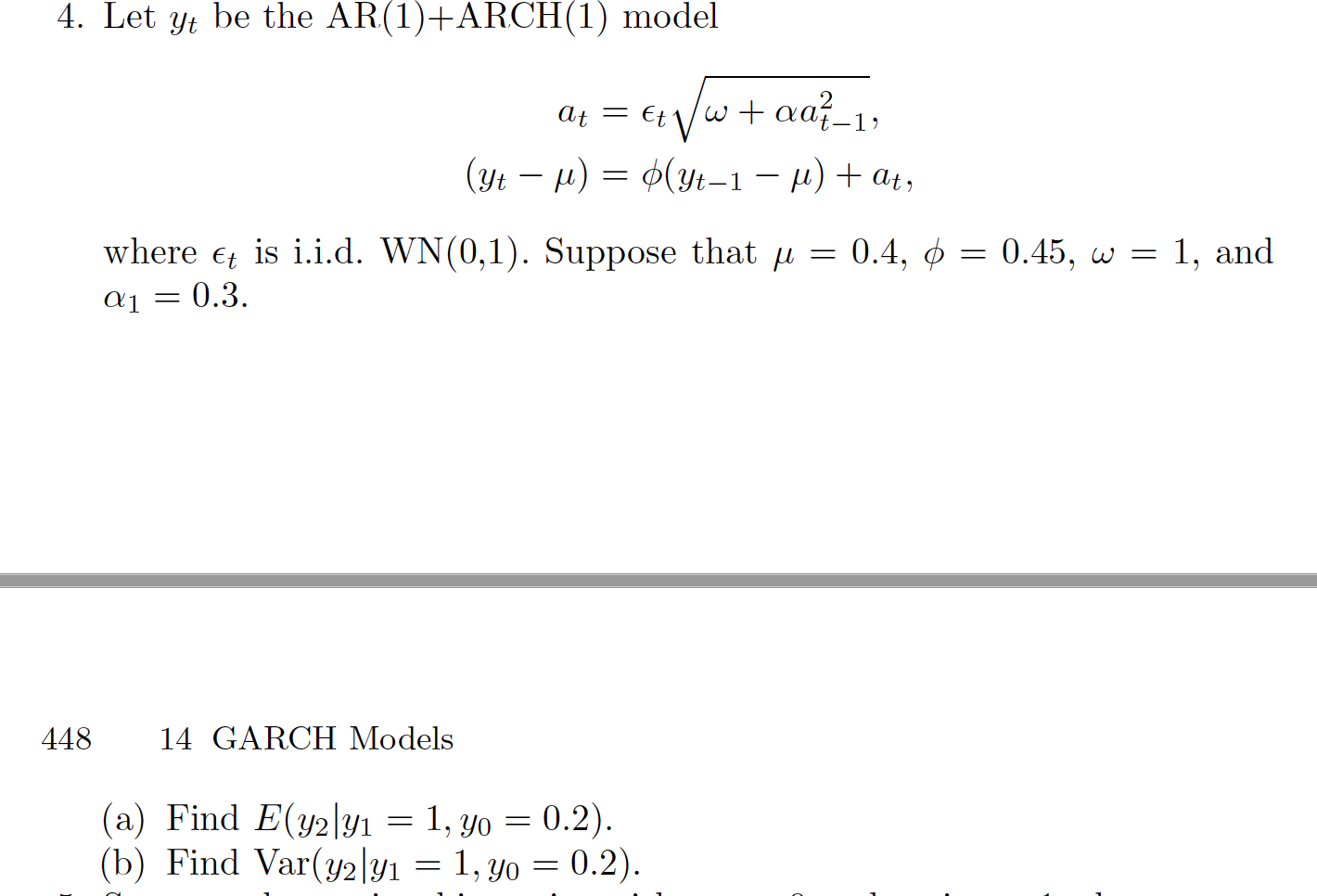

4. Let yt be the AR(1)+ARCH(1) model at(yt)=t+at12,=(yt1)+at, where t is i.i.d. WN (0,1). Suppose that =0.4,=0.45,=1, and 1=0.3. 44814 GARCH Models (a) Find E(y2y1=1,y0=0.2).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ecological Money And Finance

Authors: Thomas Lagoarde-Segot

1st Edition

3031142314, 978-3031142314