Answered step by step

Verified Expert Solution

Question

1 Approved Answer

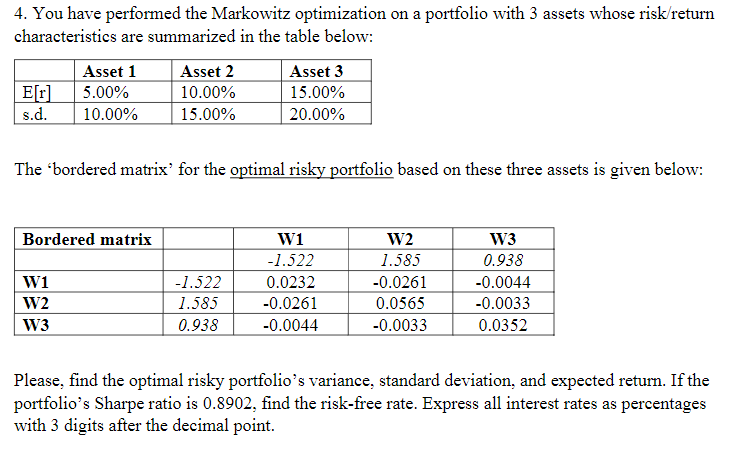

4. You have performed the Markowitz optimization on a portfolio with 3 assets whose risk/return characteristics are summarized in the table below: Asset 1 Asset

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Innovation Ecosystem Growth Developing Strategies For Sustainable Growth

Authors: Isadora Bozzi

1st Edition

979-8388710420