Answered step by step

Verified Expert Solution

Question

1 Approved Answer

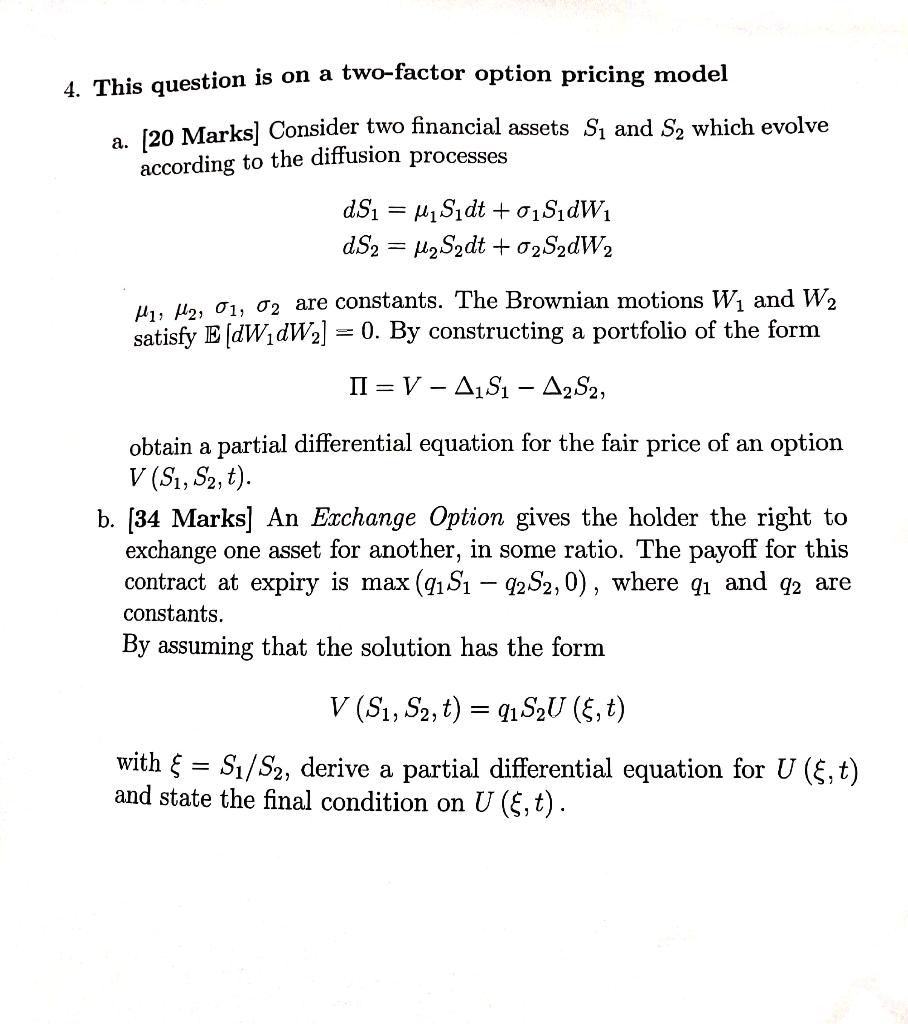

4. This question is on a two-factor option pricing model a. [20 Marks] Consider two financial assets S and S which evolve according to the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money How The Destruction Of The Dollar Threatens The Global Economy And What We Can Do About It

Authors: Steve Forbes, Elizabeth Ames

1st Edition

0071823700,0071823719