Answered step by step

Verified Expert Solution

Question

1 Approved Answer

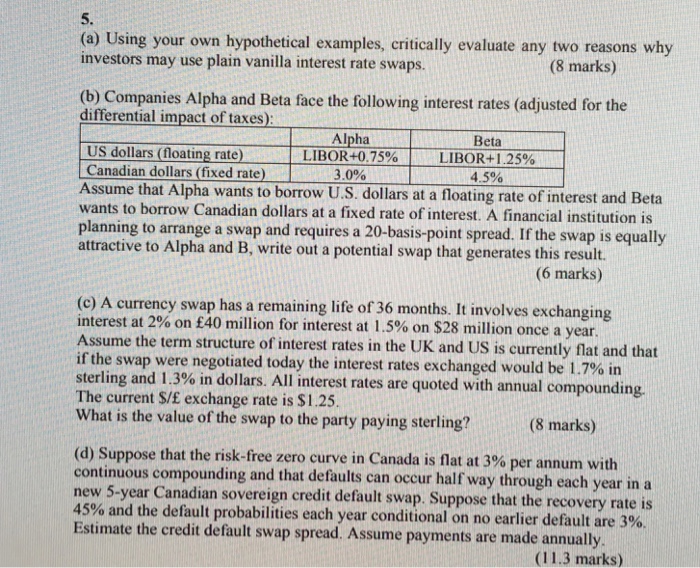

5. (a) Using your own hypothetical examples, critically evaluate any two reasons why investors may use plain vanilla interest rate swaps. (8 marks) (b) Companies

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

Concise 6th Edition

324664559, 978-0324664553