Answered step by step

Verified Expert Solution

Question

1 Approved Answer

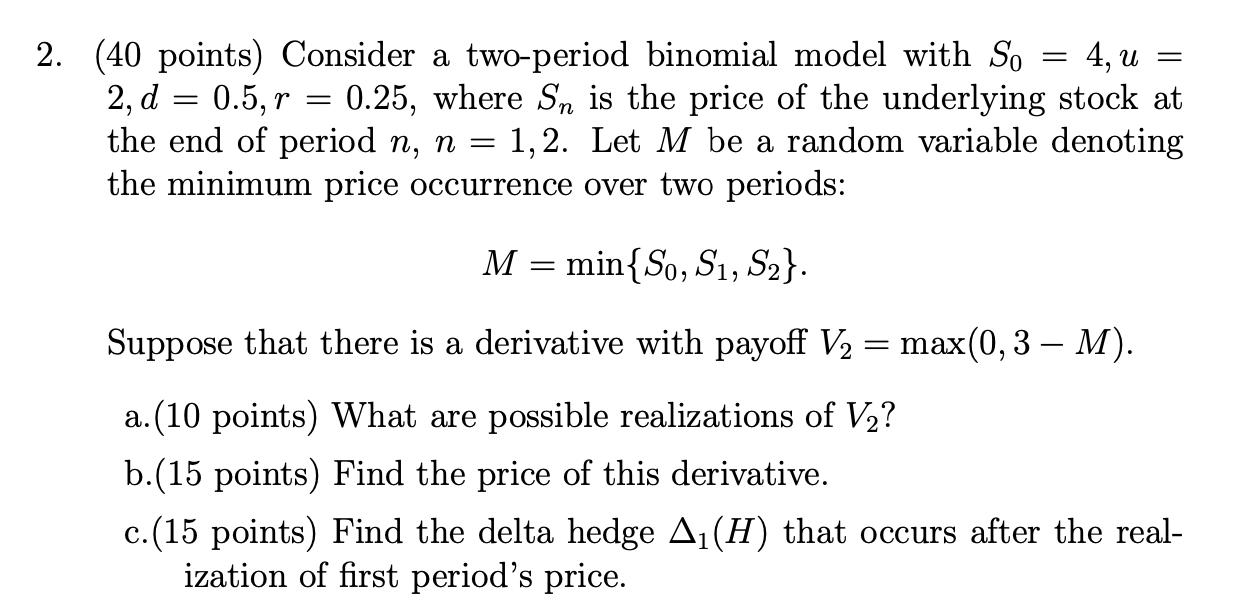

= 4, u = 2. (40 points) Consider a two-period binomial model with So 2, d=0.5, r = 0.25, where Sn is the price

= 4, u = 2. (40 points) Consider a two-period binomial model with So 2, d=0.5, r = 0.25, where Sn is the price of the underlying stock at the end of period n, n = 1,2. Let M be a random variable denoting the minimum price occurrence over two periods: M = min{So, S1, S2}. Suppose that there is a derivative with payoff V = max(0, 3 M). a. (10 points) What are possible realizations of V? b.(15 points) Find the price of this derivative. c.(15 points) Find the delta hedge A(H) that occurs after the real- ization of first period's price.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Derivatives Markets

Authors: Robert McDonald

3rd Edition

978-9332536746, 9789332536746